Gurus

35 Ideas from 2021 - Vishal

Right before the year ends, I thought I’d share a handful of ideas I’ve read, learned, re-learned, and wrote about in the past twelve months. Here are 35 of them, in no particular order of importance. I hope you find these useful, as much as I did.

1. You or Me are Not the Market

Earning the long-term returns of the market, of the past or the future, is not in our control. Managing our risks and avoiding ruin, mostly is.

“Rationality is avoidance of systemic ruin,” advices Nassim Taleb.

Trying to avoid the ruin the stock market system enforces upon people who disregard its workings is rational. Believing that you can beat the system at it, by playing the game mindlessly, isn’t.

Someone wise once said –

People destroy themselves in unique interesting ways. Systems destroy people in uniform boring ways.

Now the problem with beating the system for some time is that we get a swelled head. We start believing that if the stock we have invested in has earned us magnificent returns over the past 2-3 months or years, it was entirely an element of our skill and no luck. Yes, that’s how the mind behaves and makes us believe.

2. Beware the Swelled Head

In his book Jesse Livermore – Boy Plunger: The Man Who Sold America Short in 1929, the author Tom Rubython says of the period during which Livermore, ranked among the best stock market speculators ever, lost his $100 million fortune: “In truth, it was a period of total inconsistency and illogicality during which, by his own rules, he should have been out of the market sitting on his money. But he wasn’t. Having conquered the world, he wanted to climb the mountain again.”

Livermore went long on the stock market as it slipped to its lows by mid-1932. Then, in 1932, he shorted the market again, and this time the market doubled. The final blows were caused in 1933 when he went long the market just as it fell back near its 1932 lows. Call it extreme bad luck, but Livermore had set himself up in a way for such luck to find him. Of course, you can make out from the readings on his life that he was prone to depression caused by extreme stress of his work i.e., stock trading and speculation.

He once said of his profession –

…a man must give his entire mind to his business if he wishes to succeed in stock speculation.

He probably took his advice too seriously and gave his entire mind to his business. It was seemingly during one of these depressive moments that he took his own life.

There is, however, no doubt that upping the game, and getting rich in the process, had gone to Livermore’s head. As he reflected after his third bankruptcy –

After all those long years of successes, tempered by mistakes that really served to pave the way for greater successes, I was now worse off than when I began in the bucket shops. I had learned a great deal about the game of stock speculation, but I had not learned quite so much about the play of human weaknesses.

There is no mind so machine-like that you can depend upon it to function with equal efficiency at all times. I now learned that I could not trust myself to remain equally unaffected by men and misfortunes at all times.

I sometimes think that no price is too high for a speculator to pay to learn that which will keep him from getting the swelled head. A great many smashes by brilliant men can be traced directly to the swelled head — an expensive disease everywhere to everybody, but particularly in Wall Street to a speculator.”

3. Make-Lose > Lose-Make

Path dependence, in simple terms, explains how history really matters – where we have been in the past determines where we currently are and where we can go in future.

Nassim Taleb writes in Skin in the Game –

Assume that your capital is around one million dollars and you are involved in speculation. Apply path dependence to the reasoning.

Making a million dollars first, then losing it, is markedly different from losing a million dollars first then making it.

The first path (make-lose) leaves you intact; the second (lose) makes you bankrupt, insolvent, maimed, traumatized and more generally unable to stay in the game, thus unable to benefit from the second part of the sequence. There is no ‘make’ after the ‘lose.’

4. A Bored Investor is A Dangerous Thing

Jason Zweig, in an article he wrote in late 2016, mentioned how a bored investor is a dangerous thing (often to himself). He wrote –

A bored investor is probably more likely to succumb to the whims of other bored investors moving in a herd.

All of this is true for professional as well as individual investors. In his classic book Where Are the Customers’ Yachts?, published in 1940, Fred Schwed wrote: “Your average Wall Streeter, faced with nothing profitable to do, does nothing for only a brief time. Then, suddenly and hysterically, he does something which turns out to be extremely unprofitable. He is not a lazy man.”

So, whether you invest for yourself or work with a financial adviser, it’s important to resist the pull of action for action’s sake.

Jason also quoted Charles Ellis, whom he calls Wall Street’s wisest man, as saying…

Investing is a continuous process too. It isn’t supposed to be interesting…If you go to the stock market because you want excitement, then sooner or later you will lose.

