The Citta way of stock investment

SYF RESOURCES BHD, Transformation from Furniture to Property Development

| SYF RESOURCES BHD Right management, Right direction and ALL Right! |

Introduction

The Company’s business segments:

a. Furniture(dining set and bedroom set)

b. particle board

c. Property

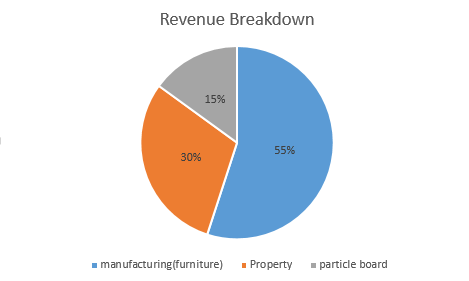

From the figures above, we can notice that Furniture remains the major source of revenue, follow by property and board. Furniture sales is mainly focused on domestic 2/3, export 1/3. The devaluation of Ringgit didn't help much for this SYFy because I expect a slow down in sales both domestic and export. Moreover, Syf furniture pattern is very old fashion and lack of competitive advantage. I expect a 5%-10% gradually decreases in manufacturing line for a continuition of 3 years. Overall, for manufacturing business, it's consider 'stable' because this do not affect much to the company since property devepment is growing well. Besides, the Particle Board production is performaning very well in recently years. Contribution from this segment has a double digits growth, from Rm14,747m to Rm33,233. The new invested machines has started its operation and expect a higher increase in production. This help to offset the slowndown in furniture business, revenue remains stable or maybe slightly increase in revenue.

Basically, the management and board of directors are noticed above the difficulty of furniture business and they are doing a very good job through diversification into other businesses(property and board).

On the other hand, housing market is slowing down after a few years of bull run. But, this will not have impact to SYF for two reasons.

1. Kiara Plaze Semenyih a combined of shoplots, Soho and service aprtment was fully sold out. This is contributing significant revenue and profit to SYF quartely upon the percentage of their vontruction finishing. This will easily help SYF double up its FY2016 revenue for sure!

2. SYF is planning to start its joint venture property development in sungai long in beginning of 2016. Sg.Long has become a very hot area after UTAR Setapak moved to UTAR Sg. Long. The number of students have increased double and rental cost increased significantly. I expect SYF will also easy sell off all their units once the project launch.

Since the manufacturing is remains stable, property deveopment segment growing stronger, we could see skyrocketing quartely results in 2016. I believe SYF still has more room to grow in 2016 and 2017.

Previously, SYF was a quiet counter, trading at low volume. But, this stocks has started to gain attention from the public since December, volume spike and stock prices trending higher and higher. SYF could be one of the best performaning stock in 2016 support by its growth prospect.

By comparison, I prefer warrant rather than mother because of its higher % of return for each bit. Although SYF is a small cap counter, but the risk for this stock is low. I suggest buy on weakness.

Article News :SYF (for reference)

I bought this stock one year ago. Since this is my first post, just show some of my holding stocks.

Wish all Happy New Year, and all the best in 2016!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Discussions

3 people like this. Showing 8 of 8 comments

Have you not heard the saying that when others are fearful we should be greedy. Property always pays better margin. Moreover people already fear for so long, isn't it there should be a turn of fend suitable. It is never feel enough to own only one house.

2016-01-01 13:04

Syf is a very small cap company and they just have 2 development projects currently, meanwhile locations are all very strategic, I believe Syf has no problem on this issue. Even few years back, Syf is managed to sold off all their new develop factory units in Sg.lalang semenyih, this is amazing. Btw, Syf has become smart, they pass all their property projects to sub-sales company (Gs Reality) and they have a lot of agents around selangor/klang valley. If you are still lack of confident, i suggest u should come to sg.long for a visit.

2016-01-02 11:49

for furniture sales, they were doing good in US market where goods shipped from their Klang factory..95% products from tis factory shipped to US and recent 1 year each month capacities were fully occupied due to good recovery of US economies..

2016-01-04 11:32

Hopefully this could sustain in 2016, but logical thinking U.S interest rate hike, this could reduce their purchasing power and expenditure on goods. Btw, SYF's managements did mentioned that they will adjust the prices, so we could not expect much on this. But I got 100% faith on development segment.

2016-01-04 23:28

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-17 15:00:00

ADX

10 Mins

SELL

2024-07-17 14:30:00

ADX

5 Mins

SELL

2024-07-17 12:25:00

EMA 5

5 Mins

SELL

2024-07-17 12:25:00

MACD/RSI

5 Mins

SELL

2024-07-17 12:20:00

EMA 5

10 Mins

SELL

Apps

Top Articles

1

The Alpha Trader

2

Bursa Stock Musings - Thoughts & Ideas

PGF Capital - insti shareholding up from 5% to 14%! (part 1)

3

南洋行家论股

4

How to become a resilient trader

5

RHB Investment Research Reports

7

Koon Yew Yin's Blog

8

BreakingOut

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

apini

Well done

Your patience had rewarded you 63% gain

Hope you will gain another 37 to make it 100%

Hahaha..

Happy new year

2016-01-01 12:53