Is Feeding on own flesh legal and healthy? Bursa Cannibal Legalised?

Protasco Bhd dividend in-a-rush on January 2018, a practice of self-cannibal? BizSchool explained.

MH370B

Publish date: Tue, 19 Dec 2017, 06:40 PM

MH370B

0 4

If a PLC conduct self-cannibal, by feeding on own flesh, is it legal and healthy? Gear up loan to pay "salaries and dividend" seems to give impression to investors there is "a lot to eat on table", but is this commercial form of self-gratification? Don't need to ask a master in law. Ask your mother, she may explain better if you shall chew your own finger for dinner.

19 December 2017 - Construction and road maintenance company Protasco Bhd (Bursa 5070) once again announced the date of dividend payout as follows.

First Dividend of 3 sen per share. Kindly be advised of the following :

1) The above Company's securities will be traded and quoted "Ex - Dividend” as from: 9 Jan 2018

2) The last date of lodgment : 11 Jan 2018

3) Date Payable : 26 Jan 2018

Presume the share price of RM1.03 as at 18 December 2017 market closing. The 3 sen dividend seems too good to be true, where off-dividend share price might just be quoted at RM1.00 on 9 January 2018. Any share price above RM1.00 after 9th until 26th January 2018, would be a "profit". Very "generous", wasn't it?

Looking back at Protasco Bhd's past dividend record vs share price performance, the "long-term" investors might have a more sour experience. Protasco Bhd share price has been adjusted down from post-dividend records but sustained lower and lower as seen from the last 12 quarters results. Why is this happening?

There is much fundamental analysis pertaining to Protasco Bhd, which might explain why smart investors do not buy the "fat dividend" illusion story as if Protasco Bhd is very healthy and generous, with an "honest & competent" management team.

"Fat Dividend Cash from where? "

3 sen dividend means about RM13mil cash will be paid out (again). Zoom into the Q3 report, Protasco Bhd cash left about RM11mil, so the shortfall for dividend might be coming from bank overdraft or gearing (as usual). Looking back, Protasco cash Y-to-Y was RM49mil (2016), and the year-earlier was RM110mil (2015). Where the money goes? Number speaks.

The Q3 report shows bank overdraft and financial cost ballooned to over RM37mil and Rm14mil respectively, compared to RM21.7mil and RM5.6mil (2016) on Y-to-Y comparison. Look deeper into the year 2015, would find bank overdraft of RM10.5mil is relatively small compared to Q3 2017.

In summary, Protasco Bhd has been "feeding on own flesh" by borrowing heavily (almost 100% of dividend matches 100% increase of bank borrowing amount), despite the artificial "profits" and misleading public relation using research reports and press releases shown during year 2014-2017 (12 quarters from Sep 2014 - Sep 2017).

" Good News vs Bad News. What is true? "

The company, led by current management after the change of major "controlling" shareholders, twice in the year 2012 and year 2015, had in the last 12 quarters delivered very strange financial results. Here are some key points in layman terms worth notice. Good news or bad news is explained below (source Bursa Malaysia Protasco quarterly & annual reports):

Good ones:

1. majority source of income "still the same" - Road Maintenance.

2. diversify to property development sounds promising.

3. construction very busy with PPA1M.

4. bidding for mega projects and going into Sri Lanka.

5. ED/Deputy-chairman (Dato Sri Chong Ket Pen) and board of directors remain in power.

6. After 10 years, Protasco Bhd still the same - relied on government concession. So as the profit close to RM40mil/year (FY2016 RM44mil PAT) as good as 10 years ago (FY2015 RM41mil PAT)

7. Dividend paid out intensified. 3 sen latest quarter.

8. Cash still positive.

Bad ones:

1. Road Maintenance margin drop to a single digit.

- Protasco strangely divested half of road maintenance company shares to an external party, reason unknown.

- Margin strangely drop to half, reason unknown.

- Divest & margin drop (half and further halved), money whereabout unknown.

2. Property development no income except Public Relation show for 1 director.

- Management (Dato Sri Chong Ket Pen) show face for PR in (Joke) “Superman Grocery Store” and “Parking Hotel” launched in the “Down Syndrome” property project in Kajang.

