Artemis FA

Focus Lumber, Cheap and Beautiful

Focus Lumber Bhd https://klse.i3investor.com/servlets/stk/5197.jsp is a player in the wood and forestry product industry specializing in the production of plywood, veneer and laminated veneer lumber. These products are widely used in all industries ranging from recreational vehicle, home decoration, furniture and structural application in real estate construction. As a brief introduction, plywood is a flat panel built up of sheets of veneer, united under pressure by a bonding agent to create a panel with an adhesive bond between the plies. Plywood can be made from softwood and hardwood but Focus Lumber Bhd produces its products mainly from hardwood (since it is located in South East Asia). As for LVL, it is produced by recycling wood chips and veneer slips and commonly used in hand rail, wooden flooring and door frames. Undoubtedbly, it can also be used for production of high-value furniture and housing materials with higher margin. As a side note, the company also established an eletricity generation entity (Untung Ria Sdn Bhd) to generate electricity by recycling the waste sourced from their production processes. This allowed for cost minimization while demonstrating the management's competency and concern for corporate social responsibilities.

Competitive Strengths

- Experienced management team: Founders possess approximately 40 years of experience each in the trading of timber and plywood manufacturing

- Approved international recognition on product quality: first plywood mill in Malaysia to obtain CARB Certified Manufacturer (formaldehyde emissions standards in US [Important especially after Lumber Liquidator Corporation downfall]), IHPA-2000 by the International Wood Products Association (in essence demonstrates the products meeting the highest standards of quality and consistency in the market place

- Established track records and relationship with customers (Ihlo Sales & Import Co. has been a customer for approximately 15 years or more)

- Persistent innovator in quality improvement and cost optimization processes (based on company's consistent commitment to capital expenditure for the past 15 years or so)

- Niche market player among Malaysian plywood mills (Huge proportion of revenue generated from the recreational vehicle industry where plywood used has to be of high quality and command a better margin)

Risk Factors

- No long-term contract with major customers: Customers purchase by order-basis so there is no contractual business (Focus Lumber Bhd mitigates this by enhancing customer relationship as seen by Ihlo Sales & Import Co. constant commitment)

- Log supply disruption: The company does not own any timber concession but tries to mitigate by diversifying their source of supplies (about 20 to 40 suppliers in Keningau, Sabah) and occassionally buying forward to hedge against the risk of sudden supply disruption

- Labor shortage: The industry is labor intensive so any labor shortage or spike in labor cost is disadvantageous (foreign employee tariff in 2016) but the company has consistently reinforced their commitment to reduce the labor intensity of the operation as a mitigation strategy. (Focus Lumber Bhd walk its talk since there were 955 factory workers in 2010 [right after recession] vs. 894 factory workers in 2016)

- Reliance on the US market (Focus Lumber Bhd is increasing its business dealings with South Korea)

- Foreign exchange risk: Focus Lumber Bhd's revenue are mainly generated in US Dollar and hence a huge appreciation of Ringgit Malaysia against US Dollar may erode the company's pricing power

Industry Outlook

Since the interior of a recreational vehicle is not huge and moisture can damage softwood products in it fairly easily, plywood is preferable over MDF and some other relevant products when it comes to flooring, ceiling and wall usage. With nearly 50% of RVs worldwide being made in America, it helps in explaining Focus Lumber Bhd's concentration in the US market. As a very niche market, most of the data employed here are provided by RVIA that emphasizes industry education, training and marketing of RVs.

In terms of growth prospect, the President of the Recreation Vehicle Industry Association forecasts RV industry's shipments to reach 472200 units in 2017, a 9.6% growth from the number shipped last calendar year while continuing this momentum into 2018. The interest in this market can be demonstrated by how the 65th Annual California RV Show is sold out within a short timeframe since launching. Among the reasons that support the RV industry prospects includes the following:

-

RV ownership and travel is a great value even if oil price spikes (Airplane ticket is costlier too when oil price spike)

Cost Comparisons of Vacations (Source: PKF Consulting, USA) Vacation Mode of Travel 3 Days 7 Days Traveling in lite-duty truck / SUV, towing their travel trailer, staying at camp grounds and preparing all meals in the trailer or outdoors $880 $1997 Traveling in compact motorhome, staying at campgrounds and preparing all meals in the motorhome or outdoors $880 $2035 Traveling in airplane, staying at a rental house / condominium, eating the majority of meals in the rental unit $2958 $4045 - Shorter trips closer to home: With more than 16000 campgrounds nationwide (USA), it's easy for RVers to stay closer to home

