CEO Morning Brief

Shadow Banking Stress in South Korea Sends Warning to Global Investors

edgeinvest

Publish date: Wed, 24 Apr 2024, 09:43 AM

(April 23): South Korea is emerging as a closely watched weak link in the US$63 trillion (RM298.95 billion) world of shadow banking.

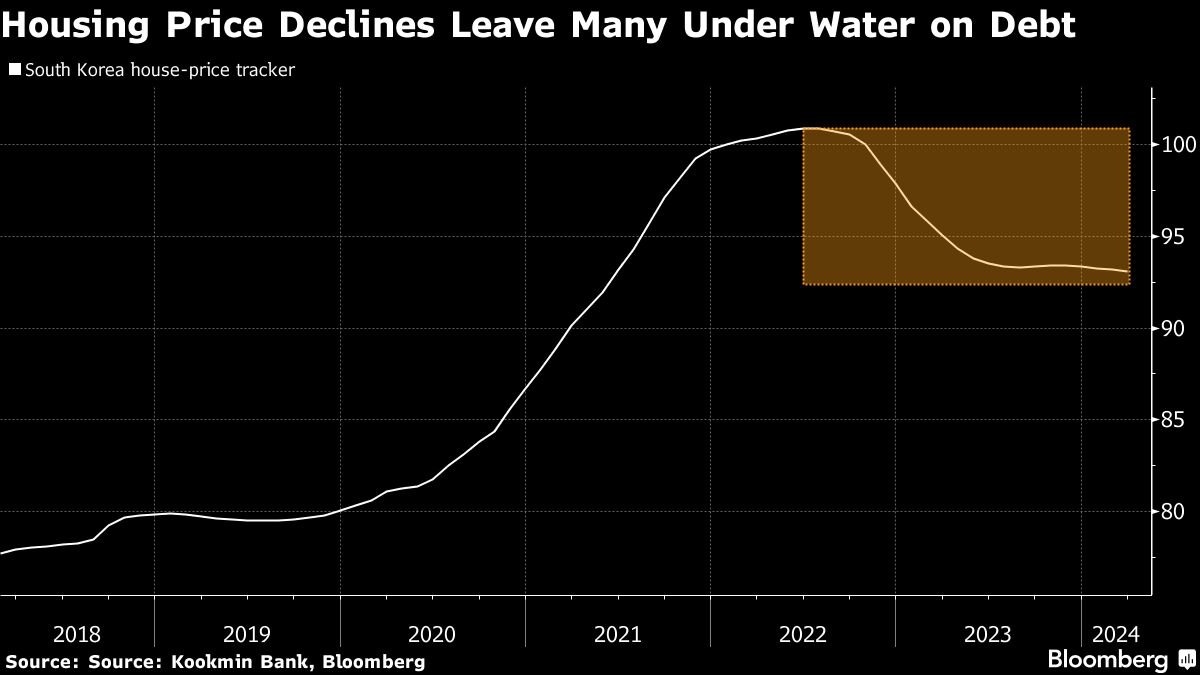

Real estate exposure has been showing cracks at home and abroad after interest rates rose, prompting financial firms including T Rowe Price Group Inc and Nomura Holdings Inc to express concern about stress in shadow loans to the sector.