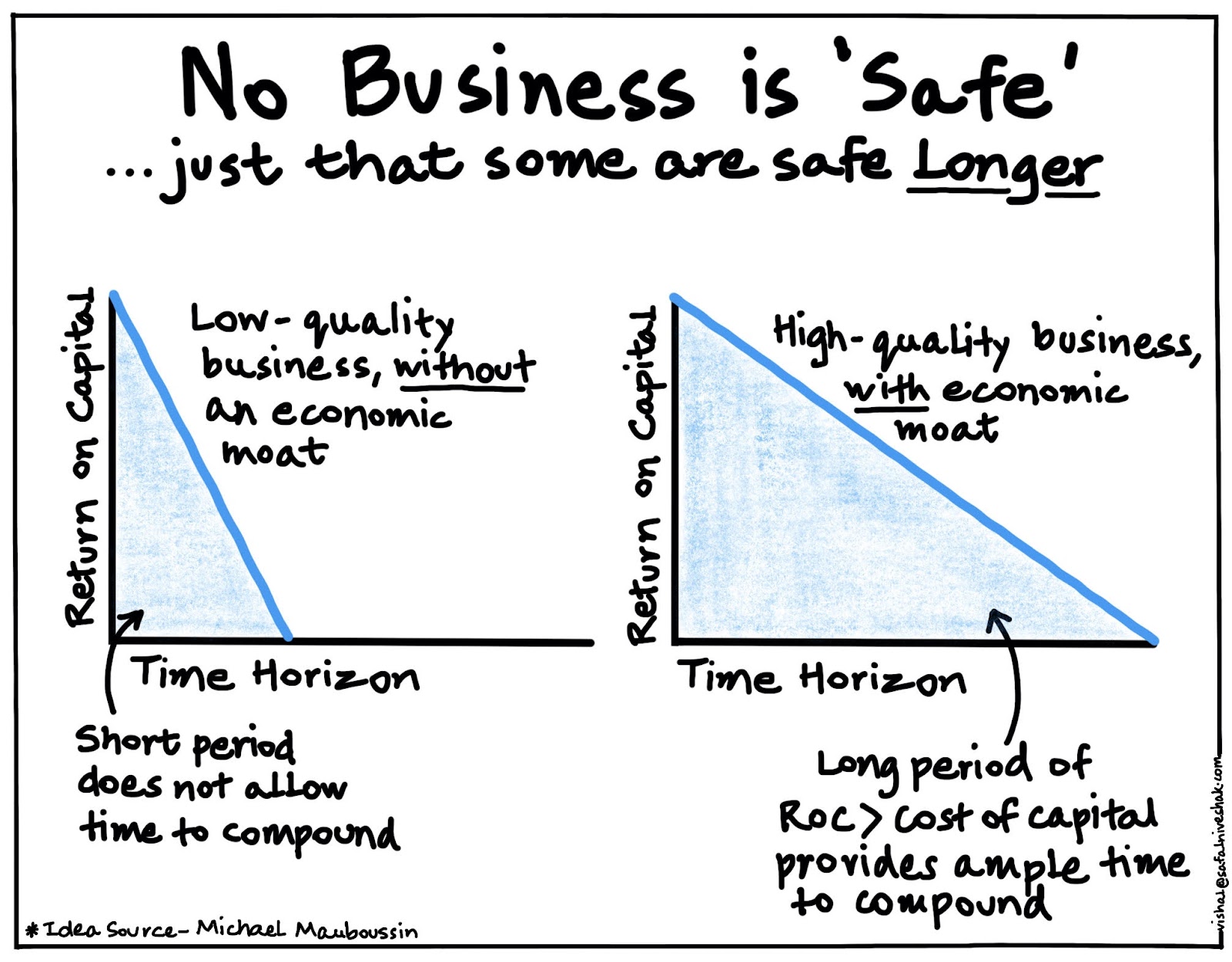

5. No Stock is Safe

The bulls may want you to believe this, but no stock is safe.

There are businesses that may remain good (earning return on capital greater than cost of capital) for some time, maybe a long time, but you must not attach infinite values to them.

This is because high returns attract competition, generally causing return on capital to move towards the cost of capital. While such companies may still earn excess returns, but the return trajectory is down.

Everything in this world, after all, is momentary. So, your best bet is to just stick with quality (even that is momentary, just for longer moments that allows time for compounding to work its magic).

