One of the classes that I teach is on investment philosophies, where I begin by describing an investment philosophy as a set of beliefs about how markets work (and sometimes don't) which lead to investment strategies designed to take advantage of market mistakes. Unlike some, I don't believe that there is a single "best" philosophy, since the best investment philosophy for you is the one that best fits you as a person. It is for that reason that I try to keep my personal biases and choices out, perhaps imperfectly, of the investment philosophies, and use the class to describe the spectrum of investment philosophies that investors have used, and some have succeeded with, over time. I start with technical analysis and charting, move on to value investing, then on to growth investing, and end with information trading and arbitrage. The most common pushback that I get is from old-time value investors, arguing that there is no debate, since value investing is the only guaranteed way of winning over the long term. Embedded in this statement are a multitude of questions that deserve to be answered:

- What is value investing and what do you need to do to be called a value investor?

- Where does this certitude that value investing is the "winningest" philosophy come from? Is it deserved?

- How long is the long term, and why is it guaranteed that value investing wins?

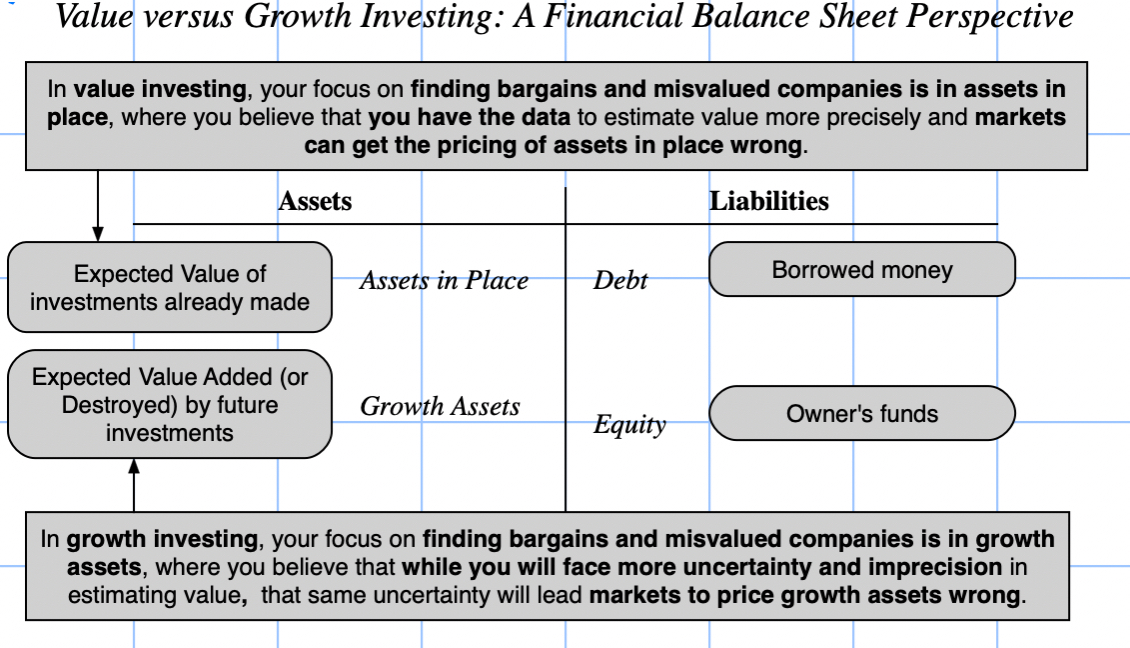

What is value investing?

Given how widely data services tracking mutual funds and active investing seem to be able classify funds and investors into groupings. how quickly prognosticators are able to pass judgment on value investing's successes and failures and how much academics have been able to write about and opine on value investing in the last few decades, you would think that there is consensus now on what comprises value investing, and how to define it. But you would be wrong! The definition of value investing varies widely even among value investors, and the differences are not often deep and difficult to bridge.

In this section, I will start by providing three variants on value investing that I have seen used in practice, and then go on to explore a way to find commonalities.

- Lazy Value Investing: Let's start with the easiest and most simplistic definition, and the one that many data services and academics continue to use, simply because it is quantifiable and convenient, and that is to base whether you are a value or growth investor on whether the stocks you buy trade at low or high multiples of earnings or book value. Put simply, if you consistently invest in stocks that trade at low PE and low price to book ratios, you are a value investor, and if you do not, you are not one.

- Cerebral Value Investing: If you use the lazy definition of value investing as just buying low PE and low PBV stocks with a group of Omaha-bound value investors, you will get pushback from them. They will point to value investing writing, starting with Graham and buffered by Buffett's annual letters to shareholders, that good value investing starts by looking at cheapness (PE and PBV) but also includes other criteria such as good management, solid moats or competitive advantages and other qualitative factors.

