Stingy Investing

H.Marks 1.0 - Harbour-Link

longterminvest i3

Publish date: Thu, 28 Jan 2016, 03:49 PM

Hello,

My pen-name is Howard Marks.

I am a stingy and conservative investor.

I hate losing money.

I love the idea of money making money.

I believe in passive income.

I don't like speculation.

I love long term investment.

I am loyal to the art of compounding.

I love to invest in undervalued things, tangible (sales) and intangible (equities)

I look at 2 sides of the coin before deciding to pick it up.

Most importantly, I believe in family & friendship above all else.

My pen-name is Howard Marks.

I am a stingy and conservative investor.

I hate losing money.

I love the idea of money making money.

I believe in passive income.

I don't like speculation.

I love long term investment.

I am loyal to the art of compounding.

I love to invest in undervalued things, tangible (sales) and intangible (equities)

I look at 2 sides of the coin before deciding to pick it up.

Most importantly, I believe in family & friendship above all else.

Hello, this is my first write up attempt!

I will focus on value investing concepts, and to hunt and highlight hidden gems that might have been otherwise unnoticed by the public. I am providing honest opinion based on 2 sides of the coin, so that an investor can make their own independent decision on whether to put in an investment or not.

HARBOUR-LINK GROUP BHD (2062)

QUALITATIVE REVIEW

INDUSTRY

Overview

Notable Competitors (Peers)

- Tiong Nam (integrated logistics)

- Century Logistics (integrated logistics)

- SysCorp (shipping)

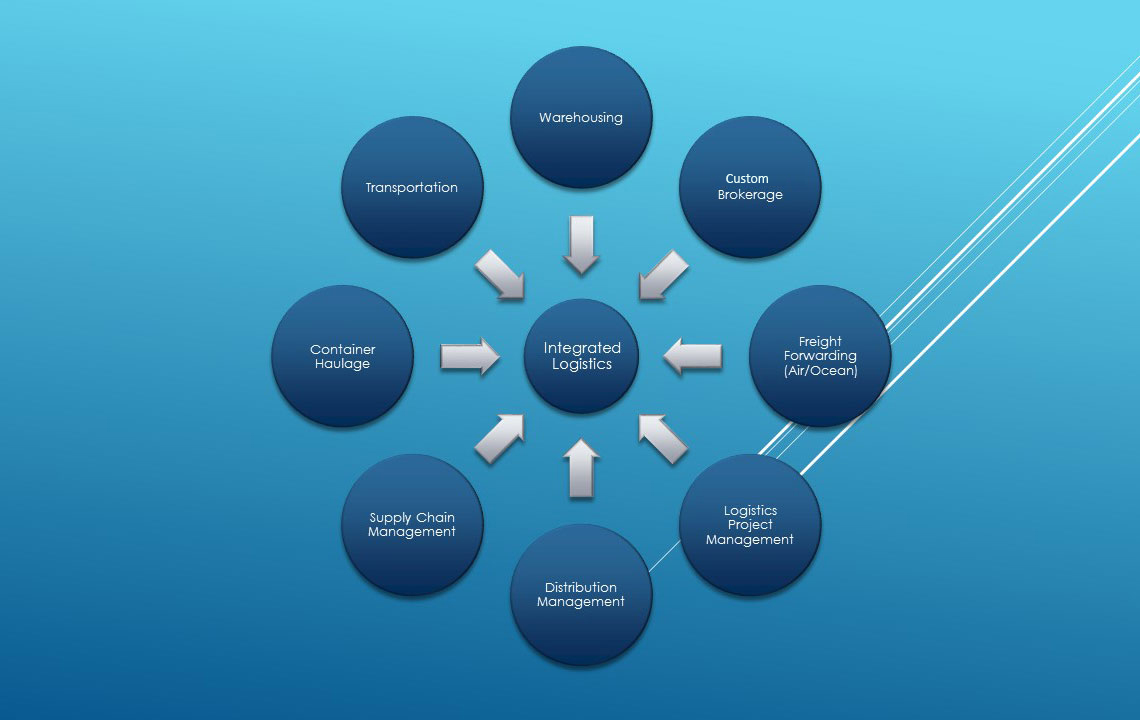

BUSINESS

Core Businesses

Harbour is based in Bintulu.

