HLBank Research Highlights

Inari Amertron - Rosy Growth Prospects Overshadow Proposed Private Placement and FMCO Concerns

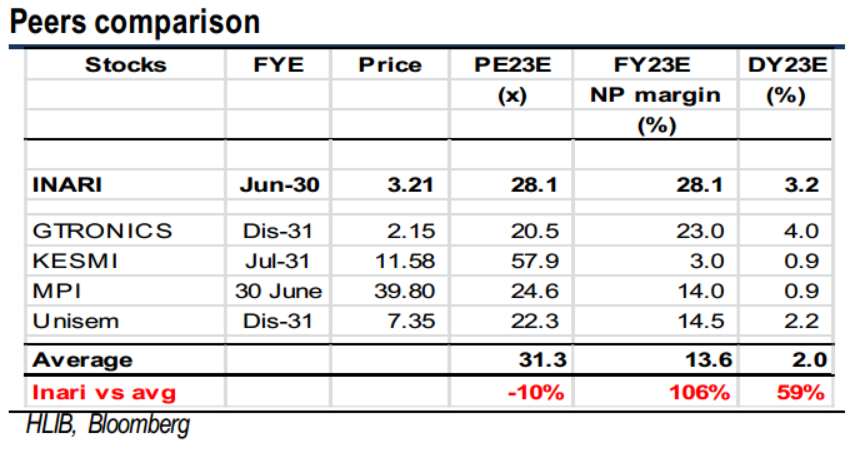

After a 14% correction from its all-time high of RM3.75 to RM3.21, we believe INARI’s (HLIB Research – BUY – TP RM3.81) risk-reward profile is attractive, underpinned by 28.1x FY22 PE (10% lower than peers), supported by a promising FY20-23E EPS CAGR of 39%, superior net profit margin and decent FY21-23 dividend yields (2.6- 3.2%). Besides, the recovery in global growth, sustained strong global semiconductor demand coupled with 5G adoption, above industry average margins, expanded capacity and robust balance sheet (net cash/share of RM0.23) are all positive catalysts for Inari. On the other hand, new earnings-accretive acquisitions, stronger USD, and new customer wins are potential re-rating catalysts for the stock.

Potential downtrend reversal following the double bottom patterns. After plunging 22% from its all-time high of RM3.75 to a low of RM2.92, INARI has staged a mild rebound to end at RM3.21 yesterday. The double bottoms and upticks in technical indicators could signal more upside towards critical neckline resistance at RM3.35. A successful breakout above this hurdle would spur greater upward momentum to retest RM3.62-3.75 zones. Supports are pegged at RM2.92-3.02. Cut loss at RM2.90.

Source: Hong Leong Investment Bank Research - 2 Jun 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-22 16:35:00

EMA 5

5 Mins

SELL

2024-11-22 16:35:00

MACD/RSI

5 Mins

SELL

2024-11-22 16:30:00

EMA 5

5 Mins

BUY

2024-11-22 16:25:00

EMA 5

5 Mins

SELL

2024-11-22 16:20:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

2

3

BFM Podcast

4

5

BFM Podcast

6

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

7

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

8

Mercury Securities Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....