- Big Data Value Investing: Closely related to cerebral value investing in philosophy, but differing in its roots is a third and more recent branch of value investing, where investors start with the conventional measures of cheapness (low PE and low PBV) but also look for additional criteria that has separated good investments from bad ones. Those criteria are found by poring over the data and looking at historical returns, a path made more accessible by access to huge databases and powerful statistical tools.

- Passive Value Investing: In passive value investing, you screen for the best stocks using criteria that you believe will improve your odds. Once you buy these stocks, you are asked to be patient, and in some cases, to just buy and hold, and that your patience will pay off as higher returns and a more solid portfolio. To see this approach play out, at least in the early days of value investing, take a look at these screens for good stocks that Ben Graham listed out in 1939 in his classic book on the intelligent investor. These screens have evolved in the years since, in two ways. The first is with the introduction of more qualitative screens, like "good" management, where notwithstanding attempts to measure goodness, there will be disagreements. The second is to use increased access to data, both from the company and about it, to both test existing screens and to add to them.

- Contrarian Value Investing: In contrarian value investing, you focus your investing energies on companies that have seen steep drops in stock prices, with the belief that markets tend to overreact to news, and that corrections will occur, to deliver higher returns, across the portfolio. Within this approach, access to data has allowed for refinements that, at least on paper, deliver higher and more sustained returns.

- Activist Value Investing: In activist value investing, you target companies that are not only cheap but badly run, and then expend resources (and you need a considerable amount of those) to push for change, either in management practices or in personnel. The payoff to activist value investing comes from activist investors being the catalysts for both price change in the near term, as markets react to their appearance, and to changes in how the company is run, in the long term.

- Minimalist Value Investing: There is a fourth approach to value investing that perhaps belongs more within passive investing, but for the moment, I will set it apart. In the last decade or two, we have seen the rise of titled index funds and ETFs, where you start with an index fund or ETF, and tilt the fund/ETF by overweighting value stocks (high PE/PBV, for instance) and underweighting non-value stocks.

Is value investing the winningest philosophy?

While it is not uncommon for investors of all stripes to express confidence that their approach to investing is the best one, it is my experience that value investors express not just confidence, but an almost unquestioning belief, that their approach to investing will win in the end. To see where this confidence comes from, it is worth tracing out the history of value investing over the last century, where two strands, one grounded in stories and practice and the other in numbers and academic, connected to give it a strength that no other philosophy can match.

The Story Strand

When stock markets were in their infancy, investors faced two problems. The first was that there were almost no information disclosure requirements, and investors had to work with whatever information they had on companies, or on rumors and stories. The second was that investors, more using to pricing bonds than stocks, drew on bond pricing methods to evaluate stocks, giving rise to the practice of paying dividends (as replacements for coupons). That is not to suggest that there were not investors who were ahead of the game, and the first stories about value investing come out of the damage of the Great Depression, where a few investors like Bernard Baruch found a way to preserve and even grow their wealth. However, it was Ben Graham, a young associate of Baruch, who laid the foundations for modern value investing, by formalizing his approach to buying stocks and investing in 1934 in Security Analysis, a book that reflected his definition of an investment as "one which thorough analysis, promises safety of principal and adequate return". In 1938, John Burr Williams wrote The Theory of Investment Value, introducing the notion of present value and discounted cash flow valuation. Graham's subsequent book, The Intelligent Investor, where he elaborated his more developed philosophy of value investing and developed a list of screens, built around observable values, for finding under valued stocks.

While Graham was a successful investor, putting many of his writings into practice, I would argue that Graham's greater contribution to value investing came as a teacher at Columbia University. While many of his students have acquired legendary status, one of them, Warren Buffett has come to embody value investing. Buffett started an investment partnership, which he dissolved (famously) in 1969, arguing that given a choice between bending his investment philosophy and finding investments and not investing, he would choose the latter. These words, in his final letter to partners in May 1969, more than any others have cemented his status in value investing: "I just don't see anything available that gives any reasonable hope of delivering such a good year and I have no desire to grope around, hoping to "get lucky" with other people's money. He did allow his partners a chance to receive shares in a struggling textile maker, Berkshire Hathaway, and the rest, as they say, is history, as Berkshire Hathaway morphed into an insurance company, with an embedded closed end mutual fund, investing in both public and some private businesses, run by Buffett. While Buffett has been generous in his praise for Graham, his approach to value investing has been different, insofar as he has been more willing to bring in qualitative factors (management quality, competitive advantages) and to be more active (taking a role in how the companies he has invested in are run) than Graham was. If you had invested in Berkshire Hathaway in 1965 or soon after, and had continued to hold through today, you would be incredibly wealthy:

|

| Source: Berkshire Annual Report for 2019 (with a Sept 2020 update) |

The numbers speak for themselves and you don't need measures of statistical significance to conclude that these are not just unusually good, but cannot be explained away as luck or chance. Not only did Berkshire Hathaway deliver a compounded annual return that was double that of the S&P 500, it did so with consistency, outperforming the index in 37 out of 55 years. It is true that the returns have looked a lot more ordinary in the last two decades, and we will come back to examine those years in the next post.

