Agrochem Jewel of Bursa

ANCOM - THE NEXT SUGAR BABY OF BURSA?

THE NEXT SUGAR BABY OF BURSA MALAYSIA?

▪️ Coffee : 3.5 years high

▪️ Sugar : 4 years high

▪️ Soybean : 6.5 years high

▪️ Wheat : 7 years high

▪️ Corn : 8 years high

▪️ CPO : 10 years high

Clearly, we are in the midst of a commodity super bull run and wall street banks are signalling that this is just the “first leg of a supercycle”. Goldman Sachs was one of the very first to call it in late 2020, and since then almost every major fund house have taken long positions on commodities. Key factors why this commodity bull still has legs to run:

- Vaccine-driven global recovery

- Supply disruptions exacerbated by lockdowns

- Continuous growth of China, the world’s biggest buyer of natural resources

- Aggressive fiscal stimulus fanning inflation concerns – commodity as hedge

Our Bursa market witnessed its first ever “limit-up” counter today that is sugar related: Malaysia’s largest sugar refiner and producer, MSM (5202).

Which other Malaysian listed co could possibly be a beneficiary of record sugar prices?

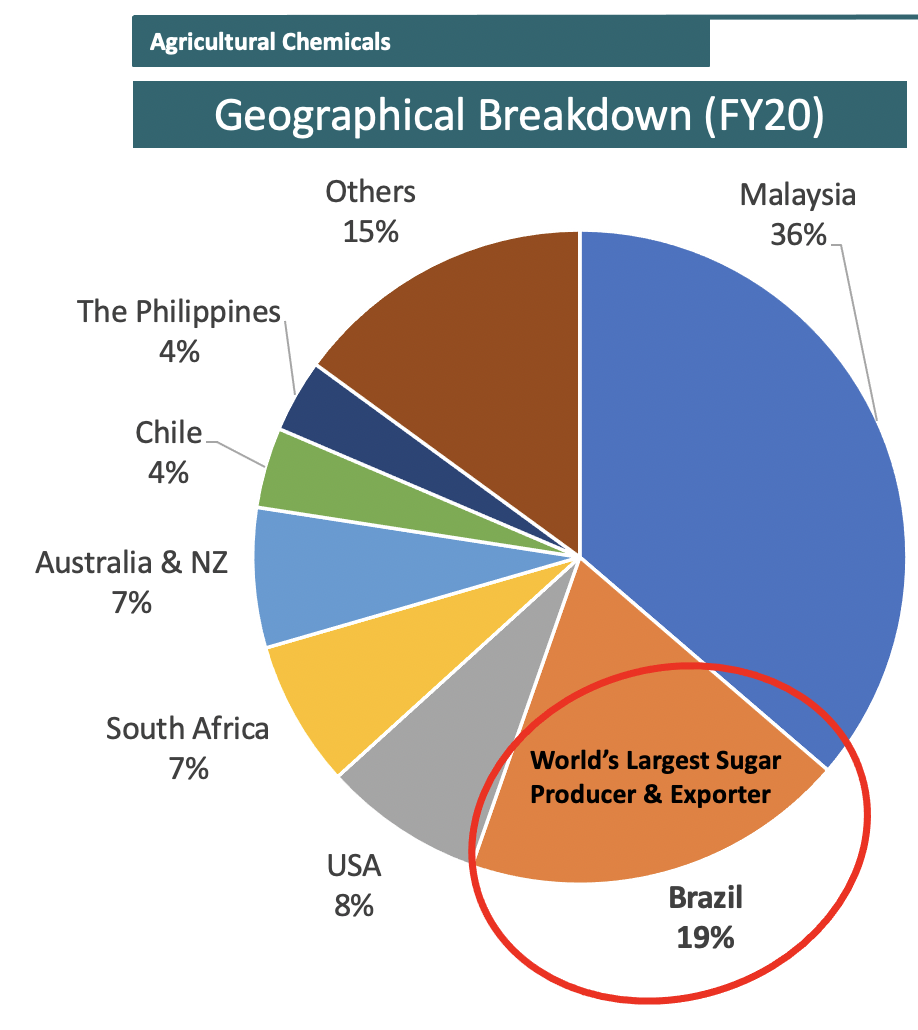

MSM as a refiner would need to source raw sugar from sugarcane-growing countries such as Thailand and of course, the number one sugarcane grower in the world: Brazil.

What if we were told that there is one Malaysian listed co whose customer is the world's largest sugarcane grower?

ANCOM (4758) is the ONLY Malaysian agrochemical manufacturer who has a presence in Brazil, its largest export market. Ancom's agrochem active ingredient products are sold to sugarcane growers in Brazil. These herbicides are important for plantation management, to increase yield and production of sugarcane.

The following pie chart details its source of revenue:

The increasing sugar prices has contributed positively to Ancom’s earnings as evident by the quarter results released Q1 & Q2. If one is diligent to look through the segmental reporting, its agrochem segment’s profit for the first 2 quarters is 40% up on the same period last financial year.