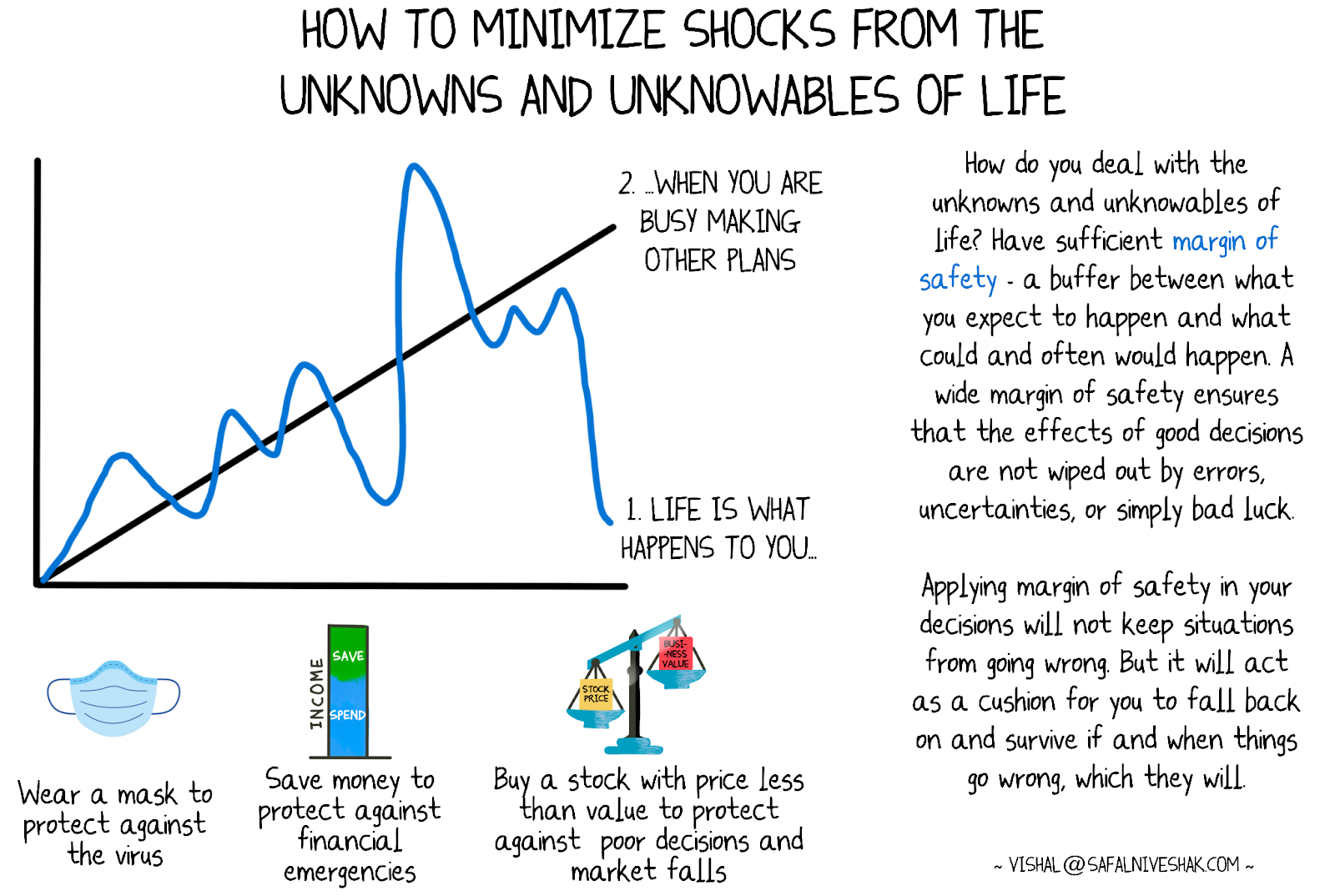

6. Minimize Shocks from the Unknowns and Unknowables of Life

“Life,” John Lennon said, “is what happens to you while you are busy making other plans.” We have seen ample proof of this in the last year.

However, here is a tool, a mental model, a practice that can help us minimize the shocks that the unknowns and unknowables of life render us from time to time.

It is called ‘margin of safety’ – a widely known but rarely applied idea – which is an engineering concept that is used to describe the ability of a system to withstand loads that are greater than expected. In simple words, it is a buffer between what you expect to happen and what could (and often would) happen.

Life may offer you a raw deal, sometimes when you least expect it. A wide margin of safety ensures that the effects of good decisions are not wiped out by errors, uncertainties, or simply bad luck.

7. Hubris = Danger

Nassim Taleb wrote in Fooled by Randomness –

Clearly, the quality of a decision cannot be solely judged based on its outcome, but such a point seems to be voiced only by people who fail (those who succeed attribute their success to the quality of their decision).

In the same way, be very careful when you judge your stock market success by the outcome you achieve, and not by the decision you made.

I am an eternal optimist as far as stock market investing is concerned, but please be very careful of what you are doing with your money and why you are doing it. There are great dangers of hubris while dealing with your money. And the only way you can avoid those dangers is by avoiding hubris.

The legendary investor Seth Klarman said this in an interview with Charlie Rose in 2012 –

You need to balance arrogance and humility…when you buy anything, it’s an arrogant act. You are saying the markets are gyrating and somebody wants to sell this to me and I know more than everybody else so I am going to stand here and buy it. I am going to pay 1/8th more than the next guy wants to pay and buy it. That’s arrogant. And you need the humility to say ‘but I might be wrong.’ And you have to do that on everything.

Staying humble with your analysis and forecasting powers will keep you from risking too much in a view of the future that may well turn out to be wrong.

Don’t be blinded by hubris. A little humility can help you steer clear of disaster, in investing and in life.

8. It’s Luck, Stupid

I remember attending a company’s analyst meet in around 2006. It was held in a three-star hotel in a crowded part of Mumbai. Before the meeting began, the company’s safety officer briefed us about the emergency exits and nearest hospitals.

Now, what were the chances of an emergency happening? Probably miniscule. But the loss, if it happened, would be significant.

That lesson applies to investing too. When you multiply the probability of loss into the magnitude of loss, it becomes meaningful. That is the reason why airlines do a safety demonstration before every flight, and surgeons go through their checklists before every surgery.

As an investor, that should be your standard operating procedure too. You should be mentally ready to see your investments go down by 50% rapidly and be prepared to act rationally when that happens.

Investing is largely a game of luck, and relying on luck tends to make us fragile. So it pays to listen to Nassim Taleb who argues that “it does not matter how frequently something succeeds if failure is too costly to bear.”

That is a wonderful, even if a bitter, lesson to take especially when you are basking in the glory of your short term success in the stock market. But that’s a lesson worth taking.

9. Know the Limits of Numbers in Life and Investing

Being an analyst and investor, I have come to know intuitively that, whether it is about a person’s or a company’s health, quantitative measures or numbers, while critically important, tell us only part of the story.

In business analysis, for example, you can calculate all the ratios you can find from now until the end of the world. But unless you try to find the cause of the numbers you come up with, you are playing a useless game.

Unless you understand the working of the business – the underpinnings, the culture, the management, growth runway, etc. – no amount of financial analysis would help you.

Marshall Jaffe wrote in his post titled The Limits of Data in Finance and Life –

All of our decisions are driven by partial information; we just can’t know everything. As objective as we try to be, relying too heavily on any one tool, however useful, can actually separate us from the very reality we think we’re measuring. The one thing that can offset this potential and keep us firmly in the real world is the inclusion of our imperfect, behaviorally biased, subjective but common sense observations.

Understanding the limits of numbers is useful for analysts and investors. Before getting swept up in running financial screeners, collecting numbers, and building models to predict the future of businesses, it is worth considering why you think numbers would solve your problem.

