Gurus

35 Ideas from 2022 - Vishal

Right before the year ends, I thought I’d share a handful of ideas I’ve read, learned, re-learned, and wrote about in the past twelve months. Here are 35 of them, in no particular order of importance. I hope you find these useful, as much as I did.

1. The Investor’s Manifesto

This is for you. This is from someone like you.

It is an Investor’s Manifesto.

It is something you can reflect back on if you ever felt stuck in your investing life.

If you believe in it, follow it, and stand for it, your investing life will be good.

Click here to download the manifesto.

Read it. Print it. Frame it. Face it. Remember it. Do it.

This is YOUR Manifesto.

And if you find value in it, please share it.

2. Long Term Investing is Hard

The biggest reasons more people do not practice long term investing are that –

- It flies in the face of anything taught in business schools – that is, short termism – where most influencers/experts come from,

- It requires a painful degree of patience because it is only over long periods of time that the market eventually gravitates toward value,

- Life spans of businesses and their competitive advantage periods, on an average, are shortening,

- Our attention spans and holding periods are shrinking, and

- Noise is magnifying.

Given all of this, long term investing has become an increasingly difficult and contrarian endeavour. And so, not many investors have the ability or the wherewithal to practice it.

In fact, most people participating in the stock market don’t even understand what they are doing. This is especially when making money gets quick and easy, and they are doing great at it.

Like Aesop’s wolf in sheep’s clothing, they play a role contrary to their real character, which often leads them to the slaughterhouse.

However, the lack of patience of such people to invest with a long-term horizon creates the opportunity for the few committed to long-term holding periods.

In the battle between impatience and patience, the latter wins.

With over nineteen years of practicing long term investing with sincerity and with decent success (purely based on personal standards of success), and seeing a lot of my fellow investors drop out due to their disbelief in its continuity and now ruing their decisions, I can vouch for this powerful idea.

Long term investing is certainly hard, but if you know how to deal well with its hardness, it’s totally worth it.

3. How to Survive Complexity of Financial Markets

I think the most important qualities that you need to survive the complexity of the financial markets are a combination of –

- Humility, and

- Fine-tuned bullshit detector.

You need humility to prevent yourself from overcomplicating investing more than it needs to be and taking risks greater than you’re able to handle.

And you need a fine-tuned bullshit detector to protect yourself from the swarms of sales pitches and get-rich-quick schemes that plague the industry.

There are other things – a good grasp of basic arithmetic and accounting, delayed gratification, and the ability to live below your means. But those first two are most important.

4. Before You Seek Investment Advice

When someone on TV says (or a journalist writes), “You should do X with your money,” stop and think: How do you know me? How do you know my goals? How do you know my short-term spending needs? How do you know my risk tolerance?

Of course, they don’t. Which means you shouldn’t pay much attention to it. Personal finance is very personal, which means broad, general, advice can be dangerous.

For media, I’m most interested in historical finance, which helps put investing into proper context, and behavioural finance, which lets you frame investing based around your own goals, flaws, and skills. But taking direct advice from someone who has never met you is asking for trouble (this includes me).

5. How to Manage Risk of Randomness in Investing

“All of life is a management of risk, not its elimination,” writes Walter Wriston, former chairman of Citicorp.

Randomness is the fabric that weaves the interaction of everything around us. Since you can’t remove randomness from our affairs, you can’t get rid of the risk also. Peter Bernstein in his book Against the Gods writes –

The essence of risk management lies in maximizing the areas where we have some control over the outcome while minimizing the areas where we have absolutely no control over the outcome and the linkage between effect and cause is hidden from us.

What does that mean to you as an investor? It means you need to avoid the game of regular dice and look for the loaded dice. In other words, you should own those stocks/investments where your knowledge (in-depth research) and expertise make the environment less random.

Once you have taken care of randomness, the second and more important thing to remember is to minimize the impact, should randomness strike. This means building a ‘margin of safety.’ The greater the potential impact, the larger the margin of safety you may need.

Here’s Warren Buffett explaining the idea in very simple words –

If you understood a business perfectly and the future of the business, you would need very little in the way of a margin of safety. So, the more vulnerable the business is, assuming you still want to invest in it, the larger margin of safety you’d need. If you’re driving a truck across a bridge that says it holds 10,000 pounds and you’ve got a 9,800-pound vehicle, if the bridge is 6 inches above the crevice it covers, you may feel okay, but if it’s over the Grand Canyon, you may feel you want a little larger margin of safety.