It primarily deals in 5 types of businesses:

- Shipping & Marine Services

- Logistics Services (incl. warehousing, customs clearance, etc)

- Heavy lifting & haulage (Crane & Equipment)

- Engineering Works (O&G)

- Property Development & Construction

Competitive Advantage (Moat)

- Branding; 1 look at their name and their logo and you will know that they are dealing with logistics. The name is catchy and easy to remember.

- Website looks modern. This reflects that the company is open minded and able to accept and adapt to new changes, even though the company has been established for a long time.

- Very experienced management team.

- High barrier of entry - High CAPEX required to acquire machinery. Being a large company means they can achieve economies of scale and force prices lower due to lower inventory costs, which smaller companies can't achieve.

- Reputable company - they must be doing their logistics business right, for being able to dominate >50% market share in East Malaysia.

- Able to receive higher margin due to the correct business model of integrated logistics. From vessel services, to crane rental for lifting, to trucking and warehousing. "Bao-ka-liao"

- Asset Play; Acquired 53 hectares of industrial land beside Bintulu port, GDV of MYR 1 billion - Land, especially industrial land appreciates very rapidly if they are located beside ports, due to the reduction of costs required for inner-land transportation. If they play their cards right, they can either do rental which give high recurring income, or build it into a industrial township. An alternative cunning thought, they can also play the "bully game" by forcing others to be located further away from the port, therefore "forcing" them to use their transport.

Business Risks

- Competitive freight rates for shipping segment. This is reflected by the low operating margins.

- Unsure of what future projects can they capture. 60% of earnings growth in FY15 depend on logistics services and crane business, which is getting their profits from the construction of RM1.8 billion Samalaju Industrial Park. The park is projected to complete by 2017.

- Reduced business due to lower crude oil prices; According to Wikipedia, Bintulu has estimated 85% of natural gas, and 50% of crude oil in Sarawak. Therefore a majority of income coming from Bintulu derives directly or indirectly from O&G sector.

- Chairman is conservative on future growth prospects based on the upcoming economic downturn.

- Reduced trade flow due to forecasted economic downturn.

- The Baltic Dry Index which is a representation of ocean freight prices have been falling. This will prove to be a bad sign for Harbour's shipping arm by reduced operating margins.

Growth Drivers

- Continuous low oil price = increased profit margin. Already reflected in FY15. Oil not expected to rebound in the near term.

- Benefit from Samalaju-SCORE project; by getting increased cargo volume. Acquired 2 new container vessels with 700 TEU capacity.

- MNCs especially heavy industries may take advantage of the weaker MYR by establishing new plants in the region, therefore increasing business flow for Harbour.

- Pan Borneo Highway; Potential benefits directly (via construction, lifting and logistics income) and indirectly (boost of road logistics due to improved transportation network)

MANAGEMENT

Director Profile

- MD, YONG PIAW SOON, 63 - Founder in the forwarding industry in East Malaysia since 1975. Got an honest and reliable face. ha ha.

- Director, WONG SIONG SEH, 53 - Founder, in the shipping industry since 1980s

- DATO’ TOH GUAN SENG, 60 - Founder of Eastern Soldar Engineering & Construction (ESEC). 40 years experience in O&G industry.

- LAU SII HIN, 64 - 30 years experience in transportation, inventory and mechanical industries. Key person for overseeing workshop repair, maintenance, ordering of spare parts, day to day operations.

Comments:

-Very well experienced management team. Each of the directors have a specific branch to focus on, therefore showing professionalism in the company. The MD leads the company, and based on his background he walks the talk.

Chairman's Statement

The MD, Yong Piaw Soon, has been very frank that the future outlook of the company will be challenging due to the economic slowdown. This is a good sign, as it shows that he is willing to admit on potential failures or mistakes. He has also added that they are confident to weather it out. We must test on this by studying the company's cash ratio.