Of course, knowing and understanding the numbers – the vital stats – whether in health or investing, is important to know a part of where you stand today. But if you just depend on those stats to tell you whether things are all fine or not and where they are likely to head, you are missing out on the real, bigger picture.

10. Limits of Heuristics in Investing

I heard a recent brilliant conversation between Barry Ritholtz and Michael Mauboussin on the subject of thinking about stock selection process. Here’s an excerpt –

RITHOLTZ: So, Howard Marks is fond of discussing second level thinking. And so, what I’m hearing from you is that just looking at earnings or P.E. multiples is first level thinking, and second level thinking is putting this into the broader context of earnings relative to free cash flow, relative to intangibles and growth. Is that like a wild overstatement or …

MAUBOUSSIN: No, not at all. I mean, I think that the answer is — the way I might say this differently is that free cash flow is the ultimate thing that we care about. All the other stuff you just mentioned in terms of earnings and multiples, those are all proxies that try to get to the same thing, so they’re short of shorthand, right?

And, by the way, I mean, you’ve had the great Danny Kahneman with you, right? What’s good about shorthands, what’s good about heuristics is they save you time, right? So that’s why they’re useful, that’s why we use them.

What’s limiting about heuristics or shorthand is they have biases, right? And so, the key is not to never use them, the key is to understand where they lie. And I think that’s where people get a little bit – can be a little bit lazy around the edges and just sort of say like it’s — those things always traded at 20 times this, and so it should be 20 times this. That’s not really — you — you want to go back to the core — the core ideas.

11. Know What You Control

The one year period between Feb. 2015 and Feb. 2016 was a particularly bad one for the markets. The broader markets fell around 20% during this period, and there were multitude of stocks that cracked 30-40%. Howard Marks, the legendary investor and Chairman of Oaktree Capital Management, described the situation in the stock market in his Feb. 2016 memo to clients thus –

My buddy Sandy was an airline pilot. When asked to describe his job, he always answers, “hours of boredom punctuated by moments of terror.” The same can be true for investment managers, for whom the last few weeks have been an example of the latter. We’ve seen bad news and prices cascading downward. Investors who thought stocks were priced right 20% ago and oil $70 ago now wonder if they aren’t risky at their new reduced prices.

In the rest of the memo, he went on to explain why Mr. Market – representative of the stock prices – has nothing valuable to offer to investors through his daily mood swings –

Especially during downdrafts, many investors impute intelligence to the market and look to it to tell them what’s going on and what to do about it. This is one of the biggest mistakes you can make. As Ben Graham pointed out, the day-to-day market isn’t a fundamental analyst; it’s a barometer of investor sentiment. You just can’t take it too seriously. Market participants have limited insight into what’s really happening in terms of fundamentals, and any intelligence that could be behind their buys and sells is obscured by their emotional swings. It would be wrong to interpret the recent worldwide drop as meaning the market “knows” tough times lay ahead.

Predicting the subsequent movement of stock prices, like I have mentioned umpteen times in my posts, or the next mood swing of Mr. Market, whether he will be in the best of his spirits or worst – is a loser’s game.

Focusing on where the earnings and cash flows of the underlying businesses you own, or want to own, are going to go long term is what you must focus on.

Your behaviour and expectations are under your control, and so is the amount of risk you wish to take and the time you have in hand. Stock prices and future returns aren’t under your control and thus you must leave them at what they do best, that is, fluctuate.

“If owning stocks is a long-term project for you,” warns psychologist Daniel Kahneman, “following their changes constantly is a very, very bad idea. It’s the worst possible thing you can do, because people are so sensitive to short-term losses. If you count your money every day, you’ll be miserable.”

12. Reality is More Vicious than Russian Roulette

Nassim Taleb wrote in Fooled by Randomness –

First, reality delivers the fatal bullet rather infrequently, like a revolver that would have hundreds, even thousands of chambers instead of six. After a few dozen tries, one forgets about the existence of a bullet, under a numbing false sense of security.

Second, unlike a well-defined precise game like Russian roulette, where the risks are visible to anyone capable of multiplying and dividing by six, one does not observe the barrel of reality. One is capable of unwittingly playing Russian roulette – and calling it by some alternative “low risk” game.

13. Future Returns Will Be Worse than Past

Anand Sridharan wrote in A Statutory Warning for Investing –

I’m in the 15th year of my gig and we’ve have had a decent run so far. But does that mean we’re good investors? I really don’t know because there has been a massive tailwind to my kind of investing. In sticking to decent businesses and not selling, we have benefited from a sizable valuation re-rating. While not unicorn-crazy, current valuations in my corner of the world are near the upper decile of any historical range. Odds are that valuation will be a headwind over next 15 years. As a corollary, future returns will be worse than past. Only question is by how much.

