CEO Morning Brief

Analysts Lower Target Prices for Axiata on Wider 3Q Net Loss, Frontier Market Risks

edgeinvest

Publish date: Fri, 01 Dec 2023, 08:52 AM

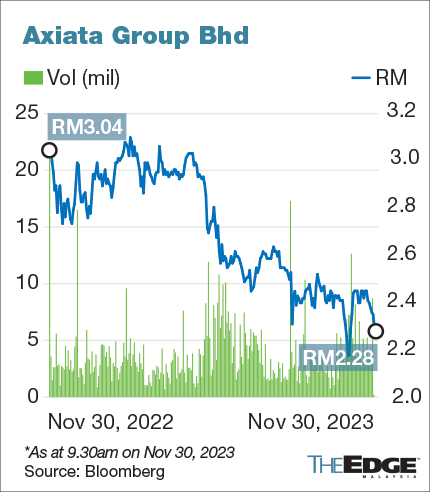

KUALA LUMPUR (Nov 30): Analysts lowered their target prices (TPs) for Axiata Group Bhd, after the telecommunications company’s net loss widened to RM797.41 million for the third quarter ended Sept 30, 2023 (3QFY2023), from RM52.4 million a year ago, mainly due to asset impairment and lower share of results from subsidiary CelcomDigi Bhd.

The impairment of RM1.01 billion during the quarter followed the reclassification of Axiata's Nepal unit Ncell as an asset held for sale, resulting in a widened discontinuing operations loss of RM824.5 million. Quarterly revenue improved to RM5.7 billion, from RM5.37 billion previously.

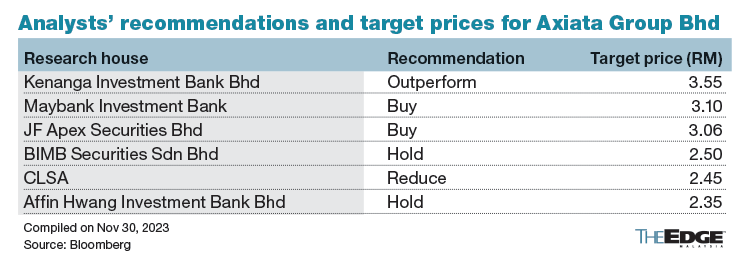

In separate notes on Thursday, TA Securities lowered its TP to RM2.35 (from RM2.80), while Apex Research lowered its TP to RM3.06 (from RM3.27).

TA Securities also downgraded Axiata to “sell” after: i) revising the valuation methodology for Ncell based on its book value; and ii) attaching a higher conglomerate discount of 30% (previously 20%) to reflect the persistent risks associated with Axiata’s investments in its frontier markets.

“Our TP implies an enterprise value/earnings before interest, taxes, depreciation and amortisation (Ebitda) of 6.3 times against forecast calendar year 2024 Ebitda.

“Given the stock’s unfavourable risk-reward potential, we downgrade our recommendation on Axiata to 'sell',” it added.

Meanwhile, Apex Research, which still has a "buy" call on the stock, said Axiata’s core net profit of RM255.2 million for the cumulative nine months ended Sept 30, 2023 was below house expectations, due to higher depreciation, interest cost and lower contributions from CelcomDigi.

The research house said that in view of the challenging outlook, Axiata has decided to exit Nepal, and reclassified Ncell as an asset held for sale.

To recap, Axiata bought a 80% stake in Ncell for RM5.9 billion in 2016, and was slapped with a capital gains tax of RM785 million in 2019.

The research house reduced its FY2023 earnings forecast for Axiata by 33% to adjust for the reclassification of Ncell as an asset for sale.

“We maintain our 'buy' recommendation, with a lower TP of RM3.06 (previously RM3.27), after reducing our sum-of-parts valuation of Ncell.

“Axiata continues to face geopolitical, macroeconomic and regulatory risks, as well as a strengthening US dollar and rising interest rates,” it said.

Read also:

Axiata’s 3Q loss widens on impairments, lower CelcomDigi contribution

Source: TheEdge - 1 Dec 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-07-26

AXIATA2024-07-26

AXIATA2024-07-26

AXIATA2024-07-25

AXIATA2024-07-25

AXIATA2024-07-25

AXIATA2024-07-24

AXIATA2024-07-24

AXIATA2024-07-24

AXIATA2024-07-24

AXIATA2024-07-24

AXIATA2024-07-23

AXIATA2024-07-23

AXIATA2024-07-23

AXIATA2024-07-22

AXIATA2024-07-22

AXIATA2024-07-22

AXIATA2024-07-22

AXIATA2024-07-19

AXIATA2024-07-19

AXIATA2024-07-19

AXIATA2024-07-18

AXIATA2024-07-18

AXIATA2024-07-18

AXIATA2024-07-18

AXIATA2024-07-16

AXIATA2024-07-16

AXIATA2024-07-16

AXIATAMore articles on CEO Morning Brief

JAKS Resources Inks Land Lease MOU With TDM Unit for LSS5 Project

Created by edgeinvest | Jul 26, 2024

Meta to be Hit With First EU Antitrust Fine for Linking Marketplace and Facebook — Reuters

Created by edgeinvest | Jul 26, 2024

Apple's China Market Share Shrinks as Huawei Surges, Data Shows

Created by edgeinvest | Jul 26, 2024

Insured Losses From CrowdStrike Outage Could Reach US$1.5b, CyberCube Says

Created by edgeinvest | Jul 26, 2024

Thailand Car Production Drops Sharply in June, Local Sales Fall

Created by edgeinvest | Jul 26, 2024

Hyundai Motor Posts Record 2Q Profit on Strong US Sales, to Boost Hybrid Lineups

Created by edgeinvest | Jul 26, 2024

UK Mortgage Rate Surge Pushed 320,000 Into Poverty, Report Shows

Created by edgeinvest | Jul 26, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-26 16:05:00

ADX

5 Mins

SELL

2024-07-26 16:00:00

OBV

10 Mins

SELL

2024-07-26 15:50:00

ADX

10 Mins

SELL

2024-07-26 15:50:00

EMA 5

5 Mins

SELL

2024-07-26 15:30:00

ADX

10 Mins

BUY

Apps

Top Articles

1

BFM Podcast

2

MQ Market Updates

3

BFM Podcast

4

BFM Podcast

5

PublicInvest Research

6

BFM Podcast

7

8

M+ Online Research Articles

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....