6. Get the Small Things Right

you must do just a few small things right to create wealth for yourself over the long run. Pat Dorsey, in his wonderful book – The Five Rules for Successful Stock Investing – summarizes these few things into, well, just five rules –

- Do your homework – engage in the fundamental bottom-up analysis that has been the hallmark of most successful investors, but that has been less profitable the last few risk-on-risk-off-years.

- Find economic moats – unravel the sustainable competitive advantages that hinder competitors to catch up and force a reversal to the mean of the wonderful business.

- Have a margin of safety – to have the discipline to only buy the great company if its stock sells for less than its estimated worth.

- Hold for the long haul – minimize trading costs and taxes and instead have the money to compound over time. And yet…

- Know when to sell – if you have made a mistake in the estimation of value (and there is no margin of safety), if fundamentals deteriorate so that value is less than you estimated (no margin of safety), the stock rises above its intrinsic value (no margin of safety) or you have found a stock with a larger margin of safety.

If you can put all your efforts into mastering just these five rules, you don’t need to do anything fancy to get successful in your stock market investing. Of course, even as these rules sound simple, they require tremendous hard work and dedication.

As Warren Buffett says – “Investing is simple but not easy.” And then, as Charlie Munger says, “Take a simple idea but take it seriously.”

You just need a simple idea. You just need to draw a few small circles. And then you put all your focus and energies there. That’s all you need to succeed in your pursuit of becoming a good learner, and a good investor.

I believe that the process of working on the basics (the small circles) of learning or investing over and over again leads to a very clear understanding of them. We eventually integrate the principles into our subconscious mind. And this helps us to draw on them naturally and quickly without conscious thoughts getting in the way. This deeply ingrained knowledge base can serve as a meaningful springboard for more advanced learning and action in these respective fields.

Josh writes in his book –

Depth beats breadth any day of the week, because it opens a channel for the intangible, unconscious, creative components of our hidden potential.

The most sophisticated techniques tend to have their foundation in the simplest of principles, like we saw in cases of reading and investing above. The key is to make smaller circles.

Start with the widest circle, then edit, edit, edit ruthlessly, until you have its essence.

I have seen the benefits of practicing this philosophy in my learning and investing endeavors. I’m sure you will realize the benefits too, only if you try it out.

7. Follow the Owner, Not the Dog

8. Mauboussin on Investing Process

Michael Mauboussin recently reflected on his investing process in an interview with Frederik Gieschen. Here are a few wonderful snippets from the same –

“Great investors do two things that most of us do not. They seek information or views that are different than their own and they update their beliefs when the evidence suggests they should. Neither task is easy.”

On common mistakes among analysts. “There was a letter from Seth Klarman at Baupost to his shareholders. He said, we aspire to the idea that if you lifted the roof off our organization and peered in and saw our investors operating, that they would be doing precisely what you thought they would be doing, given what we’ve said, we’re going to do. It’s this idea of congruence.”

What has he changed his mind on? “When you start to understand the fundamental components of complex adaptive systems, there’s no way to look at the stock market the same way again, personally.”

On being an effective teacher. “To be a great teacher, an effective teacher, it’s about being a great student, be a great learner yourself. And I think that comes through if you’re doing it well.”

Check out the interview here.

9. It’s Never a Market Crash Problem

It’s almost always an –

- I don’t know who I am problem

- I don’t know how much pain I am willing to take problem

- I don’t have the patience to give my stocks time to grow problem

- I bought on the tip of that popular social media influencer and did not do my homework problem

- I did not diversify well problem

- I bought the stock just because it dipped problem

- I cannot resist my friends getting rich problem

- I love to fall in love with my stocks problem

- I cannot differentiate between stock price and intrinsic value problem

- I suffer from a buy at any price problem

- I borrowed to invest problem

- I invested the money I needed soon problem

- I don’t have time on my hands to see through market cycles problem

- I trade too much and too often problem

- I keep watching and worrying about stock prices problem

- I will watch the market and my portfolio again after reading this post problem

And so, I must remind myself this at all times –

A market crash is ‘never’ the problem. ‘I’ am the problem, and I must sort myself out, because that is only what I control. And if I can control the ‘I’ better, a market crash will never be a problem.