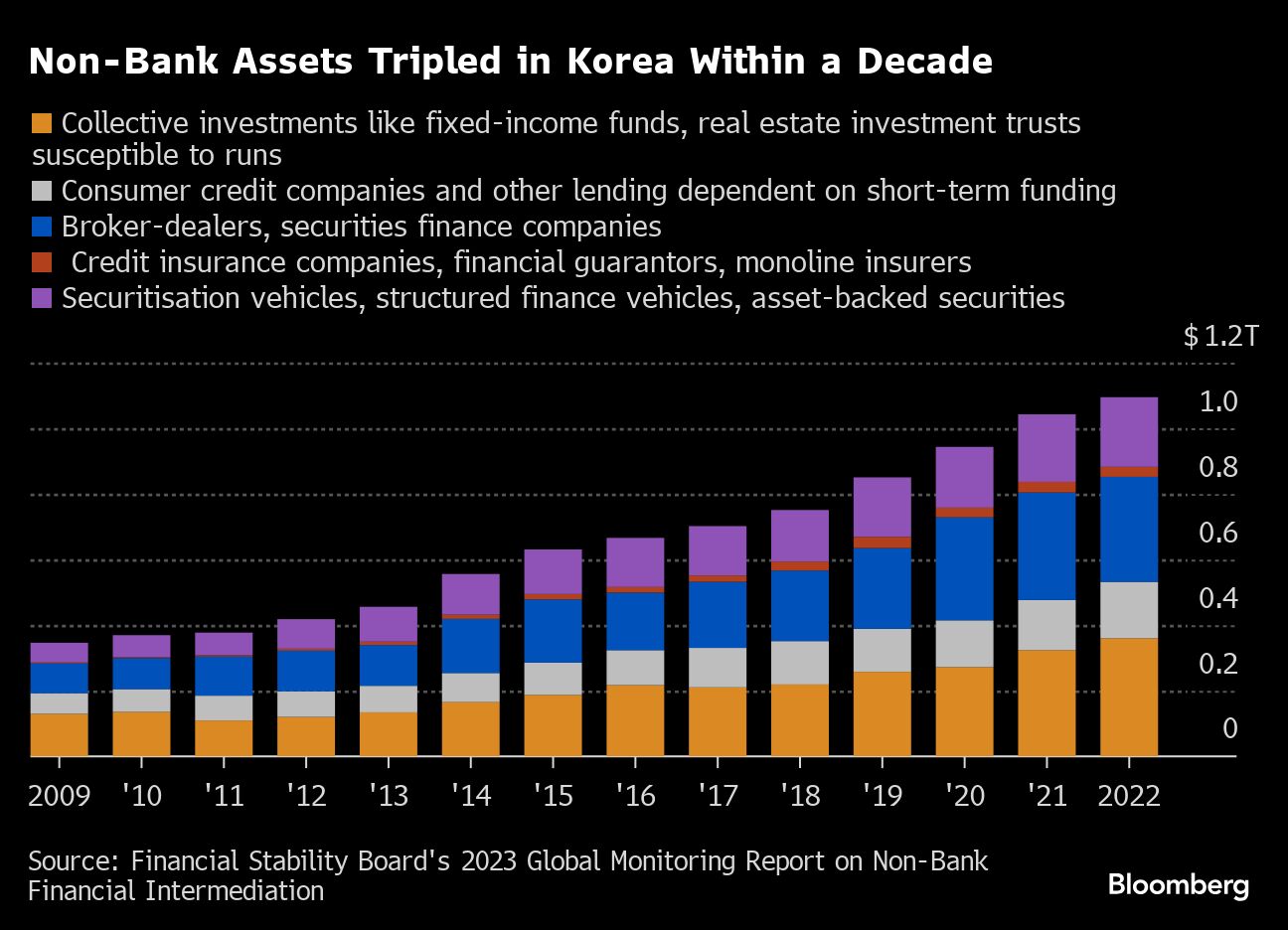

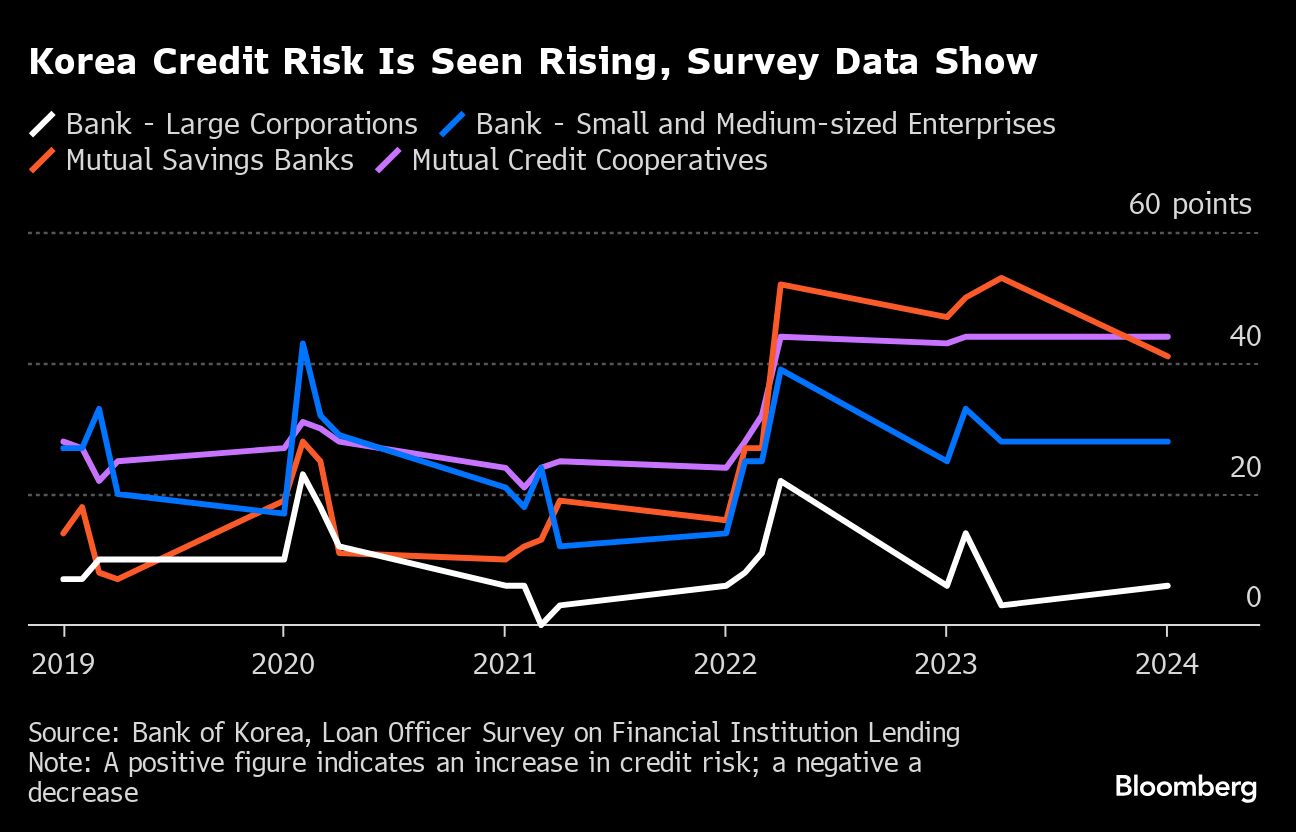

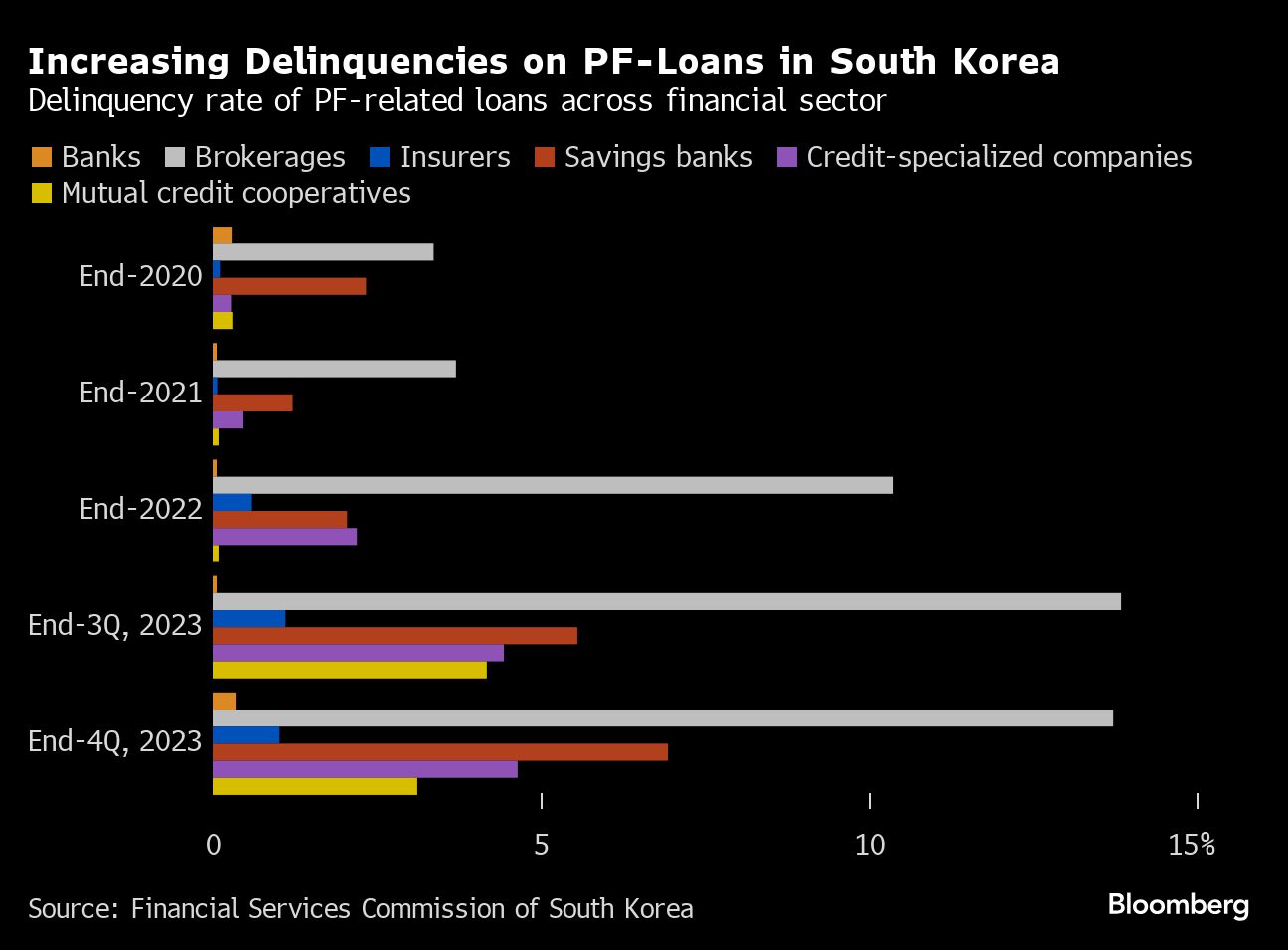

Delinquency rates at one key group of Korean lenders nearly doubled to 6.55% last year, while economists at Citigroup Inc estimate 111 trillion won (RM385.11 billion) of project-finance debt is “troubled.” Korean shadow-bank financing to the real estate sector rose to a record 926 trillion won last year, over four times a decade ago, data from the Korea Capital Market Institute show.

Policymakers stemmed contagion risks by expanding certain loan guarantees, but a shock restructuring announcement late last year by builder Taeyoung Engineering & Construction Co underscored the threat of flareups. The firm will need a debt-to-equity swap of about one trillion won to erase capital impairments, its largest creditor said last week.

Such restructurings stand to worsen strains among shadow banks — as non-bank lenders are often called. The part of that sector with activities that may pose stability risks is large compared with other advanced economies, and is second only to the US in relative size, according to data from the Financial Stability Board.

“What is happening in Korea is probably a microcosm of what could be happening elsewhere,” said Quentin Fitzsimmons, a global fixed-income portfolio manager at T Rowe Price Group Inc. “It has made me concerned.”

Shadow-bank lending, which includes what is typically termed private credit, grew quickly in the aftermath of the 2008 financial crisis as banks pulled back from risky loans, prompting smaller and less profitable businesses to turn to alternative sources.