3. Construction sector booked loss.

- Variation dispute and finance cost not justify.

- Made a loss, and more variation dispute to surface in the next 24 months post-delivery.

4. Megaproject and Sri Lanka with the noisy thunder-cloud news but no rain.

5. 1 ED/Deputy-chairman (Dato Sri Chong Ket Pen) increase salary 400% to over RM4.2 mil per year, while the board of directors taking RM10 mil fees. Up 1,000% compared to a good year when Protasco Bhd was making RM40mil net profit/year.

6. After 10 years, the (current) management track record: losses money in Syria, Libya, China Hainan, Indonesia, and South Africa. 100% screw up rate. Thumbs up. Latest venture into Sri Lanka is questionable. Past record speaks.

7. Dividend derives from Protasco loan (bank overdraft) - is actually eating own flesh.

8. Cash Position is positive but drops to RM11mil vs RM49mil (2016) and RM110mil (2015) same quarter. Earlier, cash was once RM260mil!

More surgical insight, proven that Protasco Bhd after 10 years from IPO, the core business is still "road maintenance business" and "profit" is almost flat ; but the board of directors salaries had skyrocketed. Technically Protasco directors & management is feeding not only on Protasco own flesh, but they are also "civil servants" since road maintenance technically belongs to Malaysian. These huge changes (cash payout to inflated salaries and dividend) raise eyebrows.

1. Protasco still relied on government concession but came with "half & halved" margin. Profit amount (FY2016 RM44mil PAT) same as 10 years ago (FY2005 RM41mil PAT), but "artificially inflated" with low-margin construction numbers, a time bomb yet to surface the next 24 months.

2. ED/Deputy-chairman and the management shows NO improvement yet self-rewarded at the cost of the company by taking higher risk, more cash borrowing, more cash paid out. Why the rush?

3. Cash is technically “deficit” and depleted from RM260mil to RM11mil the same period. Compared to bank overdraft, Protasco is technically “negative” cash position.

4. Bank overdraft shoots up the roof to RM37mil, compared to (2016) of RM21.7mil and (2015) RM10.5mil. The increase almost matches 100% of dividend cash being paid out.

" Feed on own flesh - Legalised self-cannibal? "

If taking into consideration of "director's loan" being the case study in the developed country "Corporate Crime Law", where shareholder cum director gearing up the company to pay money out and eventually ended up in the said director's pocket, is a form of "director loan", why the directors wanted to loot company in such a hurry? Same goes for substantially increased salary, which is a form of self-gratification, having the company results did not actually generate "Free Cash Flow" despite "accounting-profit" on paper. Artificially inflated accounting-profit from construction sector is one of the reasons "bank loan" has to be used to raise cash to pay high salaries and dividend, and the majority of the dividend went to selected controlling shareholders pocket.

The reasons above perhaps answers the minority shareholders questions of why such a "good dividend stock" the share price keep coming down.

" Who Took The Cheese in Protasco? Number Speaks "

Artificially, by pocketing so much money, someone would be very very cash rich, regardless of the company "net profit" is real or not, or the "cash vs bank overdraft" is sustainable or not. The FY2017 Q3 report shows the Cash position is at RM11mil yet Dividend "must be paid out" in exceed of RM13mil. net Profit plunged to just RM21mil combined Q1-Q3, and Q4 "window dressing" likely will push up some profits to buy time until next dividend, or perhaps another 2 more quarters of dividends.

The very question of "what if" the current Executive Director cum controlling shareholders and the management ran away when the sky falls? Is the dividend paid to them be crawled back to pay for "Right Issue" (and dilute your shares)? What if the other way round, when the sky falls the current Executive Director cum controlling shareholders will still be sitting on the sunken ship and suddenly flush with money subscribing to Protasco Bhd cash call exercise, while he will tell newspapers "The Hero Saving Protasco" subscribing to bond or shares? Wonder who dried up Protasco blood in the first place? Would the minority shareholders be diluted and all the years of dividend flushed down the pipe suffering capital (share price) loss?