Agrochem EBITA

FY21 YTD Q2 : RM 27.5m (+40%)

FY20 YTD Q2 : RM 19.5m

FY20 Full-Year : RM 35.4m

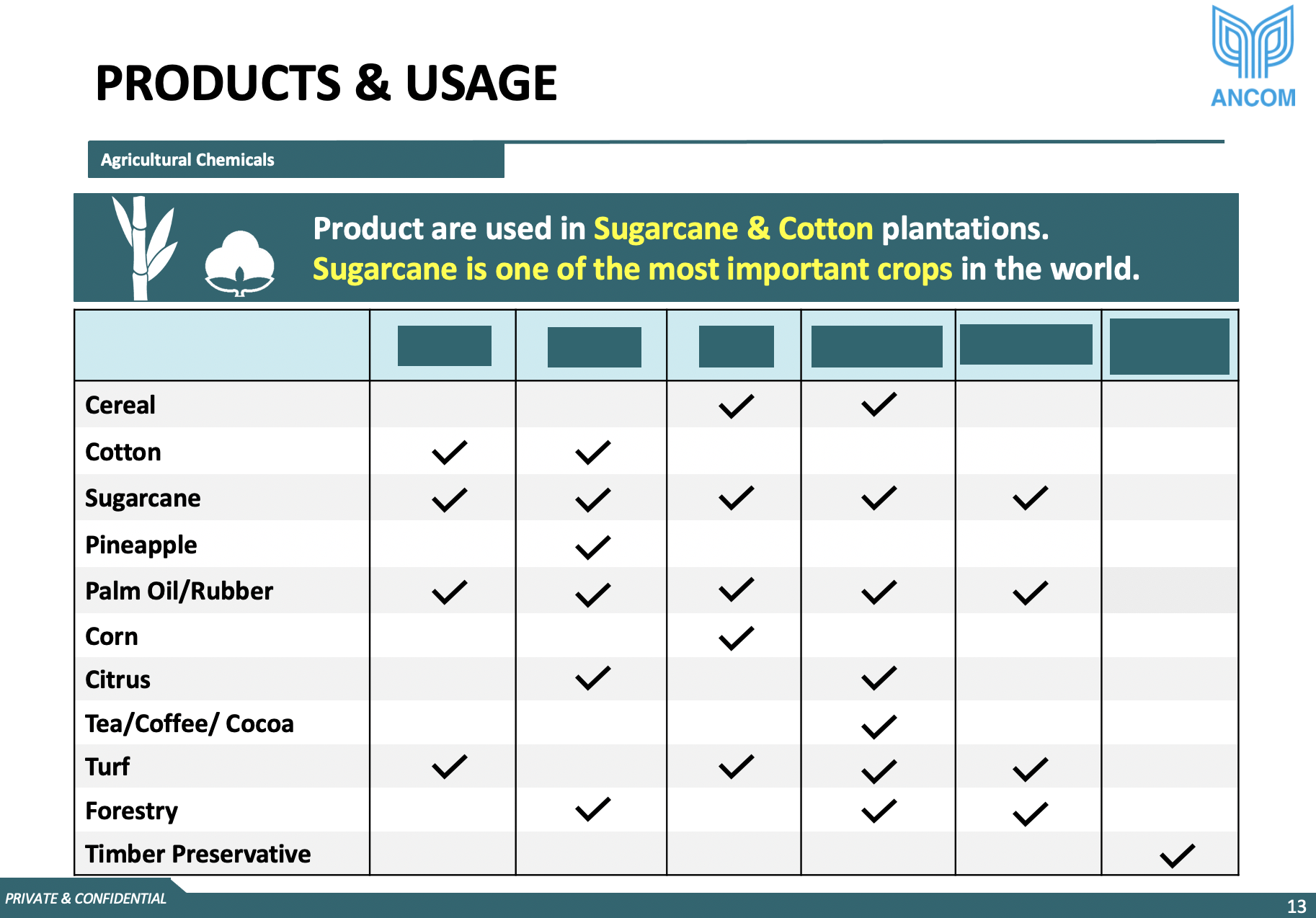

Apart from sugar, Ancom’s products cover a wide variety of food crops as well such as corn, coffee, palm oil. The prices of the crops mentioned have leaped to multi-year highs. This has enabled and encouraged growers to spend more on agrochemicals to enhance yield.

MSM’s “limit-up” performance has just awakened investors and analysts, all on a sugar rush to identify the next SUGAR BABY of Bursa Malaysia.

- Beneficiary of record-high sugar prices

- Only Malaysian co serving the world’s largest sugar exporter Brazil

- Impending completion of RTO exercise of ALB-S5

-

Turnaround into profitable territory Q1 & Q2,

Q3-Q4 said to be ‘continuation of upward trend’

Could ANCOM be the next sugar-themed investment gem of 2021?

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Agrochem Jewel of Bursa

Discussions

1 person likes this. Showing 5 of 5 comments

Don't get angry. Ancom chemicals are too pricey even for big company. Malaysian plantation prefer cheap and efficient calibration of chemicals.

2021-02-27 10:30

Momokoko, yes everybody wants cheap inputs but still Ancom derives one third revenue from Malaysia. Clearly there are customers paying for their agrochem.

2021-02-28 17:33

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-14 16:55:00

EMA 5

5 Mins

SELL

2025-01-14 16:45:00

EMA 5

5 Mins

BUY

2025-01-14 16:25:00

ADX

5 Mins

BUY

2025-01-14 16:20:00

EMA 5

5 Mins

SELL

2025-01-14 16:15:00

ADX

5 Mins

SELL

Apps

Top Articles

1

2

Good Articles to Share

Eli Lilly CEO on Fighting Cancer and Obesity, Drug Pricing (Correct)

3

Good Articles to Share

Evercore ISI's Julian Emanuel says its too early to buy weakness

4

Good Articles to Share

5

Good Articles to Share

6

Good Articles to Share

7

Good Articles to Share

Tens of thousands demonstrate in nationwide strike in Belgium | REUTERS

8

Good Articles to Share

Thousands help at huge Los Angeles wildfire donation center | REUTERS

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

michaeso

Good luck everyone

2021-02-27 09:13