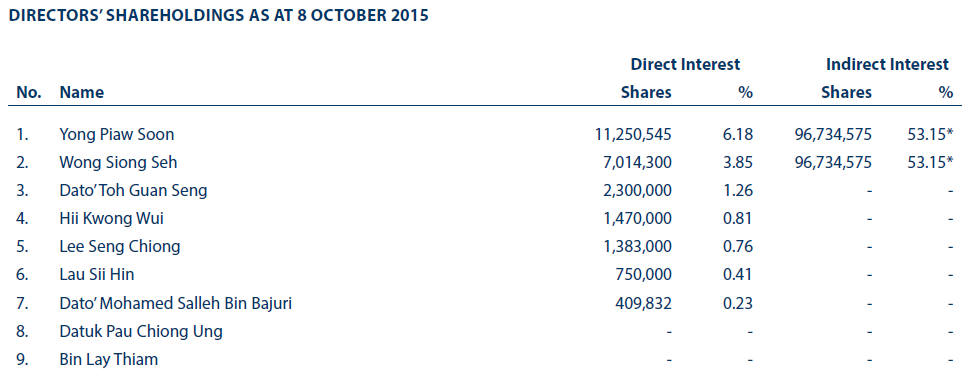

Renumeration

From the above 2 pictures, we can see that the director's renumeration is at 5,136,874 / 54,641,961 = 9.4% which is reasonable for a "typical Malaysian Chinese company". The average is about 10%.

Shareholder Statistics

I like it that their founders are majority shareholders. Combined with their renumeration, this will mean that they are more likely to act inline with shareholder's interest, by either increasing shareholder's value or by giving out dividends.

Insider Trading

There are no insider trading for 2015. If the company or the shareholders are doing buyback it would show that they are confident of the company based on the current share price or they are aware of some "insider info" that the public does not know yet.