The challenges of refinancing such borrowings rose to the fore after the Bank of Korea became one of the first major central banks to raise interest rates in 2021. Of course, Korea is now far from the only economy dealing with the unintended consequences of higher financing costs. The default rate on US leveraged loans topped 6% for the first three months of 2024 and spreads on the riskiest European junk bonds recently widened to the most since early in the pandemic.

But in Korea, the extent of the concern can be seen in the rapidity of the policy response. An official at Korea’s financial watchdog, the Financial Supervisory Service, said earlier this month that the organisation may conduct on-site inspections of saving banks after evaluating loan delinquencies for the first quarter.

South Korean President Yoon Suk Yeol suffered a loss in a parliamentary election earlier this month, but with the polls at least out of the way, authorities may have freer rein to refocus on cleaning up soured loans.

“The government will speed up restructuring” in the property sector, said Jeong Woo Park, an economist at Nomura Holdings Inc. “Taeyoung’s debt work-out isn’t the end, but it is likely the beginning of project-finance debt stress.”

Still, overall credit risks haven’t sparked broader economic damage, in contrast to China. An unprecedented real estate slump there has fueled more than US$130 billion of bond defaults and persistent deflation. It also led shadow lender Zhongzhi Enterprise Group Co to file for bankruptcy this year.

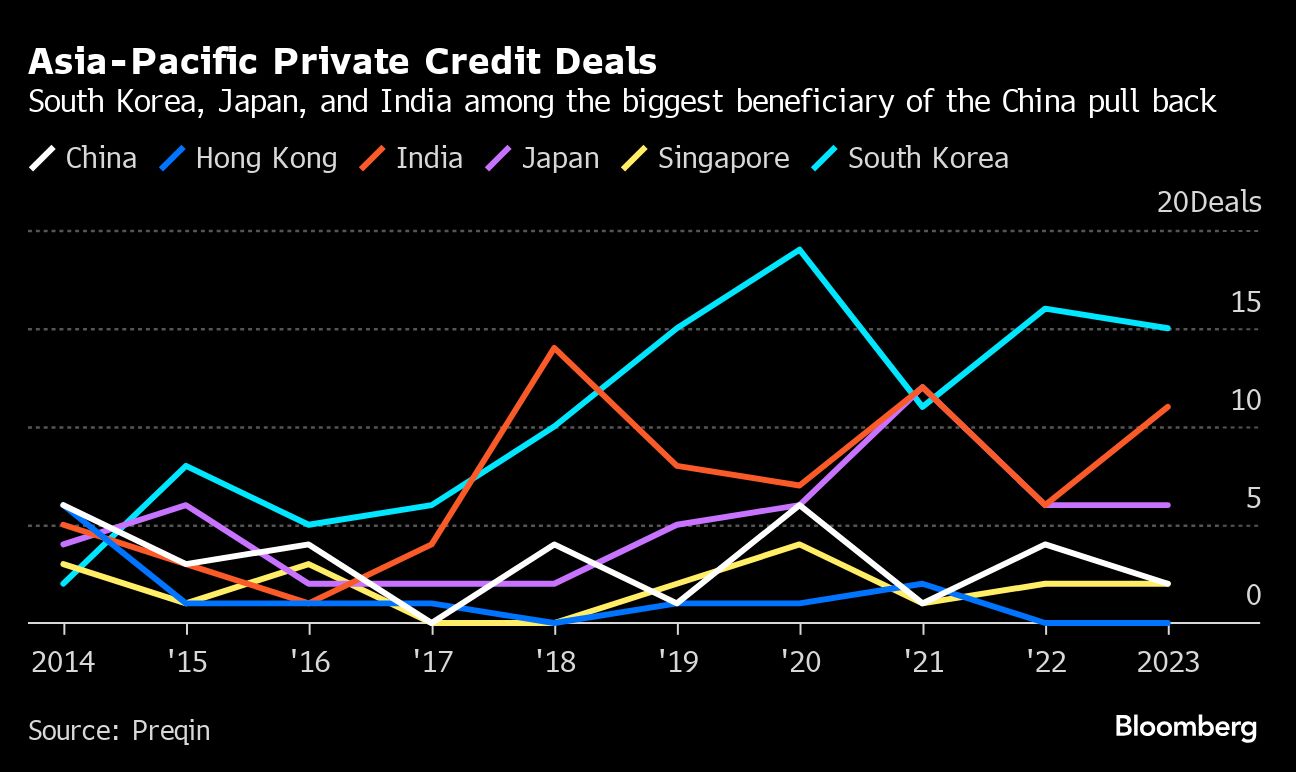

Many private lenders spooked by such risks in China have considered channelling money elsewhere in Asia including Korea. KKR & C., for example, signed a deal to lend US$40 million to property firm Innovalue earlier this year.

But the worst from Korea’s property malaise is likely yet to come. Citigroup economist Jin-Wook Kim reiterated the bank’s view this month that restructuring of project finance debt will slow economic growth in the second half to 0.2% in their base case scenario.

Project finance loans — a kind of short-maturity debt — became popular with developers after the Asian financial crisis in 1997 when South Korea requested an International Monetary Fund bailout.

The practice of using such funding gained momentum during the years of low rates and rising property values. Brokerages got in on the action by securitising such loans and selling them on to money-market investors.

But they have become a common thread through the recent scares.