10. Watch out for the streak of being right

Howard Marks of Oaktree Capital, wrote this in his seminal book The Most Important Thing –

In bull markets – usually when things have been going well for a while – people tend to say ‘Risk is my friend. The more risk I take, the greater my return will be. I’d like more risk, please.’

The truth is, risk tolerance is antithetical to successful investing. When people aren’t afraid of risk, they’ll accept risk without being compensated for doing so… and risk compensation will disappear. But only when investors are sufficiently risk-averse will markets offer adequate risk premiums. When worry is in short supply, risky borrowers and questionable schemes will have easy access to capital, and the financial system will become precarious. Too much money will chase the risky and the new, driving up asset prices and driving down prospective returns and safety.

Risk, which Marks and Warren Buffett have often defined as losing significant amounts of money and permanently, often moves in the same direction as valuations.

In other words, risk increases/decreases as valuations rise/fall. At the same time, high valuations imply weak prospective returns, while depressed valuations imply strong prospective returns. Consequently, both Marks and Buffett suggest that risk is lowest precisely when prospective returns are the highest, and risk is highest precisely when prospective returns are the lowest.

Economist and investment strategist Peter Bernstein said –

The riskiest moment is when you are right.

In much of life, doing things right over and over again is a sign of skill. Consider chess players or expert musicians. They rarely make a wrong move or hit a wrong note. Also, the skill of one good musician does not cancel out the skill of other musicians, that is, it does not make it harder for others to be equally good. This is not true of financial markets. ‘Skilled’ investors’ actions cancel each other out as they quickly bid up the prices of any bargains, which makes luck the main factor that distinguishes one investor from another.

Skill in investing shines through over the long term, but a streak of being right in the short term can make anyone forget how important luck is in determining the outcome.

Watch out for that streak of being right, dear investor.

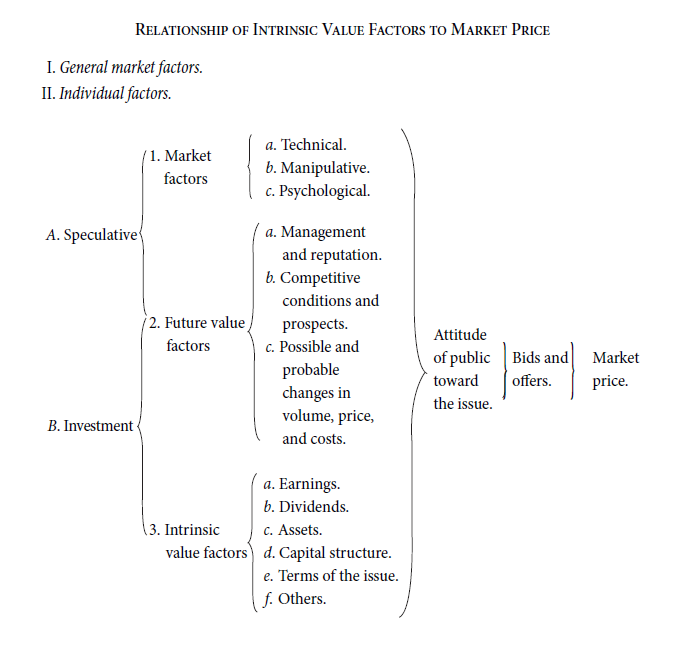

11. What Makes a Market Price

The general question of the relation of intrinsic value to the market quotation may be made clearer by the following chart, which traces the various steps culminating in the market price. It will be evident from the chart that the influence of what we call analytical factors over the market price is both partial and indirect — partial, because it frequently competes with purely speculative factors which influence the price in the opposite direction; and indirect, because it acts through the intermediary of people’s sentiments and decisions. In other words, the market is not a weighing machine, on which the value of each issue is recorded by an exact and impersonal mechanism, in accordance with its specific qualities. Rather should we say that the market is a voting machine, whereon countless individuals register choices which are the product partly of reason and partly of emotion.

