HLBank Research Highlights

Traders Brief - Glove Stocks to Stay in the Limelight Amid the Resurgence of Covid-19 Cases

MARKET REVIEW

Global. Asian markets ended mildly higher last Friday as strong US and China economic data bolstered expectations of a solid global recovery, overshadowed worries of renewed spike in Covid-19 infections worldwide, which may force more rolling lockdowns in global hotspots. Wall St ended in buoyant mode as the Dow (+164 pts to 34200) and S&P 500 (+15 pts to 4185) closed at record highs whilst the Nasdaq climbed 15 pts to 14052, following better-than-expected earnings from banks, retreating US10Y Treasury yield, and a strong April preliminary consumer sentiment index.

Malaysia. KLCI slipped as much as 8 pts to 1600.3 but recouped the losses to end 0.1 -pt higher at 1608.4, thanks to the bargain hunting interests on index-linked glove makers sparked by fears of another aggressive wave of Covid-19 infections worldwide. Market breadth turned positive as the G/L ratio (516/501) regained above 1 after falling below 1 in the last five consecutive sessions.

Local institutions were net buyers last Friday (RM68m; 46.6% of trading value) compared with net selling by retailers (-RM17m; 38.2% of trading value) and foreigners (-RM51m; 15.2% of trading value). In the week ending 16 April, foreigners were net sellers with net weekly outflows of RM235m (-RM78m previously) whilst local institutions (+RM137m vs - RM11m previously) and retailers (+RM98m vs +RM89m previously) were the net buyers during the week.

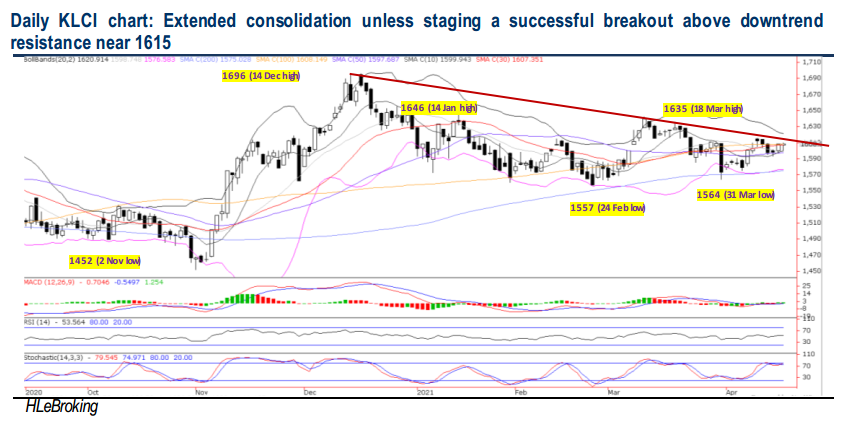

TECHNICAL OUTLOOK: KLCI

WoW, KLCI eased 4 pts at 1608 last Friday on mild profit taking after registering a 27-pt rebound in the week previously. We expect KLCI to extend its sideways consolidation but with an upside bias amid the formation of a small hammer candlestick last Friday. A successful downtrend resistance breakout above 1615 will spur the benchmark higher towards 1635-1646-1656 zones. On the flip side, a sharp fall below 1597 (50D SMA) will trigger downward pressures at 1585-1575 levels.

MARKET OUTLOOK

On the back of the renewed buying appetite on index-linked glove stocks (amid fears of another global Covid-19 wave) coupled with the buoyant Wall St performance, KLCI may attempt to break above the immediate downtrend line resistance near 1615 this week. However, we see stiffer hurdles situated at 1635-1646 levels due to the lack of domestic fresh catalysts and concerns of elevated local Covid-19 cases amid rising R-naught will derail a smoother domestic economic recovery. Meanwhile, weekly supports are pegged at 1597-1585-1574 zones.

On stock selection, we expect a slow and steady recovery for M-REITs, underpinned by a gradual domestic economic revival, the vaccine rollout plan, and the current low interest rates environment (bodes well for future acquisitions). Our top pick is AXREIT (TP: RM2.48; FY21E DY: 4.8%) with strong resiliency throughout the pandemic driven by increased demand in industrial properties, high occupant tenancy in its diversified portfolio and one of the few Shariah-compliant REITs. Other BUY ratings are IGB REIT (TP: RM1.91; FY21E DY: 4.9%), KLCC (TP: RM7.82; FY21E DY: 4.9%) and SENTRAL (TP: RM0.94; FY21E DY: 8%).

Source: Hong Leong Investment Bank Research - 19 Apr 2021

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

BFM Podcast

4

BFM Podcast

5

save malaysia!

6

BFM Podcast

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....