What if the questionable profits hit with the tax invasion bill, and disappearing "profit margin" paid to "external parties" were captured by MACC or other authorities for transfer pricing or other serious matters? What would be the risk factor costing the company and the minority shareholders if illgotten money were frozen or confiscated?

Until the relevant authorities obtained their Ph.D. from developed countries on how to spot the virus within the system and came up with brilliant measures to protect the minorities, drink your own blood and eat your own flesh is self-declared "legalized" in Bursa Malaysia. Before anything cooking within (the company) shoot off the roof, take your sweet dividend and enjoy the taste of your own blood while you still can.

Maybe this last piece of facts would save you (the minority shareholders) some sleepless nights. Some cash-rich controlling shareholders will use some of the (questionable) cash to buy up Protasco shares. The share price is at least sustained. What a hero and you feel good and confident right? EPF though so, but not Hong Leong Bank. What do you think?

"BizSchool analysis 101"

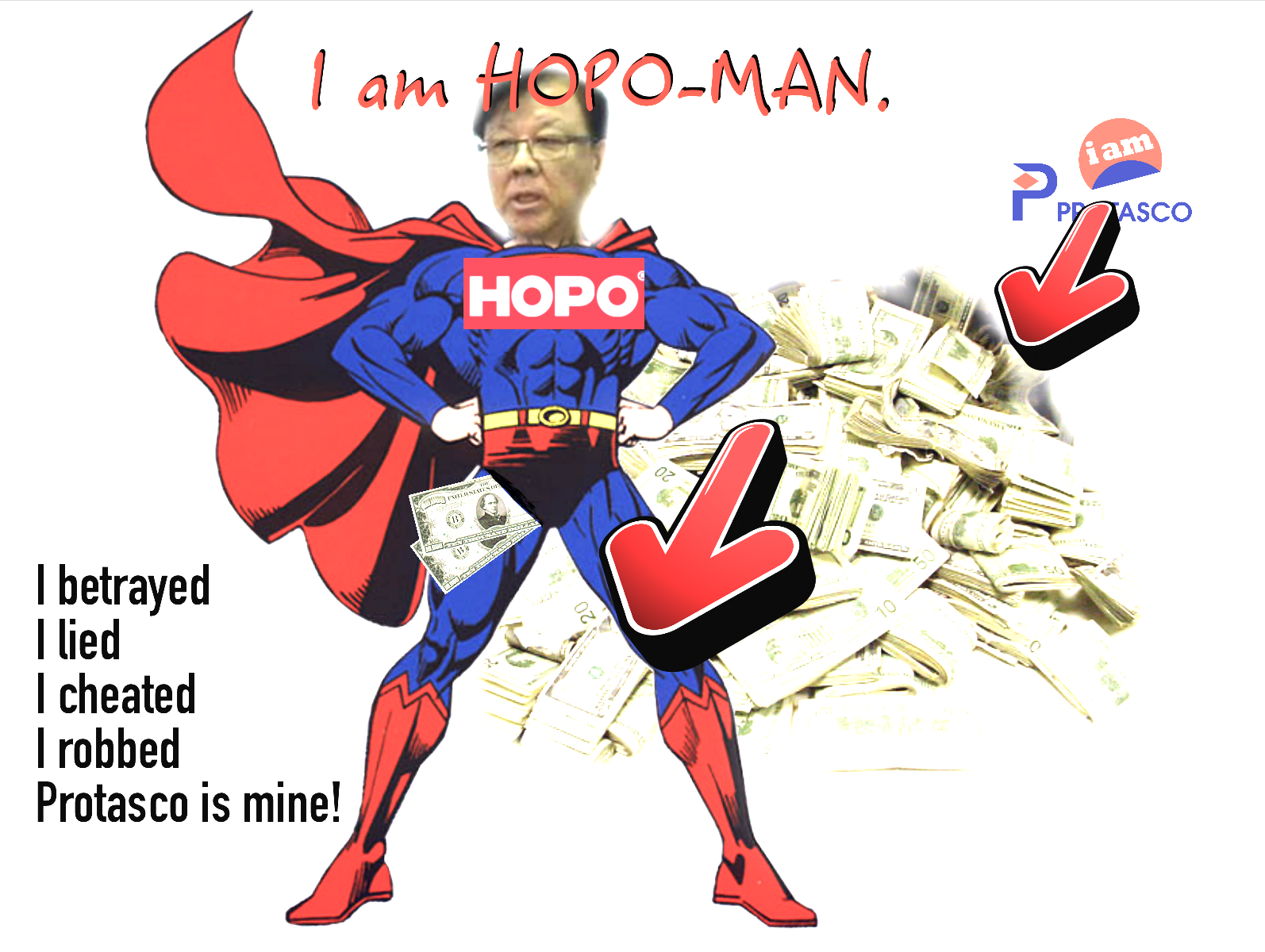

Fresh Today! Without prejudice, a reader sends this interesting wrap-up of "what is happening inside Protasco". With the money flow and annual report publicly published, apparently, it looks like the key suspect Dato Sri Chong Ket Pen is "going after Protasco money for his own benefits". It's all about money after all. What he did to Protasco former controlling shareholders from the year 2012 (1st owner - Tun) and the year 2014 (second owner - Ooi & Tey) before he took full control of Protasco on the year 2014-2017 (today), which intensified his money-depleting scheme under Protasco carpet. Take a wild guess "Who took the people money"?

Here is another example of the typical scheme the suspect Dato Sri Chong Ket Pen did to blame everyone else, to "rationalize" what he did and still doing as of to date - 19 December 2017.

reference source: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5627797

| PROTASCO BERHAD |

First Dividend of 3 sen per share.

Kindly be advised of the following :

1) The above Company's securities will be traded and quoted "Ex - Dividend” as from: 9 Jan 2018

2) The last date of lodgment : 11 Jan 2018

3) Date Payable : 26 Jan 2018