Source: Ben Graham and David Dodd, Security Analysis

12. Jack Bogle’s Rules for Investing

Bogle argued for an approach to investing defined by simplicity and common sense. His book The Clash of the Cultures: Investment vs. Speculation has 10 rules laid out in great detail in Chapter 9, and they sum up the Bogle philosophy as:

Investing Versus Speculation

- Remember Reversion to the Mean

- Time Is Your Friend, Impulse Is Your Enemy

- Buy Right and Hold Tight

- Have Realistic Expectations: The Bagel and the Doughnut

- Forget the Needle, Buy the Haystack

- Minimize the Croupier’s Take

- There’s No Escaping Risk

- Beware of Fighting the Last War

- The Hedgehog Bests the Fox

- Stay the Course

13. Focus on the Risks You Take, Not the Returns You Make

In The Psychology of Money, Morgan Housel wrote this on the topic of luck vs risk –

Luck and risk are both the reality that every outcome in life is guided by forces other than individual effort. They are so similar that you can’t believe in one without equally respecting the other. They both happen because the world is too complex to allow 100% of your actions to dictate 100% of your outcomes.

They are driven by the same thing: You are one person in a game with seven billion other people and infinite moving parts. The accidental impact of actions outside of your control can be more consequential than the ones you consciously take.

Apply this to investing and you would realize that when you judge the financial success of others, and even your own, you must not just look at the returns made but also the risks assumed.

Doing well with money is, after all, is less about what you know and more about how you behave. The earlier you understand and appreciate it, the better off your financial return will be over the long run.

But just avoid dying early.

14. Decouple Your Ego from Outcome

There are negative connotations attached to the word ‘loss.’ It’s considered as a synonym to failure. The words loss, wrong, bad, and failure are all regarded as same. So when someone loses money in the stock market, he or she invariably equates it to being wrong. Similarly, when someone makes a profit, it’s assumed that the person was right. But in the stock market, being right and making a profit aren’t necessarily the same thing. And being wrong and incurring a loss aren’t same either.

Jim Paul and Brendan Moynihan wrote in their book What I Learned Losing a Million Dollars –

Success can be built upon repeated failures when the failures aren’t taken personally; likewise, failure can be built upon repeated successes when the successes are taken personally…

Personalizing successes sets people up for disastrous failure. They begin to treat the successes totally as a personal reflection of their abilities rather than the result of capitalizing on a good opportunity, being at the right place at the right time, or even being just plain lucky. They think their mere involvement in an undertaking guarantees success. This phenomenon has been called many things: hubris, overconfidence, arrogance. But the way in which successes become personalized and the processes that precipitate the subsequent failure have never been clearly spelled out.

In other words, successes and failures get personalised when the ego gets involved. And bringing in the ego is the fastest way you can sabotage your investing.

The truth is that investment gains and losses are never a reflection of your intelligence or self-worth. In fact, investing is not about being right or wrong. It is about making decisions, after careful consideration. That is where you sow the seeds of future outcomes, good or bad.

But an outcome is, well, just an outcome, never to be taken personally.

When you decouple your ego from a bad outcome, it creates an opportunity for you to learn from it.

When you decouple your ego from a good outcome, it saves you from future disasters.

15. Investing is a Problem-Solving Exercise

The more I think about investing generally, the more it looks like a massive problem-solving exercise. To succeed at this, you need to manage a series of concepts that may appear to be incompatible. The paradox is that any of these ideas — either side of the argument — may be correct at different times.

The best investors are intellectually flexible but approach their craft as a discipline with a specific process. They understand Probability Theorem but view mistakes as learning opportunities. They use a variety of Mental Models, many of which may occasionally contradict each other or lead to different results. They engage in second-order thinking, use counterfactuals, are aware of information hygiene. They possess a high level of self-awareness regarding their own psychological states.

Source: Investing is a Problem-Solving Exercise by Barry Ritholtz

16. Investing’s Anti-Patterns

In most fields, studying the patterns of success is a standard way to learn. So when people come to financial markets they try the same approach. All new investors get busy investigating how successful investors made their money in the stock market. They want to know the secret behind the winning strategies. But investing is a world of counterintuitive ways.

All successful investors and traders have made their money in widely varying ways and more often than not, their strategies often contradict each other. If one market pro vouches for his or her winning method, another market savant would seem to oppose it ardently.