- IRS tax deduction: For most RV buyers, interest on their loan is deductible as second home mortgage interest

- Population and demographic trends: University of Michigan study of RV consumers identified that buyers aged 35 - 54 are the largest segment of RV owners while the median age of US workers is approximately 42 years old (Bureau of Labor Statistics). Concurrently, baby boomers are entering retirement and RV sales are expected to benefit as aging baby boomers continue to enter the age range in which RV ownership has been historically highest

- RV manufacturers are offering innovative new products: optimal mix of sizes and price for budget concious consumers, lightweight and fuel-efficient motorhomes (green technologies such as solar panels and energy efficient components are appearing on an increasing number of RV models)

The following shows the Recreational Vehicle Delivery (US Data)

| (Unit '000) | |||||||||||||

| Time | January | February | March | April | May | June | July | August | September | October | November | December | Growth (%) |

| 2007 | 26.8 | 29.7 | 37.1 | 34.3 | 33.6 | 34.5 | 27.9 | 30.4 | 26.8 | 28.4 | 21.5 | 22.4 | |

| 2008 | 24.9 | 27.6 | 30.1 | 31.4 | 25 | 23.5 | 17.1 | 16.9 | 15.4 | 13.5 | 6 | 5.6 | -32.94% |

| 2009 | 7.3 | 10.3 | 12.8 | 13.3 | 13.3 | 15.7 | 13.5 | 17.8 | 17.4 | 16.6 | 13.7 | 14 | -30.08% |

| 2010 | 15.8 | 20.1 | 24 | 24.6 | 24.4 | 27.1 | 19.8 | 21.5 | 16.7 | 16.6 | 13.4 | 18.3 | 46.23% |

| 2011 | 17.8 | 19.8 | 27.5 | 24.6 | 27.6 | 26.7 | 18 | 21 | 17 | 19.1 | 16.3 | 16.9 | 4.13% |

| 2012 | 18.7 | 24.6 | 28.1 | 27 | 29.1 | 27.5 | 22.9 | 24.5 | 19 | 24.9 | 20.6 | 19 | 13.32% |

| 2013 | 24.4 | 26.1 | 28.9 | 32.1 | 32.5 | 30.9 | 26.2 | 25 | 22.5 | 29.1 | 21.7 | 21.7 | 12.31% |

| 2014 | 25.5 | 30.8 | 33.7 | 33.8 | 35.5 | 32.8 | 28 | 26.4 | 24.9 | 32.3 | 26.3 | 26.7 | 11.09% |

| 2015 | 28.5 | 32 | 36.5 | 38.3 | 33.5 | 33.8 | 27.1 | 27.3 | 28 | 33.8 | 27.3 | 28 | 4.88% |

| 2016 | 31.526 | 35.929 | 40.74 | 40.064 | 37.955 | 40.072 | 28.35 | 35.946 | 33.704 | 38.765 | 34.67 | 32.97 | 15.13% |

| 2017 | 33.859 | 39.428 | 47.579 | 42.295 | 45.853 | ||||||||

As shown above, the number of delivery the first five months of 2017 outstripped the same period in 2016 and is expected to continue outstripping until the end of the year.

Business Outlook by Management

The management anticipates improving demand for plywood from US in year 2017. They believe that the US recreational vehicle sector will continue to grow in the back of recovering US economy. They also have a capital investment program in place to focus on producing different types and sizes of plywood to cater to the needs from the US market. The management intend to install a new peeling machine in 2017 with some modification to other existing machineries to grow its market share in the US RV sector.

Revenue and Cost Structure

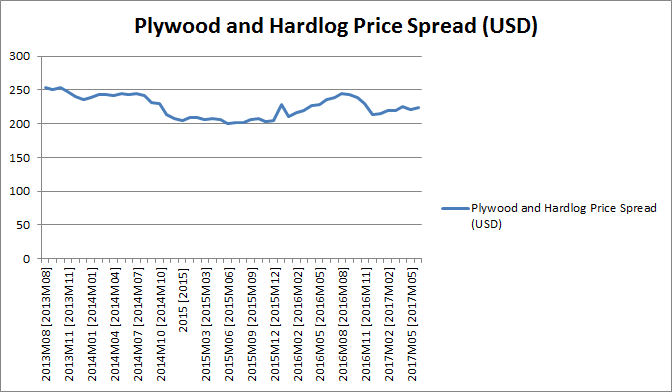

Based on data obtained from World Bank, we can calculate the spread between plywood price and hardlog price (World Bank provided Sarawak hardlog price but in USD so I decided to use USD figures for both plywood and hardlog price) as shown in the following.