NUMBERS

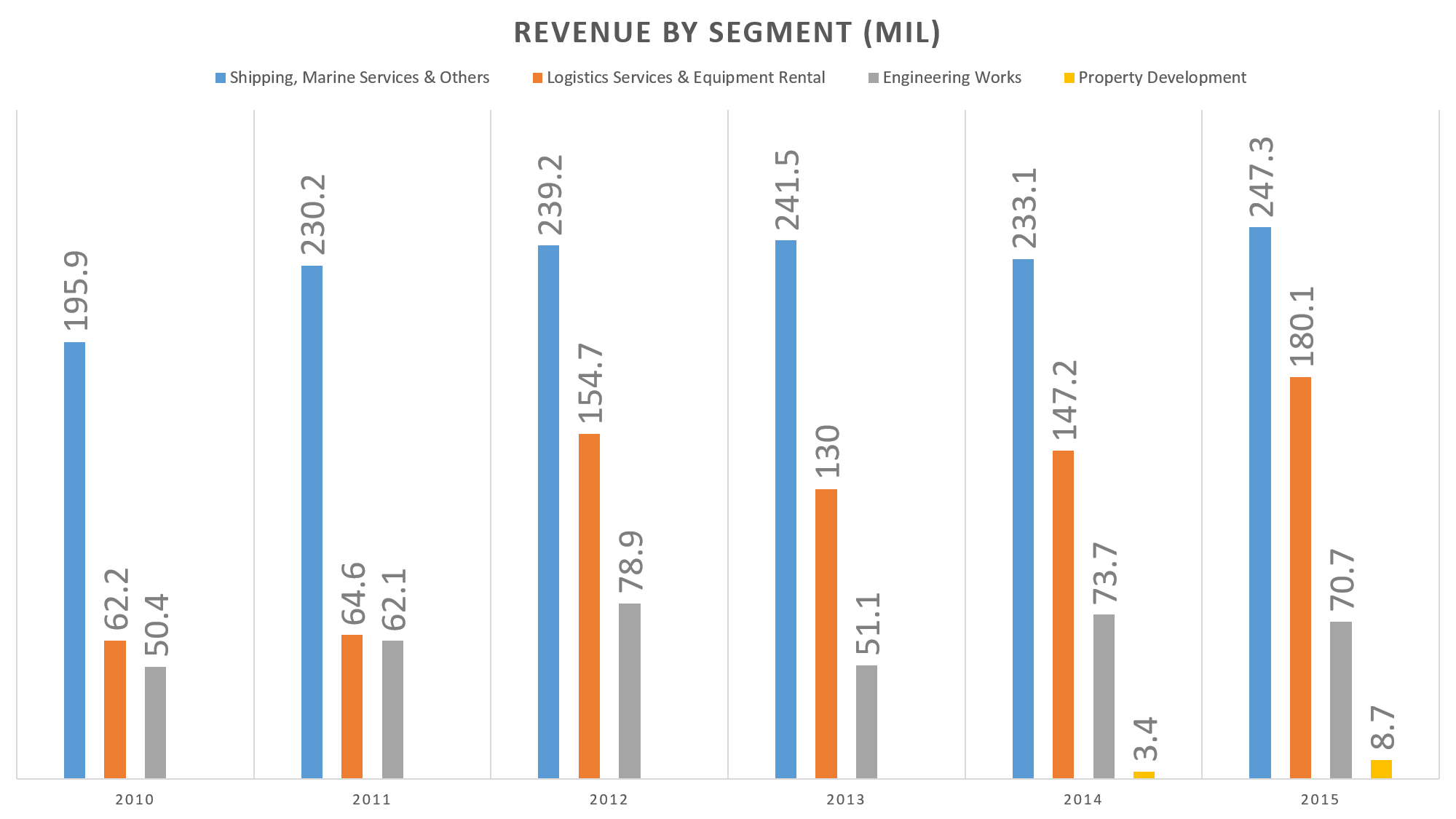

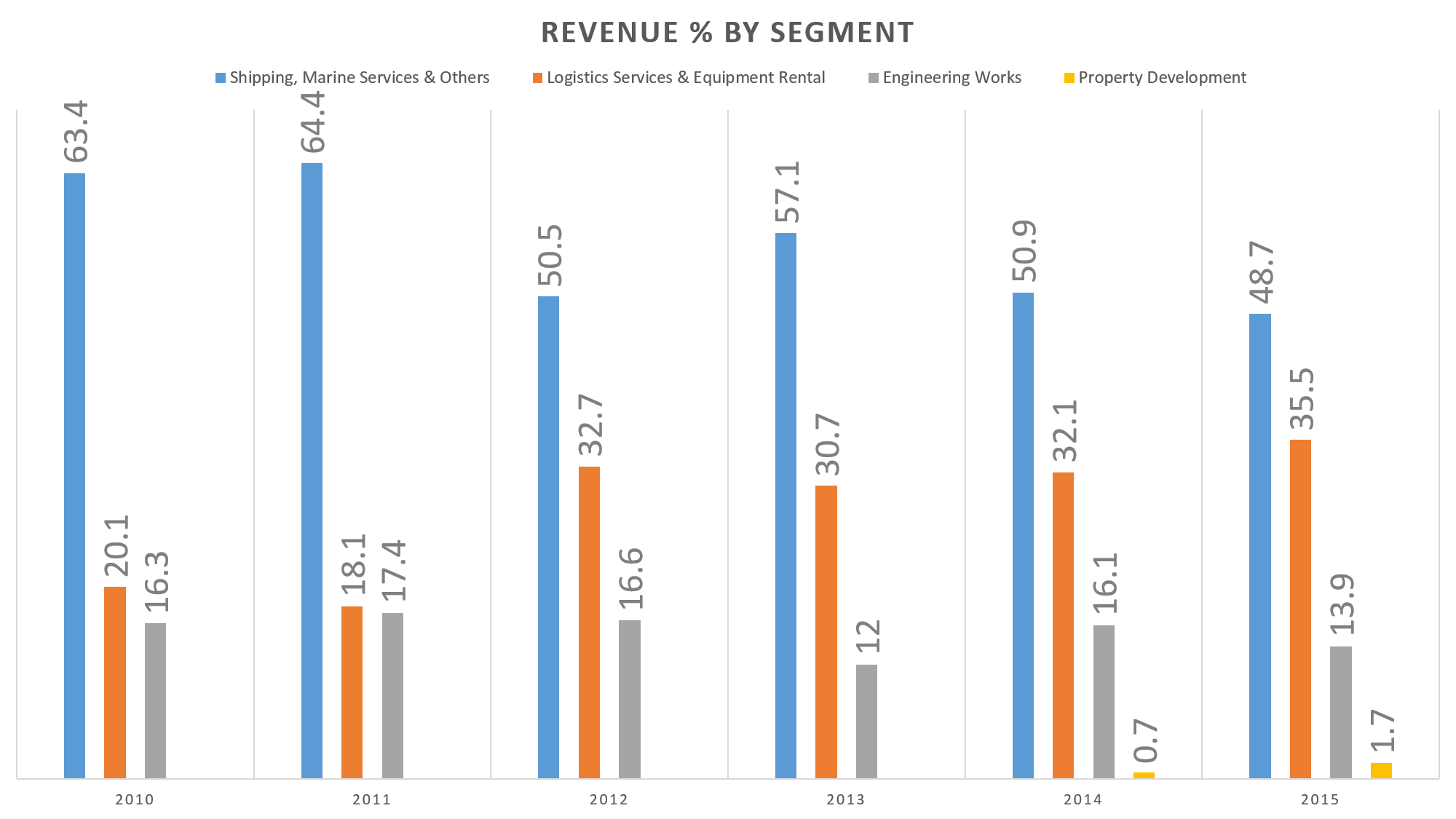

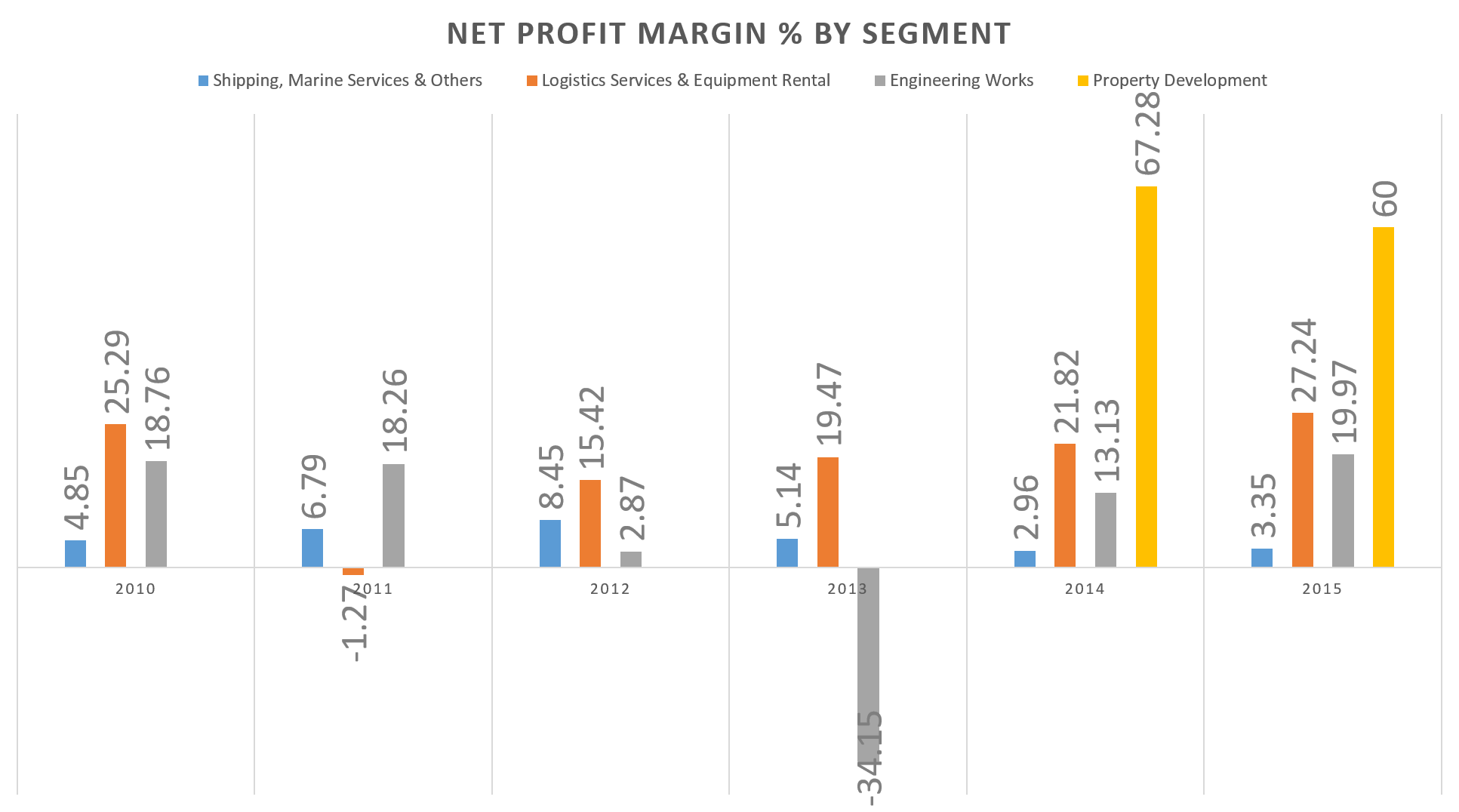

Segment Analysis

We can see that the revenue from shipping, logistics and engineering has been on a steady increase.