Jim Paul, in his book What I Learned Losing A Million Dollars, wrote —

Why was I trying to learn the secret to making money when it could be done in so many different ways? I knew something about how to make money; I had made a million dollars in the market. But I didn’t know anything about how not to lose. The pros could all make money in contradictory ways because they all knew how to control their losses. While one person’s method was making money, another person with an opposite approach would be losing — if the second person was in the market. And that’s just it; the second person wouldn’t be in the market. He’d be on the sidelines with a nominal loss. The pros consider it their primary responsibility not to lose money.

The truth is that like there is more than one way to skin a cat, there is more than one way to make money in the markets.

Obviously, there is no ‘one’ secret way to make money because the people who have achieved success in this game over the long run have done it using very different, and often contradictory, approaches. But one big lesson that almost all these people have agreed to settle for is this – Learning how not to lose money is more important than learning how to make money.

Which means if you are looking for success in investing, your chances are better if you take the indirect approach, i.e., finding the ‘anti-patterns.’ In other words, finding ways which most often lead to losses and then actively try to avoid those patterns.

Some such anti-patterns include –

- Chasing performance

- Looking to get rich quick

- Ignoring market cycles

- Letting emotions guide decisions

- Failure to accept mistakes and cut losses

- Venturing beyond circle of competence

- Ignoring margin of safety

- Driven by FOMO – fear of missing out

The list is long, but the idea is simple. To win in investing, find the anti-patterns, and then try to avoid them.

17. When Stock Prices Fall, Are You Happy or Sad?

If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices?

These questions, of course, answer themselves.

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period?

Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall.

In effect, they rejoice because prices have risen for the ‘hamburgers’ they will soon be buying! This reaction makes no sense.

Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.

Source: Warren Buffett, 1997 letter to shareholders

18. The Secret of Investing

If you haven’t figured out your temperament, the stock market is a very expensive place to find out. A long term view requires an ability to stomach extreme short term market volatility. If you can’t do that, you may want to move your money to other instruments like bank fixed deposits and liquid/debt funds.

Jason Zweig wrote in a post on The Wall Street Journal –

In order to capture the potentially higher returns that stocks can offer, you have to reconcile yourself to the certainty of horrifying short-term losses. If you can’t do that, you shouldn’t be in stocks — and shouldn’t feel any shame about it, either.

That’s the point. If your inner voice tells you that you are not wired to do well in stocks because, may be, you are not adept at business analysis or you are too emotional with stock prices or you just do not have the time, you must stay away from direct stock picking, and not feel any shame about that.

But if you are in the arena, it’s better to prepare for problems, expect that your portfolio will occasionally be ‘stormed,’ and get used to such storms. Any market crash won’t feel scary then, just because you would start accepting that as an integral part of your journey of wealth creation.

The secret of investing is that there is no secret. It’s staying the course.

The moment you get it, you become what Ben Graham would call an ‘intelligent investor’ who is destined to do well over the long run.

19. Investing in Uncertain Times

…is almost always more profitable than investing when everything seems certain.

Investors, like most people going about their daily lives, don’t like doubts and uncertainties – like the Covid-19 pandemic, or the Russia-Ukraine crisis. So, we would anything we can to avoid it.

Of course, it’s a good idea to avoid entirely what you can’t totally get your mind around, successful investing is largely about dealing well with uncertainties.

In fact, uncertainties are the most fundamental condition of the investing world.

Seth Klarman wrote in Margin of Safety –

Most investors strive fruitlessly for certainty and precision, avoiding situations in which information is difficult to obtain. Yet high uncertainty is frequently accompanied by low prices. By the time the uncertainty is resolved, prices are likely to have risen.

Investors frequently benefit from making investment decisions with less than perfect knowledge and are well rewarded for bearing the risk of uncertainty. The time other investors spend delving into the last unanswered detail may cost them the chance to buy in at prices so low that they offer a margin of safety despite the incomplete information.

What Klarman suggests is that if you need reassurance and certainty, you’re giving up quite a bit to get it. Like high fees to experts who would predict the future (which you falsely believe as certainty, which it isn’t), or expensive prices for stocks (because everyone knows their future is clear, which often isn’t).