14. To Be Rich, Don’t Be A Rick

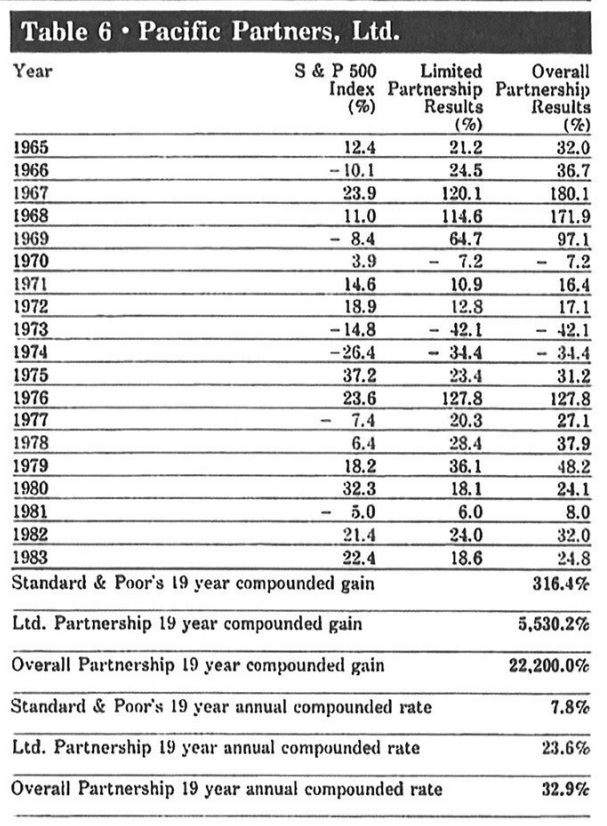

Mohnish Pabrai, the famed investor whom I interviewed in the fourth episode of The One Percent Show, has a lot of lessons to share that he learned from the charity lunch with Warren Buffett he won in 2007. One of the best insights for me, which Warren shared with Mohnish, was about the story of Rick Guerin, who was Warren’s and Charlie Munger’s partner in the 1970s.

Warren had even praised Rick Guerin in his 1984 essay titled “The Superinvestors of Graham-and-Doddsville,” in which he outlined famous value investors and their performances. Warren included in the essay the following table which summarized the performance of Rick’s fund Pacific Partners –

But then, Rick pretty much disappeared off the map, and today not many people know of him as must as they know of Warren and Charlie.

So, when Mohnish asked Warren during the lunch, “Whatever happened to Rick Guerin?” the latter replied something on these lines –

Charlie and I always knew that we would become incredibly wealthy. But we were not in a hurry to get wealthy; we knew it would happen. Rick was just as smart as us, but he was in a hurry. And so actually what happened was that in the 1973-74 downturn, Rick was levered with margin loans. And the stock market went down almost 70% in those two years, and so he got margin calls, and he sold his Berkshire stock to me. I bought Rick’s Berkshire stock at under $40 apiece, and so Rick was forced to sell shares at … $40 apiece because he was levered.

Warren then gave Mohnish this invaluable advice –

If you’re an even slightly above average investor who spend less than they earn, over a life time you cannot help but get rich, if you are patient.

No one else has ever taught about the dangers of leverage and impatience the way Warren taught Mohnish in that one lunch outing.

15. Understand the Pendulum’s Behaviour to Understand the Stock Market

The legendary Howard Marks wrote this to his clients in a memo in July 2004 –

The mood swings of the securities markets resemble the movement of a pendulum. Although the midpoint of its arc best describes the location of the pendulum “on average,” it actually spends very little of its time there. Instead, it is almost always swinging toward or away from the extremes of the arc. In fact, it is the movement toward an extreme itself that supplies the energy for the swing back.

Investment markets follow a pendulum-like swing between euphoria and depression, between celebrating positive developments and obsessing over negatives, and thus between overpriced and underpriced.

There are a few things of which we can be sure, and this is one: Extreme market behavior will reverse. Those who believe the pendulum will move in one direction forever—or reside at an extreme forever—eventually will lose huge sums. Those who understand the pendulum’s behavior can benefit enormously.

16. Wait for the Market to Whisper in Your Ear

One of the key, rarely noticed, skills of the best investors out there is that they often separate their hard work from their action. What this means is that the moment they identify as good business worth investing in may not be the moment they actually buy it. There is sometimes a pause, a wait, a re-reflection, and only then if it is warranted, an action.

This is unlike what we do most of the time, in life and in investing. We do the hard work, and we act on the conclusion. There is rarely a moment of pause and reflection.

I interviewed Vinod Sethi, ex-MD and CIO of Morgan Stanley India, in the

second episode of The One Percent Show. Out of the many insights he shared over our 150 minutes of interaction, here is one that stood out for me that led me to appreciate even more the idea of pausing and waiting for the right time to invest in an idea I have worked upon.

Vinod said –

People have this natural urge that if I have spent 100 hours doing something, then I must act. Whereas my view is that act when prices are going to go up or down, not when you have completed your homework. The market is not waiting for you to complete your homework for the prices to go up or down. I would always urge a lot of my analysts, including myself, to delink analysis from decision-making. Because you have spent a hundred hours on something, you don’t need to act.

The key to being a good money manager is to not act, or not link your hard work to your action. Delink the two. Keep working, because the point of conviction and intuition comes when it comes. But at that time, your homework should be complete. That time you shouldn’t be running around doing homework, because that intuition point will happen when it happens. It is all sitting in your brain. But you act when your intuition wakes up. In a way, the market whispers in your ear.

At the end of the day, I’d say that’s what it is. Because there are 10,000 listed stocks and why would you zone in on something? You need to do a lot of work, but don’t believe or don’t live under the delusion that your work has got you this brilliant idea.

The work has given you the foundation for good seeds to grow. It’s like a garden, which has been well fertilized and watered for some roses to bloom. That’s your research on a daily basis. But the act of the rose coming is when there is a confluence of events, like when a stock is dirt cheap or forgotten or expensive. There’s the real world out there and you’re ready with your homework.

Let’s put it this way. It is like there’s a woolly mammoth coming at you and I give you a gun with a few bullets. There are two ways you can respond. I’ve given you a gun with bullets, so you can start firing. The other way to look at it is to just sit and fire when the woolly mammoth shows up. So, research is like loading the gun, having the bullets. The opportunity is the mammoth showing up. They’re not linked. Having a gun gives you the arrogance that I will fire and can hit the mammoth. That is a classic mistake of most analysts.

