HLBank Research Highlights

MTAG Group - A Laggard Against Its EMS Customers

MTAG’s future outlook remains promising, given its impeccable track record with reputable “Customer D” suppliers (i.e. ATA IMS, SKP Resources and VS Industry) as well as the multi-year secular uptrend from the ongoing supply chain rerouting out of China. The stock is trading at an appealing FY21 P/E of 12.5x (37% below EMS peers), underpinned by a strong EPS CAGR of 21% from FY20-22 on robust orders from EMS customers and expansion plans underway, attractive FY21-22 DY of 4.9- 5.6%, solid NCPS of RM93m or 13.9sen (after netting ~RM15m for capex in the next 24 months) and potential re-rating catalyst from the transfer of listing status to Main Market from ACE.

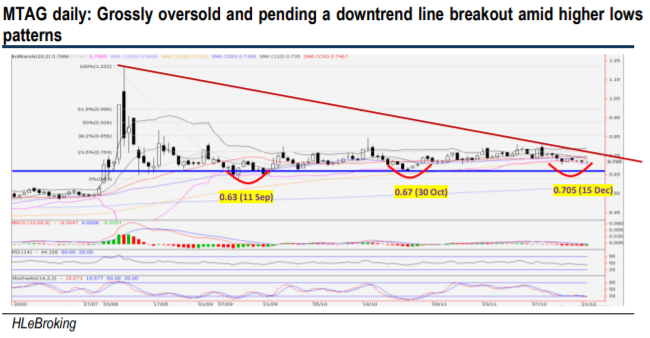

Pending a downtrend line breakout. After hitting all-time high at RM1.22 (7 Aug), MTAG price slid 48% to a low of RM0.63 (11 Sep) before consolidating higher to close at RM0.715 yesterday. Following the formation of higher lows pattern and grossly oversold technical readings, the stock is ripe for a technical rebound in the short term. A decisive breakout above RM0.75 (downtrend line) will spur prices higher to rechallenge RM0.80 levels before heading towards our LT objective at RM0.855 (38.2% FR). Supports are situated at RM0.70 and RM0.67. Cut loss at RM0.66.

Source: Hong Leong Investment Bank Research - 29 Dec 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

save malaysia!

3

4

Good Articles to Share

5

Good Articles to Share

North Korea vows 'total destruction' of enemy on Korean War anniversary

6

Good Articles to Share

7

Good Articles to Share

Yellen says US$3 tril needed annually for climate financing, far more than current level

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....