On the other hand, if you can get in the habit of seeking out uncertainty, you’ll have developed a great instinct. Plus, in the long term, it’s highly profitable.

20. Need for an Investment Premise

When you buy a stock, or any investment, you must have a premise – the foundational reason(s), the ‘why?’ for its place in your portfolio – not a narrative that you try to forcefully fit in to what’s hot and in the limelight.

A premise is a reason why a stock will go up over the long run, because the underlying business will grow profitably because the management will allocate capital efficiently, and the market will value that business at current or higher multiples. A narrative, on the other hand, is usually a story you try to fit in to justify why a stock will go up, which is largely because it has gone up in the recent past, and you probably have already made up your mind to own it, and now you cannot go back because you have already committed to the idea in your mind.

Like a storytelling premise, an investment premise also has three elements – the protagonist (you), your goal (wealth creation, or financial freedom) and the obstacles you may face (your emotions of greed, fear, and envy, or the investment going bad).

Without a sound premise, the protagonist of a story may end up with wrong goals and wrong solutions. It will be a flop. In the same with, without a sound investment premise, you may end up owing just a ‘stock’ that you would flip in the next few minutes or days, not an ‘investment’ that you would be willing to own for a few years so that it contributes to your journey of wealth creation and financial freedom.

21. The Five Most Irrelevant Facts of Stock Investing

Look at the following chart. This is a stock’s price plus four other “irrelevant” facts that drain most investors when they consider their investments.

These four irrelevant facts are –

- Price the stock sold at its all-time high,

- Price you paid for the stock,

- Price the stock quoted at its highest since your purchase, and

- Price as on today

None of these matters when you are deciding what to do with your stock investment today. The only thing that matters is where the underlying business stands today and where its earnings and cash flows may reach 5-10 years down the line.

Of course, in the long run, stock prices are representative of the value created by businesses. But they are just that, representatives.

Actual value does not gets created in the world of stock market, but in the world of business.

In fact, like Mr. Bogle said, “the stock market subtracts value, due to all the costs we pay to play the game.”

One of those costs include the stress you take looking at your stock prices, which are plain irrelevant.

So, in short, avoid looking there. Look instead at the businesses you own, the managements that run them, and the value they may create over time.

22. Why Envy is a Really Stupid Emotion

Comparing yourself to others is a perfectly normal human instinct. It’s like comparing notes in a book club – you want to know what everyone else is talking about and how they’re feeling, so you can join them in the conversation. But this comparison isn’t always positive. Some people are more successful than others, some have more money than others, some look better than others – and it’s easy for these differences to lead us into envious rages when other people seem to be doing better than us at something we care about (like making money or looking good).

Charlie Munger calls, envy as a “really stupid sin because it’s the only one you could never possibly have any fun at. There’s a lot of pain and no fun.”

I believe it’s stupid to be envious because of two more reasons. One, envy leads us to want things (or people) for the wrong reasons. We want it because someone else has it, not because we need it.

Two, when we are envious of others, we want just those parts of their lives that look good – high net worth, big house, popularity etc., while not also wanting their hard work, sleepless nights, insecurities, mistakes, tragedies, sorrows, loneliness, injuries, etc.

By separating desire from demand, we can detach from our envy and instead be grateful for what we already have.

The next time you feel envious, remember that the root of this emotion is feeling like you don’t measure up to someone else. This is a natural part of life, but it’s not healthy or productive. Especially when you are an investor.

23. Focus on What’s More Important

Some equations of life I try to live by and that have helped me through my struggles, internal and external –

- Observing > Seeing

- Listening > Hearing

- Health > Wealth

- Compassion > Anger

- Kindness > Wisdom

- Love > Hate

- Forgiveness > Vengeance

- Truth > Facts

- Empathy > Judgement

- Giving > Receiving

- Courage > Intelligence

24. Learn to Listen to Your Inner Voice

Vinod Sethi said this in the second episode of The One Percent Show as one of the lessons he learned early in life –

When people ask me what books I read, or books I recommend reading, I ask them to spend some time listening to their inner voice, their inner guide, their inner compass. It is out there alive and kicking and people should try to listen to it as much as they would like to read other things.

I am not discouraging people from reading other things. I am not saying that, but you need to combine that with what works for you.

