HLBank Research Highlights

Media Prima - A good turnaround and ESG investing proxy, with solid NCPS of 13.5sen

Despite a challenging outlook in the media industry, we are encouraged by the group’s initiative in streamlining its operations and at the same time proactively improving their integrated advertising solutions. MEDIA’s risk-reward profile is attractive after sliding 46% from a 52-week high of RM0.385 to RM0.205. Valuation is undemanding at 41% discount to BVPS of RM0.50 (also 41% below its 5Y mean), supported by 13.5sen NCPS (or 66% to share price). Moreover, current share price is considerably lower against major shareholders’ entry costs i.e. Syed Mokhtar (bought 31.9% stake back in Oct 2019) and Morgan Stanley (12.8% stake accumulated in Apr 2017).

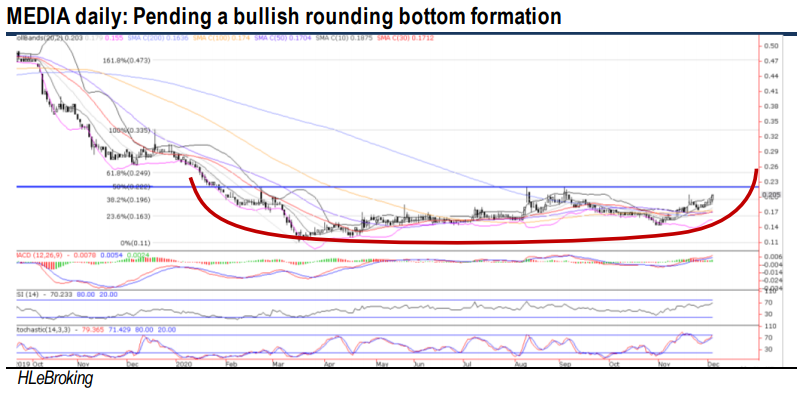

Pending a bullish rounding bottom formation. The rounding bottom or a saucer bottom is a long-term reversal pattern, representing a long consolidation period that turns from a bearish bias to a bullish bias. Following the 1st and 2nd bottoms on 11 March (RM0.11) and 2 Nov (RM0.145), MEDIA’s share price has rebounded above all key SMAs. Given the bullish technicals and a huge 26.3m shares done yesterday (vs 90D average of 4.9m shares), the stock is expected to break the long-awaited neckline resistance of RM0.22 soon. Clearing this hurdle will lift prices higher towards RM0.25 (61.8% FR) before reaching our LT objective at RM0.28 (76.4% FR). Supports are pegged at RM0.195 (38.2% FR) and RM0.18 (20D SMA). Cut loss at RM0.17.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

2

save malaysia!

3

4

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

5

Good Articles to Share

6

Good Articles to Share

7

Good Articles to Share

North Korea vows 'total destruction' of enemy on Korean War anniversary

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....