HLBank Research Highlights

Traders Brief - More Downside Toward 1,400-1,410 Before Staging a Technical Rebound on 3Q22 Window Dressing

MARKET REVIEW

Asia/US. MSCI All Countries Asia Pacific index tumbled 1.5% to 145.1 (-3.46% WoW), spooked by relentless selloff from Wall St and surging Treasury yields coupled with sliding emerging market currencies (vs USD) that underscored expectations for tighter monetary policy and a slowing global economy. Dow plunged 486 pts to 29,590 (-4% or 1232 pts WoW; -20% from all-time high 36,952), rattled by unambiguously hawkish Fed that is willing to tolerate a recession as the necessary trade-off for regaining control of inflation.

Malaysia. Follow-through selling spree from Wall St and regional markets coupled with persistent net selling by foreigners (-RM802m for 8th straight session) dragged KLCI to record its 3rd consecutive loss (-14.2 pts to 1,425), resulting a weekly loss of 42.3 pts or 2.9%. In terms of fund flow movements, the week saw both local institutions and retailers registering net weekly inflows amounting to RM353m and RM213m, respectively whilst foreigners emerged as net sellers totalling RM566m.

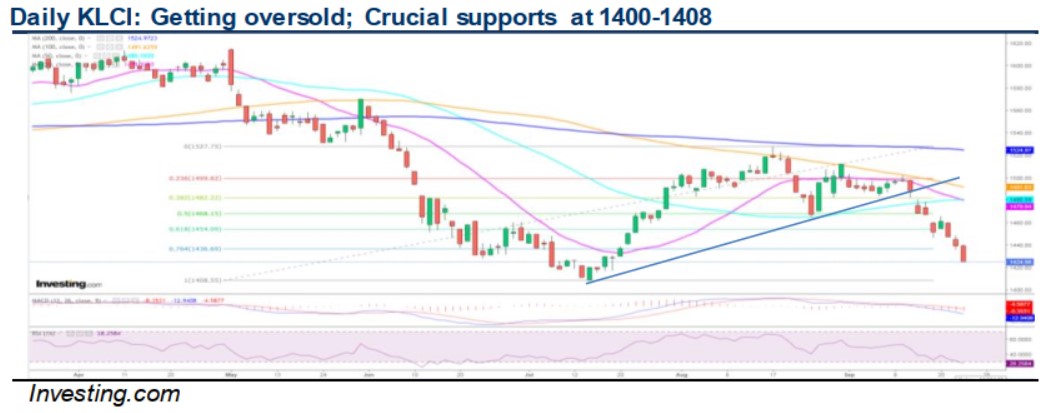

TECHNICAL OUTLOOK: KLCI

The bears are in total control after violating multiple crucial supports to record its 7th decline out of 8 trading days. We reiterate that an extended downward consolidation may prevail towards our envisaged 1,400-1,408 (25M low) supports this week, taking cue from persistent rout from Wall St. Nevertheless, KLCI is getting oversold after tumbling 12% from 52-week high of 1,620, with key supports situated near 1,400-1,408 zones. Major resistances are pegged at 1,436 (764% FR), 1,454 (61.8% FR) and 1,482 (38.2% FR).

MARKET OUTLOOK

Following a 12% selloff from 52-week high of 1,620, any technical rebound from an oversold position in anticipation of potential 3Q22 window dressing and market-friendly Budget 2023 (tabling on 7 Oct) is likely to be brief, capping at stiff hurdles near 1,436- 1,454-1,482 zones whilst key supports are pegged at 1,400-1,408 levels. Overall, Bursa Malaysia will probably remain under pressure in the short term, dampened by lingering headwinds including: (i) global bank’s aggressive tightening policies, (ii) elevated inflation, (iii) heightened geopolitical tensions, (iv) global recession fear, (v) sliding RM (vs USD, 9.8% YTD to 4.58), (vi) GE15 fluidity, (vii) vulnerability of Malaysian corporate earnings and GDP growth in 2H22 and (viii) resumption of foreign net selling in Sep (-RM887m, Aug: +RM1.98bn).

Source: Hong Leong Investment Bank Research - 26 Sept 2022

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

save malaysia!

3

BFM Podcast

4

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

BFM Podcast

8

MQ Market Updates

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....