The first signs of trouble in Korean credit markets emerged about 19 months ago, when the developer of a Legoland amusement park to the northeast of Seoul missed payment on project finance loans, triggering the biggest local run-up in short-term debt yields since the global financial crisis. Then, in July last year, fears about ill-timed real estate bets forced a branch of a non-bank lender, one of Korea’s biggest credit unions, to shut.

Korean authorities have so far managed to limit the pain. After Taeyoung, they promised to expand a US$66 billion stabilisation package if needed to limit the spillover. Last month, the government backed up those pledges with billions of dollars of additional support.

“They are managing the risks but it has to be monitored closely,” Krishna Srinivasan, the International Monetary Fund’s director of the Asia and Pacific Department, told Bloomberg. “Some of the smaller institutions could be at risk.”

Policymakers can ill afford a steep drop in property prices that might exacerbate bad loans and hurt the economy, as happened in Japan in the 1990s.

Korea’s non-bank lenders have made large investments in overseas commercial real estate in the past decade, lured by favourable exchange rates and the perception — common until the pandemic — that offices, with their long-term leases, provided safe returns.

Many of those assets suffered in the post-Covid slump. Hana Alternative Asset Management’s investment in London’s No 1 Poultry retail-and-office property is an example.

Threats are most acute for smaller lenders of the type that, at least in Asia, are often considered part of the private credit market.

“Given the government’s intention to restructure some of the weak performing development sites, we think some of the smaller and non-bank financial institutions are more vulnerable,” said Matt Choi, director of Asia-Pacific Financial Institutions at Fitch Ratings.

Source: TheEdge - 24 Apr 2024

More articles on CEO Morning Brief

JAKS Resources Inks Land Lease MOU With TDM Unit for LSS5 Project

Created by edgeinvest | Jul 26, 2024

Meta to be Hit With First EU Antitrust Fine for Linking Marketplace and Facebook — Reuters

Created by edgeinvest | Jul 26, 2024

Apple's China Market Share Shrinks as Huawei Surges, Data Shows

Created by edgeinvest | Jul 26, 2024

Insured Losses From CrowdStrike Outage Could Reach US$1.5b, CyberCube Says

Created by edgeinvest | Jul 26, 2024

Thailand Car Production Drops Sharply in June, Local Sales Fall

Created by edgeinvest | Jul 26, 2024

Hyundai Motor Posts Record 2Q Profit on Strong US Sales, to Boost Hybrid Lineups

Created by edgeinvest | Jul 26, 2024

UK Mortgage Rate Surge Pushed 320,000 Into Poverty, Report Shows

Created by edgeinvest | Jul 26, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

save malaysia!

3

BFM Podcast

4

BFM Podcast

6

BFM Podcast

7

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....