Although the plywood price here is for general plywood (Focus Lumber Bhd sells higher quality plywood for niche uses), this can be a reasonable proxy for the performance of the company's pricing margin. Although the spread fell from late last year, it is increasing again and with the ringgit hovering around current levels, the company's performance in 2017 should at least match its performance in 2016.

FCFF Projection

| Financial Performance Analysis | ||||||||||

| Years | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

| Revenue | 113837004 | 114373286 | 102299804 | 120378236 | 122150080 | 132803282 | 147208017 | 150418522 | 180732725 | 201475697 |

| YoY (%) | 0.47% | -10.56% | 17.67% | 1.47% | 8.72% | 10.85% | 2.18% | 20.15% | 11.48% |

| Gross Profit Margin (%) | 20.80% | 20.03% | 26.19% | 26.31% | 27.87% | 23.03% | 24.04% | 25.91% | 31.07% | 26.43% |

| Adjusted EBIT | 8423731 | 10535994 | 11801372 | 7738036 | 12260046 | 7632157 | 11504436 | 13228136 | 26950995 | 20679921 |

| YoY (%) | 25.08% | 12.01% | -34.43% | 58.44% | -37.75% | 50.74% | 14.98% | 103.74% | -23.27% |

| Adjusted EBIT Margin (%) | 7.40% | 9.21% | 11.54% | 6.43% | 10.04% | 5.75% | 7.82% | 8.79% | 14.91% | 10.26% |

| Net cash | 5803028 | 21851257 | 17953092 | 28810477 | 33818985 | 57536491 | 62877603 | 60422335 | 75020204 | 92382420 |

| CAPEX % of Revenue | -3.09% | -5.61% | -4.81% | -4.84% | -1.41% | -1.08% | -1.34% | -1.78% | -2.68% | -0.32% |

*Adjusted EBIT strips out Other Income and one-off transactions

Since the company's performance in 2015 was heavily boosted by a huge decline in Ringgit over USD that provided more pricing advantage, the 5-year average figures are used to reduce the effect of this support in the case of an appreciation of Ringgit.

| Free Cash Flow Projection (5-year average) | Terminal Value | |||||

| Year | 1 | 2 | 3 | 4 | 5 | 6 |

| Revenue | 176651301 | 192002299 | 208687299 | 226822225 | 246533077 | |

| Adjusted EBIT margin | 10% | 10% | 10% | 10% | 10% | |

| Adjusted EBIT | 17665130 | 19200230 | 20868730 | 22682223 | 24653308 | |

| Income Tax rate | 25% | 25% | 25% | 25% | 25% | |

| Adjusted EBIT after tax | 13248848 | 14400172 | 15651547 | 17011667 | 18489981 | |

| Depreciation Expenses | 5248610 | 6354646.5 | 7556797.6 | 8863415.6 | 10283579 | |

| NWC | 32195645 | 34688132 | 37373579 | 40266925 | 43384265 | |

| Growth in NWC | -4811601 | 2492486.6 | 2685447.1 | 2893346.1 | 3117339.9 | |

| CAPEX | -7066052 | -7680092 | -8347492 | -9072889 | -9861323 | |

| FCFF | 16243006 | 10582240 | 12175406 | 13908847 | 15794896 | 210598620 |

| Discount rate | 1.1 | 1.21 | 1.331 | 1.4641 | 1.61051 | 1.771561 |

| NPV | 14766369 | 8745653.2 | 9147562.7 | 9499929.9 | 9807388 | 118877431 |

| Less debt plus cash | 92382420 | |||||

| NPV | 263226754 | |||||

| Number of shares | 103200000 | |||||

| IV per share | 2.5506468 | |||||

Assumptions:

- Revenue grows at 8.69% annually for the next 5 years (8.69% is the CAGR for the past 5 years and this is very conservative as we assume revenue start from a lower level)

- CAPEX to grow at 4% assuming capital goods in the industry becomes more expensive due to greater demand from major wood products exporters (this is again conservative since the company demonstrated growth in revenue while capital expenditure declines as a proportion of revenue)

- Depreciation expenses calculated assuming straight line method of approximately 14%

- Net working capital grows at its 5-year average which is close to the growth in revenue (as the company demonstrated consistent reduction in NWC requirement for the past 10 years)

- WACC of 10% considering this company has no debt with a competent management

- Terminal growth rate of 2.5% similar to inflation rate in Malaysia

At its current price, an investment in this company provides investor with a margin-of-safety approximately around 32.5%.