This has been one of the most wonderful insights I have received from anyone on The One Percent Show so far.

What Vinod suggested is that you must keep doing your work of identifying good investment opportunities, but if the prices are not right, and there is no margin of safety, don’t act. Least of it, don’t act just because you have done the hard work. Stocks do not bother about your hard work.

But when the time is right – and you are ready with your idea and capital – the market will whisper in your ear.

Wait for that whisper. And only when you hear it, act.

17. A Fool and His Money Are Soon Separated

A reminder from John Kenneth Galbraith who wrote in A Short History of Financial Euphoria –

When will come the next great speculative episode, and in what venue will it recur – real estate, securities markets, art, antique automobiles? To these there are no answers; no one knows, and anyone who presumes to answer does not know he doesn’t know. But one thing is certain: there will be another of these episodes and yet more beyond.

Fools, as it has long been said, are indeed separated, soon or eventually, from their money. So, alas, are those who, responding to a general mood of optimism, are captured by a sense of their own financial acumen. Thus it has been for centuries; thus in the long future it will also be.

18. Escape Your Bubble

Nick Maggiulli wrote in one of the best posts I read this year –

We all live in bubbles. Some of these bubbles are made of money. Some are made of power. Some of pride. Some of hate. Some of lust. Some of loss. The question isn’t whether you are in a bubble, but how often do you get out of it? How often do you escape your bubble to see the world in a different light?

Because failing to escape can lead to a rude awakening. You can chase money or power or beauty or some other idea that eventually leads you astray. You can win that game, but lose yourself in the process. Victorious in battle, but defeated in war. Because there is more to life than what is in your bubble. You just have to escape it once in a while to find out.

19. Never Take a Risk You Do Not Have to Take

The world often looks, and is, like a disorderly place, full of random events. And the irresistible urge to seek patterns can get us into serious trouble when we take this tendency to the field of finance and investing.

As investors, it is important to know that we are dealing with something where randomness and chance can distort the expected outcome in the short term.

Nassim Taleb wrote in Fooled by Randomness –

…risk-conscious hard work and discipline can lead someone to achieve a comfortable life with a very high probability. Beyond that, it is all randomness: either by taking enormous (and unconscious) risks, or by being extraordinarily lucky. Mild success can be explainable by skills and labor. Wild success is attributable to variance.

Time and again it has been proved that majority of stock price changes are nothing more than random jitters in the system for which no explanation is ever required. Yet you can find people obsessing over every movement and explaining it like kids spotting animal shapes in the clouds.

You don’t have to be one of those.

In fact, you just have to do your work, and then let randomness do its own.

Like Taleb advises, risk-conscious hard work and discipline can lead you to achieve a comfortable life with a very high probability.

If you are trying to seek anything else through your investments in the market, you may be playing with fire.

20. Own Good Businesses

Bharat Shah, the legendary Indian investor, wrote this about the importance of owning good businesses, in his book Of Long Term Value & Wealth Creation from Equity Investing –

A good business may face two challenges: It may face a fundamental challenge or adversity in the business at some point in time, or there can be a general challenge when markets are passing through tough times. Both may lead to drop in market value.

More often than not, it is the good businesses which are still in profits when markets are falling, and there is an overbearing temptation to surrender them away when things look bleak, outlook negative and pain-points in the markets appear high (“Plucking the flowers to water the weed”). But it is important not to surrender away good businesses due to the trying times of the market. And even if it faces a fundamental challenge, but a temporary one, then it may be all the more important to embrace the stock than to shun it.

Equally, when the general markets are passing through a tough phase and the sentiments are down, the tendency to give away a good one for a temporary mental satisfaction may prove to be an expensive gambit. It is important not to use a broom to sweep away the good ones while keeping the dirt inside.

Howard Marks wrote this sometime in 1990 –

21. Avoid the Losers. Avoid the Losers

The best foundation for above-average long-term performance is the absence of disasters. There will always be cases and years in which, when all goes right, those who take on more risk will do better than we do. In the long run, however, I feel strongly that seeking relative performance which is just a little bit above average on a consistent basis – with protection against poor absolute results in tough times – will prove more effective than ‘swinging for the fences.

That is the mantra of sensible investing – If I avoid the losers, the winners will take care of themselves.

22. Value Investing = Hard Word

The legendary Seth Klarman wrote this in his must-read book Margin of Safety why value investing requires a great deal of hard work, unusually strict discipline, and a long-term investment horizon. Few are willing and able to devote sufficient time and effort to become value investors, and only a fraction of those have the proper mindset to succeed –

Like most eighth- grade algebra students, some investors memorize a few formulas or rules and superficially appear competent but do not really understand what they are doing. To achieve long-term success over many financial market and economic cycles, observing a few rules is not enough.

Too many things change too quickly in the investment world for that approach to succeed. It is necessary instead to understand the rationale behind the rules in order to appreciate why they work when they do and don’t when they don’t. Value investing is not a concept that can be learned and applied gradually over time. It is either absorbed and adopted at once, or it is never truly learned.

Value investing is simple to understand but difficult to implement. Value investors are not super-sophisticated analytical wizards who create and apply intricate computer models to find attractive opportunities or assess underlying value.

The hard part is discipline, patience, and judgment. Investors need discipline to avoid the many unattractive pitches that are thrown, patience to wait for the right pitch, and judgment to know when it is time to swing.

