CEO Morning Brief

Baidu’s Robotaxi Ambition Draws Sceptics After Brief Stock Rally

edgeinvest

Publish date: Thu, 25 Jul 2024, 09:35 AM

Baidu Inc has announced an expansion into ride hailing with a fleet of fully self-driving cars in the city of Wuhan.

(July 24): China’s faster-than-expected adoption of autonomous driving is doing little to rev up optimism among analysts searching for Baidu Inc’s next catalyst.

The internet search leader’s shares have almost erased gains notched in Hong Kong this month after the company announced an expansion into ride hailing with a fleet of fully self-driving cars in the city of Wuhan. Now, Baidu’s stock may extend its year-to-date decline, with analysts cutting its average 12-month target price to an all-time low.

“The stock price has not priced in robotaxi potential. But to be honest, it shouldn’t right now either, because no one really knows how successful it will be, nor do they know about future government policy towards the technology,” said Kai Wang, a Morningstar analyst. “Mass commercialisation is still like three to five years away.”

Of concern is whether Baidu’s new growth plans will be able to offset its weak advertising revenues fast enough, particularly given a lack of certainty around pending regulations or consumer demand for such products. Market competition and a weak macro environment may also weigh on the stock.

It wasn’t supposed to be this way. Autonomous driving and machine learning have been core tenets in Baidu’s broader ambitions to expand within the artificial intelligence (AI) sector. Its autonomous ride-hailing arm “Apollo Go” launched a cheap robotaxi model in May, and aims to be profitable by next year. Baidu is also expanding this service beyond Wuhan to more Chinese cities. The company in April signed an agreement with Tesla Inc to embed its maps into the automaker’s self-driving systems.

Yet that hasn’t been enough to sway market watchers. Bloomberg Intelligence analyst Robert Lea wrote in a note last month that Baidu was likely to lose market share in AI due to a price war, and its earnings might “undergo a double-digit sequential decline this year with its AI ventures continuing to lose money”.

On robotaxis in particular, a case study of operations in Shanghai unveiled “discouragingly deep loss-making financials”, JPMorgan Chase & Co analysts including Alex Yao wrote in a report this month. Discounts offered by Baidu make the strategy commercially unviable, they added.

Those concerns have forced at least seven brokers, including Goldman Sachs Group Inc and Morgan Stanley, to slash their target prices over the past two weeks.

There may be other headaches too. Baidu’s operations in Wuhan are under increasing scrutiny, with local media citing concerns including the rising unemployment of taxi drivers and the safety of those cars in more complicated traffic situations.

Still, given China’s driverless ride-hailing market potential, Baidu’s growth plans may still be a win in the long term. The country currently has about four to five million ride-railing cars in operation, according to Goldman Sachs. If 5% of those cars can switch into self driving vehicles and offer similar pricing to normal taxis, that translates into a US$5 billion (RM23.37 billion) market, it said.

At least six cities or provinces recently announced trials to promote autonomous driving over the past month, which may help grow demand.

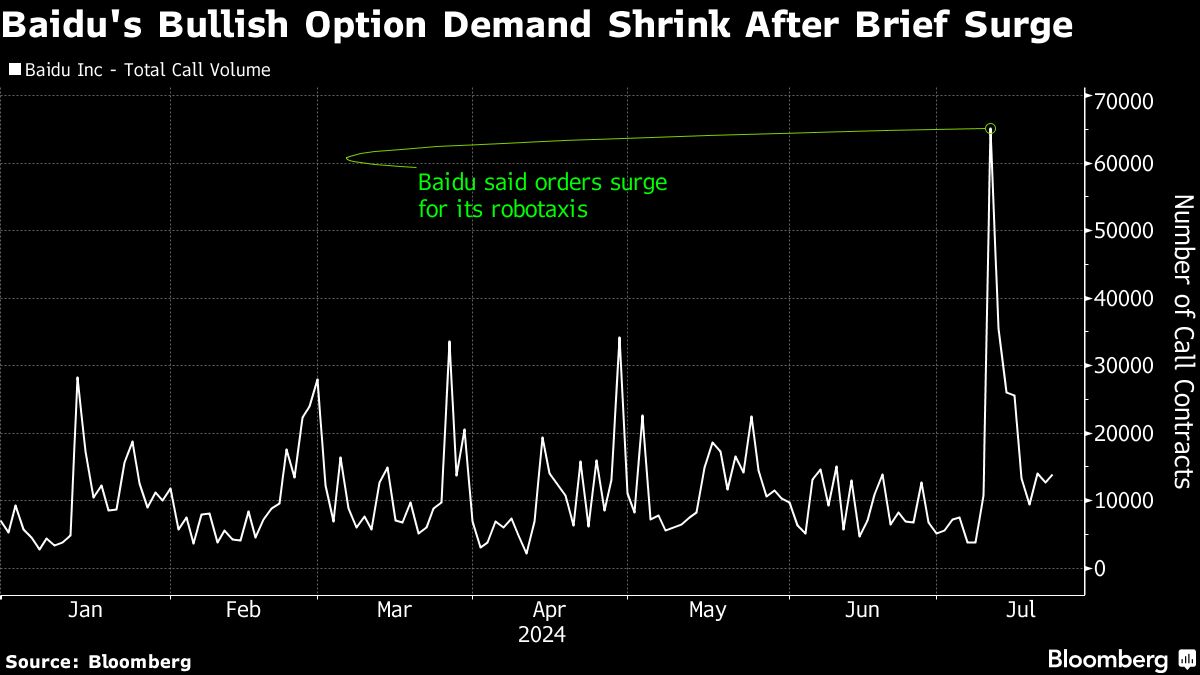

For now, the next catalyst will likely come during the firm’s earnings next month. Baidu is expected to report a 1.2% growth in revenue for the second quarter, similar to the pace in the March period, which was the slowest since 2022, according to data compiled by Bloomberg. And after a short spike in demand for bullish option contracts when the company announced its expansion in Wuhan, trading volume has quickly come down.

“Robotaxis are unlikely to generate any significant revenue or earnings for Baidu over the next few years,” Bloomberg Intelligence’s Lea said, adding that its earnings might show a double-digit sequential decline this year. “The technology is high-risk and remains in an immature stage, with developmental hurdles yet to overcome.”

Uploaded by Tham Yek Lee

Source: TheEdge - 25 Jul 2024

More articles on CEO Morning Brief

JAKS Resources Inks Land Lease MOU With TDM Unit for LSS5 Project

Created by edgeinvest | Jul 26, 2024

Meta to be Hit With First EU Antitrust Fine for Linking Marketplace and Facebook — Reuters

Created by edgeinvest | Jul 26, 2024

Apple's China Market Share Shrinks as Huawei Surges, Data Shows

Created by edgeinvest | Jul 26, 2024

Insured Losses From CrowdStrike Outage Could Reach US$1.5b, CyberCube Says

Created by edgeinvest | Jul 26, 2024

Thailand Car Production Drops Sharply in June, Local Sales Fall

Created by edgeinvest | Jul 26, 2024

Hyundai Motor Posts Record 2Q Profit on Strong US Sales, to Boost Hybrid Lineups

Created by edgeinvest | Jul 26, 2024

UK Mortgage Rate Surge Pushed 320,000 Into Poverty, Report Shows

Created by edgeinvest | Jul 26, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

save malaysia!

3

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....