25. Learn to Get Along with People You Disagree With

Morgan Housel said this in the fifth episode of The One Percent Show as one of his advices to youngsters on the skills they need to hone to do well in the coming decades –

I think the most undervalued skill is learning how to get along with people that you disagree with. And this is getting more important with technology because it used to be, not even that long ago, 10-20 years ago, that most people lived inside their own bubbles – their own political bubbles, their own religious bubbles. They just interacted with people who were like them, in their home, in their work, their friends.

Your sphere of influence in your social group was really tight in your local community. And now because of social media, your social group might be all over the world. You and I are talking in different continents right now. Like the kind of things that didn’t happen 10 or 20 years ago, but now we do it all the time. And because of that, you’re much more exposed to the views of people you disagree with.

The difference of views has always existed. We’re just aware of them now because of technology. And in that world, there’re basically two options. One, you can get increasingly angrier that other people think differently than you, and you have no ability to change their views. And that makes you angry and cynical. Or two, you can learn how to get along with people who disagree with you. Now, there’s always going to be situations where people you disagree with so fundamentally that it’s just not going to work.

26. Re-Reading Good Books is a Great Idea

The books we read are important because they become part of who we are. They give us ideas and inspiration, help us understand the world around us, and help make sense of our own lives. Books can be so much more than just entertainment or escapism — they can be an invaluable tool for growth and learning.

It’s rare these days to have time to really think deeply about books and ideas. We are bombarded with information, busy with work and family, social media and technology — and even when we’re not doing anything else at all. So it’s important that you re-read good books from time to time if only so that you can remember what they taught you in the first place.

Re-reading is an exercise in deepening your understanding of yourself and the world around you. When we re-read something, we see it from a different perspective, and that can help us see things we might have missed the first time around.

Re-reading books is great for multiple reasons –

- You re-learn ideas that you learned the last time you read the book

- You learn new ideas you missed the last time

- You get a chance to re-look at how you processed a given idea in the past compared to now

Someone asked on this tweet about the book I have re-read the most. It is How to Stop Worrying and Start Living, closely followed by Poor Charlie’s Almanack.

27. Stock Market is a Distraction to Investing

28. Know What You Don’t Know

29. Principles of Intelligent Investing

30. Optimise for Happiness, Not for Returns

31. Market Hits You Where it Hurts the Most

32. Iron Rules of Life and Investing

33. An Investor’s Moats

34: Advice to a Young Investor

Read – Part 1, Part 2, Part 3.

35: Remember the Sturgeon’s Law

May also apply to this post.

* * *

I’m so grateful to have you share this journey with me in 2022, and look forward to continuing our connection in 2023, whatever it may bring.

Stay happy and healthy.

Happy 2023.

With respect,

Vishal

https://www.safalniveshak.com/35-ideas-from-2022/

More articles on Gurus

When Internal Disorder and External Disorder Happen Together - Ray Dalio

Created by Tan KW | Oct 23, 2024

The Split in the Democratic Party: The Lina Khan Litmus Case and The Relevant Principles - Ray Dalio

Created by Tan KW | Oct 17, 2024

Behind the Memo – The Impact of Debt with Howard Marks and Morgan Housel

Created by Tan KW | Aug 27, 2024

Pick A Side And Fight For It, Keep Your Head Down, Or Flee - Ray Dalio

Created by Tan KW | Jun 26, 2024

Warren Buffett presides over the 2024 Berkshire Hathaway annual shareholders meeting — 5/4/24

Created by Tan KW | May 05, 2024

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

Good Articles to Share

New Orleans, Tesla truck explosion, Gazprom and the debt ceiling

4

Good Articles to Share

Apple offers iPhone discounts in China as competition intensifies | REUTERS

5

Good Articles to Share

US Army veteran plows truck into New Orleans crowd - Five stories you need to know | Reuters

6

Good Articles to Share

New Orleans Attack, Tesla Cybertruck Explosion Outside Trump Las Vegas Hotel

7

Good Articles to Share

US Probes New Orleans, Everything Wall Street Expects in 2025 |The Opening Trade: 01/02/2025

8

Good Articles to Share

‘THINGS ARE GETTING WORSE’: Credit card debt skyrocketing to concerning levels #shorts

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....