Remarks:- The "zero" par value is arising from the migration to the no par value regime pursuant to the Companies Act 2016, thus par value is no longer relevant

Announcement Info

| Company Name | PROTASCO BERHAD |

| Stock Name | PRTASCO |

| Date Announced | 05 Dec 2017 |

| Category | Listing Circular |

| Reference Number | ILC-05122017-00013 |

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Is Feeding on own flesh legal and healthy? Bursa Cannibal Legalised?

21 Dec17: Protasco Bhd received RM442.68 mil PPA1M project LOA jointly with Kop Mantap Bhd.

Created by MH370B | Dec 21, 2017

Discussions

Be the first to like this. Showing 3 of 3 comments

Clearly a form of stealing money, cheating, embezzlement, and spreading rumors of good news to self justify their wrongdoing. Perfect pirates led by Captain Dato Sri Chong Ket Pen. Endorsed by Bursa Malaysia and Securities Commission. Lolol

2017-12-20 11:57

https://judgement.law.blog

Summary judgemeny on chong ket pen procecution

2018-11-28 07:38

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-26 14:55:00

EMA 5

5 Mins

SELL

2024-07-26 14:50:00

EMA 5

5 Mins

BUY

2024-07-26 14:50:00

ADX

10 Mins

SELL

2024-07-26 14:45:00

ADX

5 Mins

BUY

2024-07-26 14:40:00

ADX

10 Mins

BUY

Apps

Top Articles

1

2

Good Articles to Share

3

M+ Online Research Articles

4

5

MQ Market Updates

6

THE INVESTMENT APPROACH OF CALVIN TAN

7

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Sslee

Dear MH370B,

Just write in to SC aduan@seccom.com.my and make a compliant under Companies Act 2016 Section 131,132 and 133. The MD had already committed an offend under section 131 and be liable to imprisonment for a term not exceeding five year or to a fine not exceeding three million ringgit or to both.

https://www.ssm.com.my/sites/default/files/companies_act_2016/aktabi_20160915_companiesact2016act777_0.pdf

Distribution out of profit

Section: 131.

(1) Subjects to section 132, a company may only make a distribution to the shareholder out of profit of the company available if the company is solvent.

(2) The company, every officer and any other person or individual who contrivance this section commits an offence and shall, on conviction, be liable to imprisonment for a term not exceeding five year or to a fine not exceeding three million ringgit or to both.

Thank you

2017-12-19 20:13