HLBank Research Highlights

Trading idea: SUNWAY: Values resurface after recent pullback; Grossly oversold

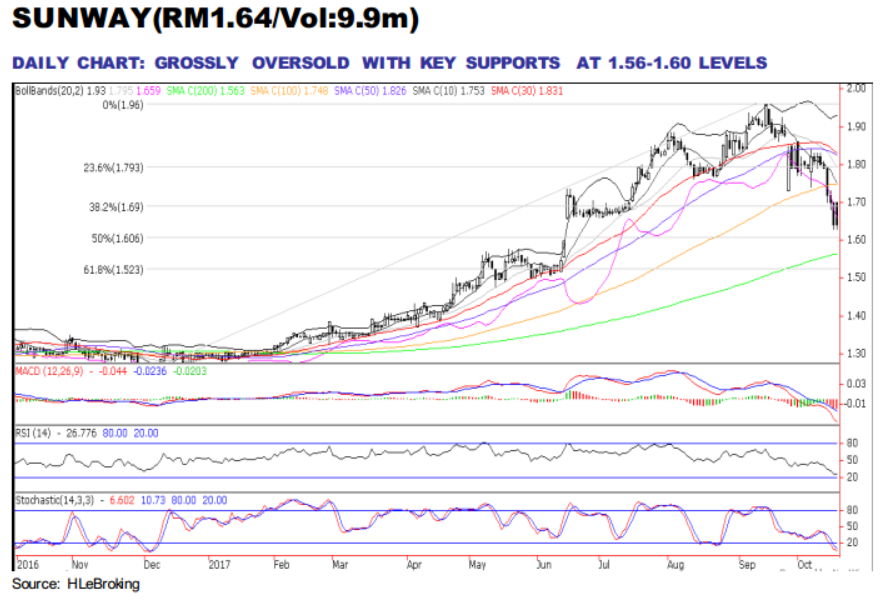

- Values resurface after recent pullback. Sunway’s share prices tumbled 16.3% from all time high of RM1.96 (15 Sep) to end at RM1.64 on 17 Oct as investors took profit following the ex-date of bonus shares and warrants (27 Sep) as well as the 3 sen dividend (13 Oct).

- Our institutional research maintains a BUY rating on Sunway with a SOP TP of RM2.25 as we believe the stock should be rerated and trade closer to its peers such as IJM (18.5x FY18 P/E) and Gamuda (15.6x FY18 P/E) given its diversified income stream and declassification from property sector (now Trading and services).

- At a FY18 P/E of 12.8x (24% lower than its peers 17x), we opine that Sunway is a deep value stock with mature investment properties and the underappreciated trading and healthcare segments, and supported by attractive DY18 of 4% (vs 2.2% for IJM and Gamuda).

- Grossly oversold with key supports at RM1.56-1.60. We believe Sunway’s undemanding valuation and attractive DY have provided a sufficient margin of safety and cushion further sharp share price decline, supported by steeply grossly oversold indicators. We expect the stock to find a floor near RM1.60 (50% FR) and RM1.56 (200-d SMA) territory and trending sideways briefly before staging a technical rebound.

- A decisive close above immediate resistance at RM1.69 (38.2% FR) will spur prices higher to RM1.79 (23.6%) before reaching to our LT objective at RM1.87 (the RM1.89-1.73 gap down on 27 Sep). Cut loss at RM1.54.

Source: Hong Leong Investment Bank Research - 19 Oct 2017

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-07-30

SUNWAY2024-07-30

SUNWAY2024-07-30

SUNWAY2024-07-29

SUNWAY2024-07-29

SUNWAY2024-07-26

SUNWAY2024-07-26

SUNWAY2024-07-26

SUNWAY2024-07-26

SUNWAY2024-07-25

SUNWAY2024-07-25

SUNWAY2024-07-25

SUNWAY2024-07-25

SUNWAY2024-07-24

SUNWAY2024-07-24

SUNWAY2024-07-22

SUNWAY2024-07-22

SUNWAY2024-07-22

SUNWAYMore articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-30 16:35:00

ADX

5 Mins

SELL

2024-07-30 16:30:00

EMA 5

30 Mins

SELL

2024-07-30 15:20:00

EMA 5

10 Mins

SELL

2024-07-30 15:10:00

EMA 5

5 Mins

SELL

2024-07-30 14:40:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

Good Articles to Share

3

4

Good Articles to Share

5

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....