23. Tomorrow May Not Be Like Yesterday

A recent memo from Howard Marks in 2021 titles The Winds of Change contained this note on the current investment environment and changing nature of business –

Today, unlike in the 1950s and ’60s, everything seems to change every day. It’s particularly hard to think of a company or industry that won’t either be a disrupter or be disrupted (or both) in the years ahead. Anyone who believes all the firms on today’s list of leading growth companies will still be there in five or ten years has a good chance of being proved wrong.

For investors, this means there’s a new world order. Words like “stable,” “defensive” and “moat” will be less relevant in the future. Much of investing will require more technological expertise than it did in the past. And investments made on the assumptions that tomorrow will look like yesterday must be subject to vastly increased scrutiny.

24. Don’t Just Get Sucked In

As a runaway bull market persists, its relentless vacuum cleaner eventually sucks everyone in. Investors who are skeptical about the perceived overvaluation are forced to watch as their career prospects melt down and security prices melt up. New rationalizations, disguised as rationales, enter the higher levels of discourse to justify jumping, or creeping, onto the asset-price train despite disdaining it when it was dozens of percentage points lower. A feeling of fear and acrophobia then becomes replaced by the giddy and disorienting feeling of finally being on track to make money along with the crowd and not feeling isolated in Cranky Valueland.

~ Paul Singer

25. Think About Your Wealth Like Your Children

Your wealth is like your children — the primary link between your present and the future. You should try to think about it in the same way. You want your children to have freedom but you also want them to be good people who can take care of themselves. You don’t want to blow it, because you don’t get a second chance. When you invest, it’s not your wealth today, but it’s your future that you’re really managing.

~ Peter Bernstein

26. No God Wants You to Get Rich

Once a bull market gets under way, and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can’t-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov’s dog, these ‘investors’ learn that when the bell rings – in this case, the one that opens the New York Stock Exchange at 9:30 a.m. – they get fed. Through this daily reinforcement, they become convinced that there is a God and that he wants them to get rich.

~ Warren Buffett

27. Things Don’t Get Better (or Worse) Forever

Very early in my career, a veteran investor told me about the three stages of a bull market. Now I’ll share them with you. The first, when a few forward-looking people begin to believe things will get better. The second, when most investors realize improvement is actually taking place. The third, when everyone concludes things will get better forever. Why would anyone waste time trying for a better description? This one says it all. It’s essential that we grasp its significance.

~ Howard Marks

28. Humility and Investing

Being humble in investing isn’t about being doubtful of yourself, or believing that you are untalented, unintelligent, or unworthy. On the contrary, it is about being humble about our own intellect, to question whether what we know is actually correct and even to adjust our beliefs if we are presented with new information. In other words, it is largely to do with intellectual humility.

As Philip Tetlock wrote in Superforecasting, true humility (in investing) is about recognizing that “…reality is profoundly complex, that seeing things clearly is a constant struggle when it can be done at all, and that human judgment must, therefore, be riddled with mistakes.”

Very few investors have the nerve to say, “I don’t know.” But that’s how you build humility in your investment process. If you start with “I don’t know,” then you are unlikely to act so boldly as to get into trouble.

29. Integrity and Investing

Successful investors focus on their investment process with unwavering steadfastness and honesty, whatever the stock market is doing and however others around them are behaving.

They show how, to be a successful investor, you must have a philosophy and a process that you stick to even when the times get tough. This is very important. If you don’t have the courage of your conviction and patience and toughness, you can’t be an investor because you’ll constantly be driven to fall in line with the consensus by buying at the top and selling at the bottom.

But it’s important to know that no approach will allow you to profit from all kinds of opportunities in all environments. You must be willing not to participate in everything that goes up, and only the things that fit your process and investment approach.

30. Tenacity and Investing

Over the years I have met a multitude of investors who knew about the power of compounding, but very few who truly understood its real power because that shows up not in one, three, or five years…but ten, fifteen and twenty years. And in an age of instant gratification, since not many have the tenacity to hold on to their faith in this power and in high-quality companies to create wealth, not many investors end up successful.

American investor, hedge fund manager, and philanthropist Leon Cooperman is quoted as saying –

It doesn’t matter whether you are a lion or a gazelle; when the sun comes up you’d better be running.

Cooperman is seemingly talking about the importance of hard work here, which is a direct offshoot of tenacity. Sensible investing is hard work.

But then, Jesse Livermore, one of the greatest stock speculators of all times, is supposed to have said –

The main reason why money is lost in stock speculations is not because Wall Street is dishonest, but because so many people persist in thinking that you can make money without working for it and that the stock exchange is the place where this miracle can be performed.

Warren Buffett has said –

I learned at a very early age how important it is to work hard and be honest.

Hard work you put in identifying businesses you want to own, and then the hard work you put in just staying put, doing nothing, is what should help you succeed in your investment endeavors. There are no shortcuts to the top.

31. Self-Awareness and Investing

George Goodman aka Adam Smith wrote in his book The Money Game –

If you don’t know who you are, [stock market] is an expensive place to find out.

Mere gathering of facts and bookish knowledge can only lead us to chaos. That chaos is what causes most people to fail in their investing lives despite all the books they read and courses they attend. While it is obviously necessary to read the wisdom and ideas contained in all those great investment books, they will only help us with the “techniques.”

But without understanding ourselves, those techniques would only lead us to frustration (maybe, an ‘intelligent’ frustration) and ultimately failure.

In studying successful investors over the years, I have come to realize that the right kind of investing education comes with the transformation of ourselves, which entirely depends on our awareness of ourselves – our behaviour, risk-taking capacities, and habits.