Along the way, Buffett has proved to be an extraordinary spokesperson for value investing, not only by delivering mind-blowing returns, but also because of his capacity to explain value investing in homespun, catchy letters to shareholders each year. In 1978, he was joined by Charlie Munger, whose aphorisms about investing have been just as effective at getting investor attention, and were captured well in this book. There have been others who have worn the value investing mantle successfully, and I don't mean to discount them, but it is difficult to overstate how much of value investing as we know it has been built around Graham and Buffett. The Buffett legend has been burnished not just with flourishes like the 1969 partnership letter but by the stories of the companies that he picked along the way. Even novice value investors will have heard the story of Buffett's investment in American Express in 1963, after its stock price collapsed following a disastrous loan to scandalous salad oil company, and quickly doubled his investment.

The Numbers Strand

If all that value investing had for it were the stories of great value investors and their exploits, it would not have the punch that it does today, without the help of a numbers strand, ironically delivered by the very academics that value investors hold in low esteem. To understand this contribution, we need to go back to the 1960s, when finance as we know it, developed as a discipline, built around strong beliefs that markets are, for the most part, efficient. In fact, the capital asset pricing model, despised by value investors, also was developed in 1964, and for much of the next 15 years, financial researchers worked hard trying to test the model. To their disappointment, the model not only revealed clear weaknesses, but it consistently misestimated returns for classes of stock. In 1981, Rolf Banz published a paper, showing that smaller companies (in terms of market capitalization) delivered much higher returns, after adjusting for risk with the CAPM, than larger companies. Over the rest of the 1980s, researchers continued to find other company characteristics that seemed to be systematically related to "excess" returns, even though theory suggested that they should not. (It is interesting that in the early days, these systematic irregularities were called anomalies and non inefficiencies, suggesting that it was not markets that were mispricing these stocks but researchers who were erroneously measuring risk.)