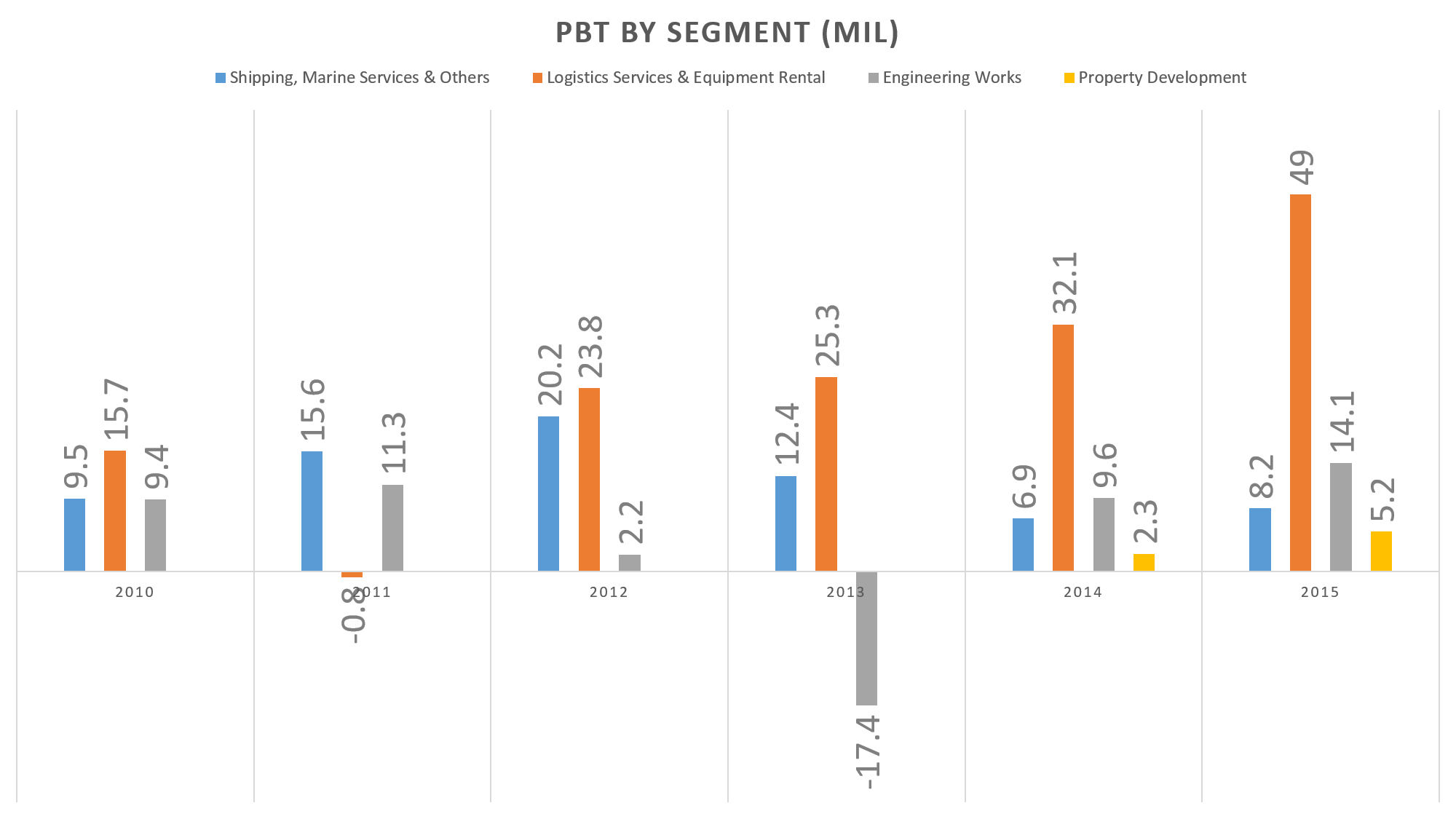

We can see that the profit before tax has been increasing for the logistics business except in 2011.

From revenue % standpoint, the shipping services has been on a steady decline since 2010. The reverse can be said for their logistics and equipment rental business.

Viewing the NPM, the logistics business has been increasing since 2012. The engineering margins is very unstable. For the shipping side, the margins has been on a decline since 2012, perhaps due to intensive competition from numerous local players.