When we are aware of ourselves, we are in a better position to behave well. And that can help us save ourselves from self-destruction that most other investors lead them to.

32. Adaptability and Investing

This is the core of Charles Darwin’s theory of evolution –

It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is most adaptable to change.

Adaptability is one of the few skills that are hard to learn but pay off for the rest of your life.

Given the ever-changing world we inhabit, and given that this change is unlikely to ever slow down, what mattered very much yesterday (e.g. skill, knowledge, etc.) might not be worth a dime tomorrow. Change used to be slow and incremental: now it is rapid, radical and unpredictable.

Adaptability enables us to dwell on new circumstances and stay on top of the situation. Of course, this skill is best when combined with insight, giving us fresh perspective before the change itself. Growth depends on how adaptable you are.

Prof. Sanjay Bakshi told me this in an interaction some time back –

If you bought the right type of business, then there is likely to be a tendency for it to deliver better than what you envisaged. If you see that tendency play out after you have invested, don’t ruin it by staying with the original model. Your model has to be adaptive. If the performance is far better (or worse) than you envisaged, you have to change the model unless the improvement (or deterioration is likely to be temporary).

As Keynes used to say, when facts change, I change my mind. You have to have the same mindset when it comes to investing in both directions. That is, if the business is delivering far poorer performance than what you had envisaged earlier, and that performance is likely to continue because the moat is impaired, then your original model needs to be re-worked and it may well turn out to be the case that you should sell the stock. You have to have the ability to be detached from the outcomes, based on dispassionate analysis of real, meaningful data (not noise).

Combine adaptability with agility in these changing times and you have the right ingredients of success as an investor.

33. Building Investing Character Takes Time

The thing about character is that it cannot be strengthened quickly (not the least by reading posts like this one) and in ease and quiet, but only over time and often through the experience of trial and distress during a crisis.

In fact, character often does not come out as a result of crisis, but in a crisis – like during 2000, 2008, and 2020.

Character also comes out during heady times – like during 1999 and 2007, and then now, when your humility, integrity, and tenacity are tested by the overdose of easy and quick money that you and investors around you are making.

Charlie Chaplin said that a man’s true character comes out when he’s drunk. Well, my advice is to learn your lessons from watching others in the stock market who often get drunk on arrogance, fear, greed, and envy. Then, avoid being like them. Over time, you will end up building a strong character.

34. Build A Museum Not A Warehouse of Stocks

I read somewhere that we spend the first half of our lives adding things, and the second half subtracting most of them.

Investing follows life, and this is also what a lot of investors end up doing. They create crowded warehouses of portfolios in the initial years of their investment careers, realize most of their choices were mistakes, and then they start subtracting vigorously.

Lest you lose out on the positive compounding timeframe, you will do yourself a world of good by respecting and practicing this lesson – of saying no to most things, of not adding a lot of unwanted stocks to your portfolios – early.

In other words, be a curator of stocks, not a warehouse manager.

As a starter, use the following checklist to start your stocks’ curation process. Run it on your existing portfolio to test which of your stocks must remain with you and which must be subtracted out.

Bruce Lee got it dead right when he said –

It is not daily increase but daily decrease, hack away the unessential.

This is one of the most critical lessons I have learned and practiced in my life and as an investor. And that has helped me simplify my life considerably and brought me tremendous peace.

35. Shut Up and Wait

The idea of buying and holding high-quality businesses over a long period of time is simple. Everyone knows that, and even those who don’t practice it appreciate that this works with most high-quality businesses as history has proven time and again. But then, it’s important to understand that the action of not doing anything over such a long period of time involves hundreds of decisions over months and years that lead to such inaction.

Like this –

Now, one way is to buy high-quality businesses and forget for 20 years and hope to end up with a fortune. There are quite a few such fairy tales you may have heard of. But the other side of the picture is that countless people have also ended with duds in their portfolios, or vanished companies, when they realized their father or grandfather had bought some stocks and forgot about them for 20 or more years.

So, overall, it’s not easy. And it’s not supposed to be easy.

But if you have done your homework well, and keep your eyes and ears open, ‘shut up and wait’ remains the best bet in your pursuit of wealth creation from stocks.

And like Frank Partnoy wrote this in a brilliant article many years back –

If we are limited to just one word of wisdom about decision-making for children born a hundred years from now, people who will have all our advantages and limitations as human beings but will need to navigate an unimaginably faster-paced world than the one we confront now, there is no doubt what that word should be.

Wait.

Better, shut up and wait.

* * *

I’m so grateful to have you share this journey with me in 2021, and I look forward to continuing our connection in 2022, whatever it may bring.

Stay happy and healthy.

Happy 2022.

With respect,

Vishal

https://www.safalniveshak.com/35-ideas-from-2021/

More articles on Gurus

When Internal Disorder and External Disorder Happen Together - Ray Dalio

Created by Tan KW | Oct 23, 2024

The Split in the Democratic Party: The Lina Khan Litmus Case and The Relevant Principles - Ray Dalio

Created by Tan KW | Oct 17, 2024

Behind the Memo – The Impact of Debt with Howard Marks and Morgan Housel

Created by Tan KW | Aug 27, 2024

Pick A Side And Fight For It, Keep Your Head Down, Or Flee - Ray Dalio

Created by Tan KW | Jun 26, 2024

Warren Buffett presides over the 2024 Berkshire Hathaway annual shareholders meeting — 5/4/24

Created by Tan KW | May 05, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

2

Good Articles to Share

3

4

Koon Yew Yin's Blog

5

BFM Podcast

6

7

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....