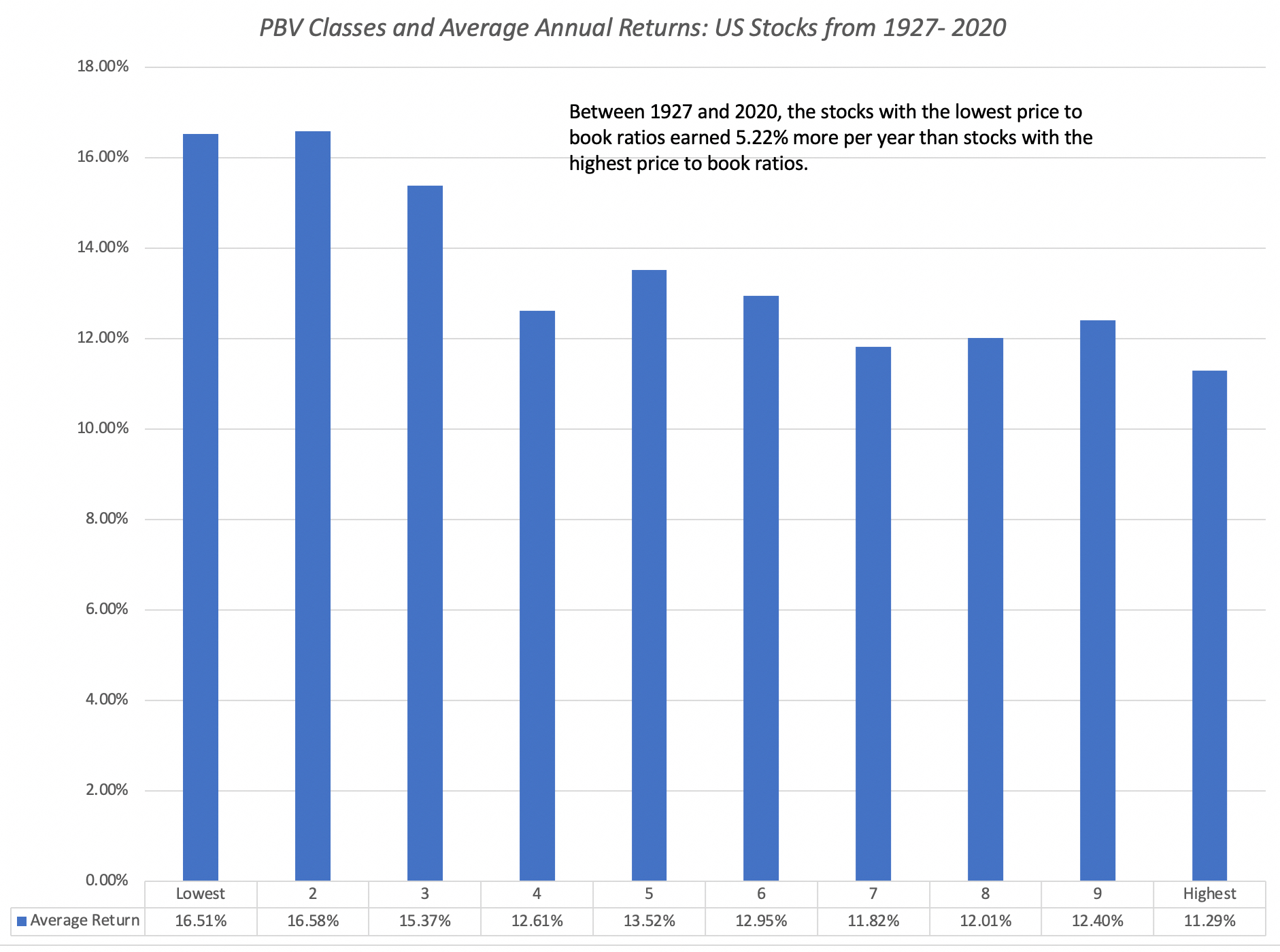

In 1992, Fama and French pulled all of these company characteristics together in a study, where they reversed the research order. Rather than ask whether betas, company size or profitability were affecting returns, they started with the returns on stocks and backed into the characteristics that were strongest in explaining differences across companies. Their conclusion was that two variables, market capitalization (size) and book to market ratios explained the bulk of the variation in stock returns from 1963 to 1990, and that the other variables were either subsumed by these or played only a marginal role in explaining differences. For value investors, long attuned to book value as a key metric, this research was vindication of decades of work. In fact, the relationship between returns over time and price to book ratios still takes pride of place in any sales pitch for value investing, and Ken French has been kind enough to keep updating and making accessible the data on the Fama-French factors, allowing me to provide you with an updated version of the link between returns and price to book ratios:

|

| Source: Ken French |

That study has not only been replicated multiple times with US stocks, and there is evidence that if you back in time, low price to book stocks earn premium returns in much of the rest of the world. Dimson, Marsh and Staunton, in their comprehensive and readable annual update on global market returns, note that the value premium (the premium earned by low price to book stocks, relative to the market) has been positive in 16 of the 24 countries that they have returns for more than a century and amounted to an annual excess return of 1.8%, on a global basis.

While value investors are quick to point to these academic studies as backing for value investing, they are slower to acknowledge the fact that among researchers, there is a clear bifurcation in what they see as the reasons for these value premium:

- It is a proxy for missed risk: In their 1992 paper, Fama and French argued that companies that trade at low price to book ratios are more likely to be distressed and that our risk and return models were not doing an adequate job of capturing that risk. They and others who have advanced the same type of argument would argue that rather than be a stamp of approval for value investing, these studies indicate risks that may not show up in near term returns or in traditional risk and return models, but eventually will manifest themselves and cleanse the excess returns. Put simply, in their world, value investors will look like they are beating the market, until these unseen risks show up and mark down their portfolios.

- It is a sign of market inefficiency: During the 1980s, as behavioral finance became more popular, academics also became more willing to accept and even welcome the notion that markets make systematic mistakes and that investors less susceptible to these behavioral quirks could take advantage of these mistakes. For these researchers, the findings that low price to book stocks were being priced to earn higher returns gave rise to theories of how investor irrationalities could explain these returns.

The End Result

When valuing companies, I talk about how value is a bridge between stories and numbers, and how the very best and most valuable companies represent an uncommon mix of strong stories backed up by strong numbers. In the realm of investment philosophies, value investing has had that unique mix work in its favor, with stories of value investors and their winning stocks backed up by numbers on how well value investing does, relative to other philosophies. It is therefore no surprise that many investors, when asked to describe their investment philosophies, describe themselves as value investors, not just because of its winning track record, but also because of its intellectual and academic backing.

YouTube Videos