Shareholding Structure and Compensation

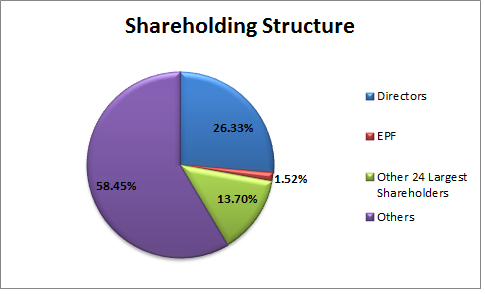

Based on the latest annual report, the only institutional fund holding Focus Lumber Bhd is EPF so a lack of institutional attention can be one reason for its undervaluation (plus analyst reports do not touch on this company that much) but this can be an opportunity since a lack of institutional exit helps support prices. On the other hand, the exit of a super-investor painted the picture of Focus Lumber Bhd's prospects very pessimistically to the extent that its pricefall overshoot but now that this investor exited, price support should be fairly strong. Since the directors (mainly family members and relatives) hold substantial amount of ownership to ensure commitment to the business, the management will maintain its focus in enhancing the business operations and prospects. At 26.33%, that translates 27175780 shares held by the Taiwanese family and its affiliates. Similarly, the compensation for executive directors in 2016 totalled RM1717800 out of a net profit of RM19180504 so this ensures no corporate resources mismanagement while motivating business owners to generate more value for shareholders (even a dividend of 6 cents last year generates similar amount with the compensation).

Multiples

| Multiples | Values |

| Enterprise Value / Adjusted EBIT | 4.22 |

| Price / Earnings *excluding cash | 4.54 |

| Price-to-book | 1.08 |

| EV / FCFF | 6.2 |

At these valuations, the company is very obviously being undervalued by the market. No doubt there are various justifiable causes for these (appreciating Ringgit Malaysia, advanced customer purchases in 2015 and etc.) but with growth prospects intact coupled with healthy balance sheet and competent management, a rational consideration of the company's valuation has to be done again.

Conclusion

As a plywood-player in a niche market in the US added with a competent management, Focus Lumber Bhd. is currently undervalued given the optimistic prospects of the recreational vehicle industry in the US. With internal cash generation ability, the company has been consistently paying dividend while growing its business without acquiring additional debt or equity financing. Given the current valuation, Focus Lumber Bhd is a safe yet rewarding investment idea (since a huge amount of conservativeness has been included) given the undertaker has a longer horizon in mind.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Artemis FA

Has current valuation of BRITE-TECH BERHAD incorporated its rosy future already?

Created by Artemis | Aug 03, 2017

Does Joel Greenblatt's Magic Formula work empirically as preached by Kcchongnz?

Created by Artemis | Aug 01, 2017

Discussions

2 people like this. Showing 11 of 11 comments

FLBHD Research report

http://klse.i3investor.com/m/blog/Investnowlah/128032.jsp

2017-07-17 23:30

Same like Latitude. Directors selfish and not wanting to share the goodies with shareholders. Collecting their huge fees and shareholders left to dry

2017-07-17 23:33

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

Stock Market Enthusiast

Feng Shui Market Outlook for FBM KLCI in the Year of the Wood Snake (2025)

3

The Alpha Trader

5

Stock Market Enthusiast

3 Resilient Stocks That Defied Malaysia’s Market Slump in January 2025 - #GCB, #ABMB, #CDB

7

THE INVESTMENT APPROACH OF CALVIN TAN

REPOSTING: BUSINESSES THAT LAST TILL THE END OF TIME IN BIBLE PROPHECY, Calvin Tan Blog

8

MQ Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

shareinvestor88

Not worth getting stuck here with FLB.

SELL and deploy resources else where in EnE eg Dufu FPG

2017-07-16 17:41