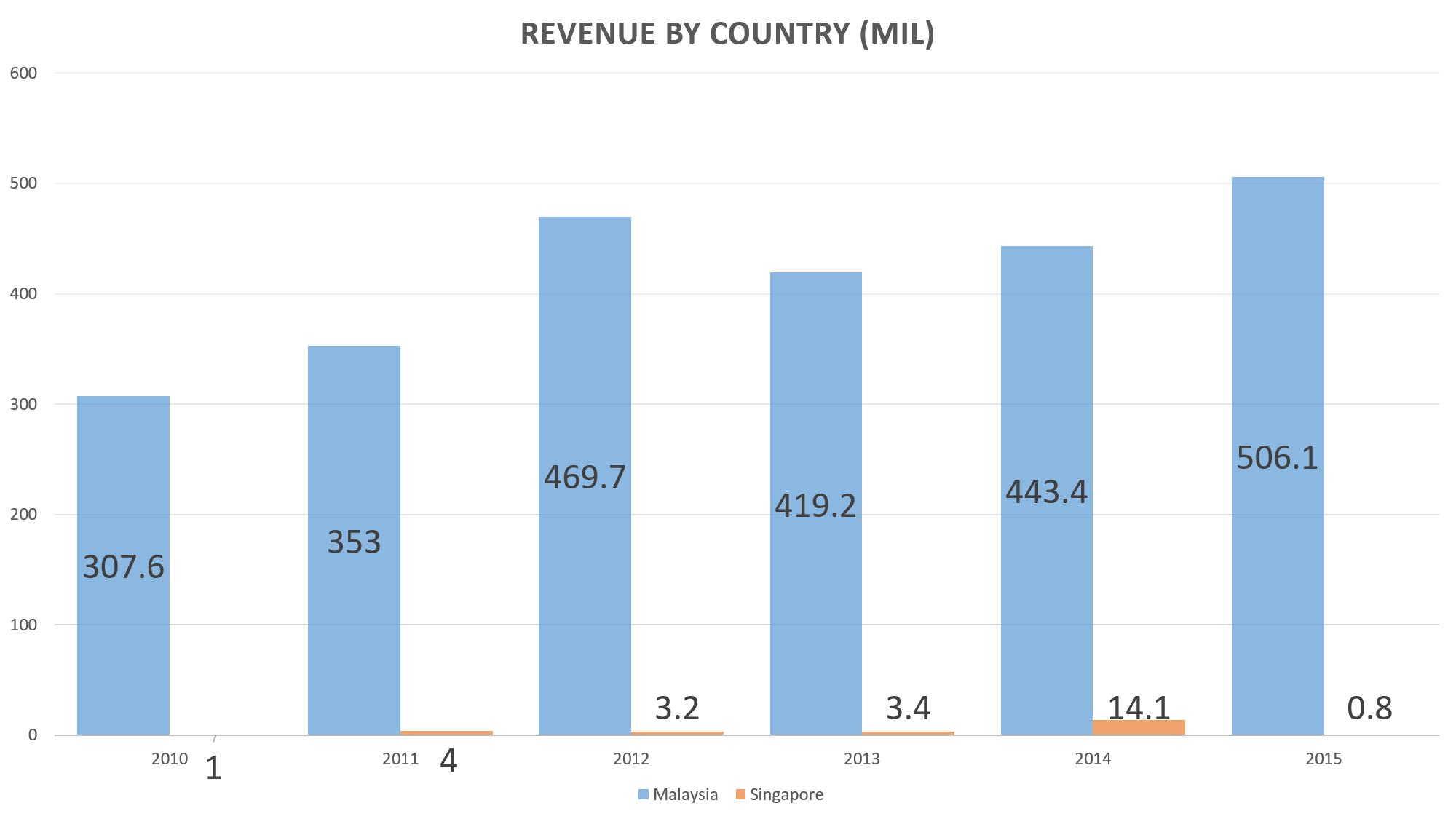

Apparently Harbour also does business in Singapore, earning a commendable 14.1 million in 2014. However that revenue has virtually vanished in 2015. Very unusual.

In the annual report, HLLines incorporated a new subsidiary called Harbour-Link Lines (S) Pte. Ltd. with a paid up capital of $1. The intended principal activities is shipping agencies.

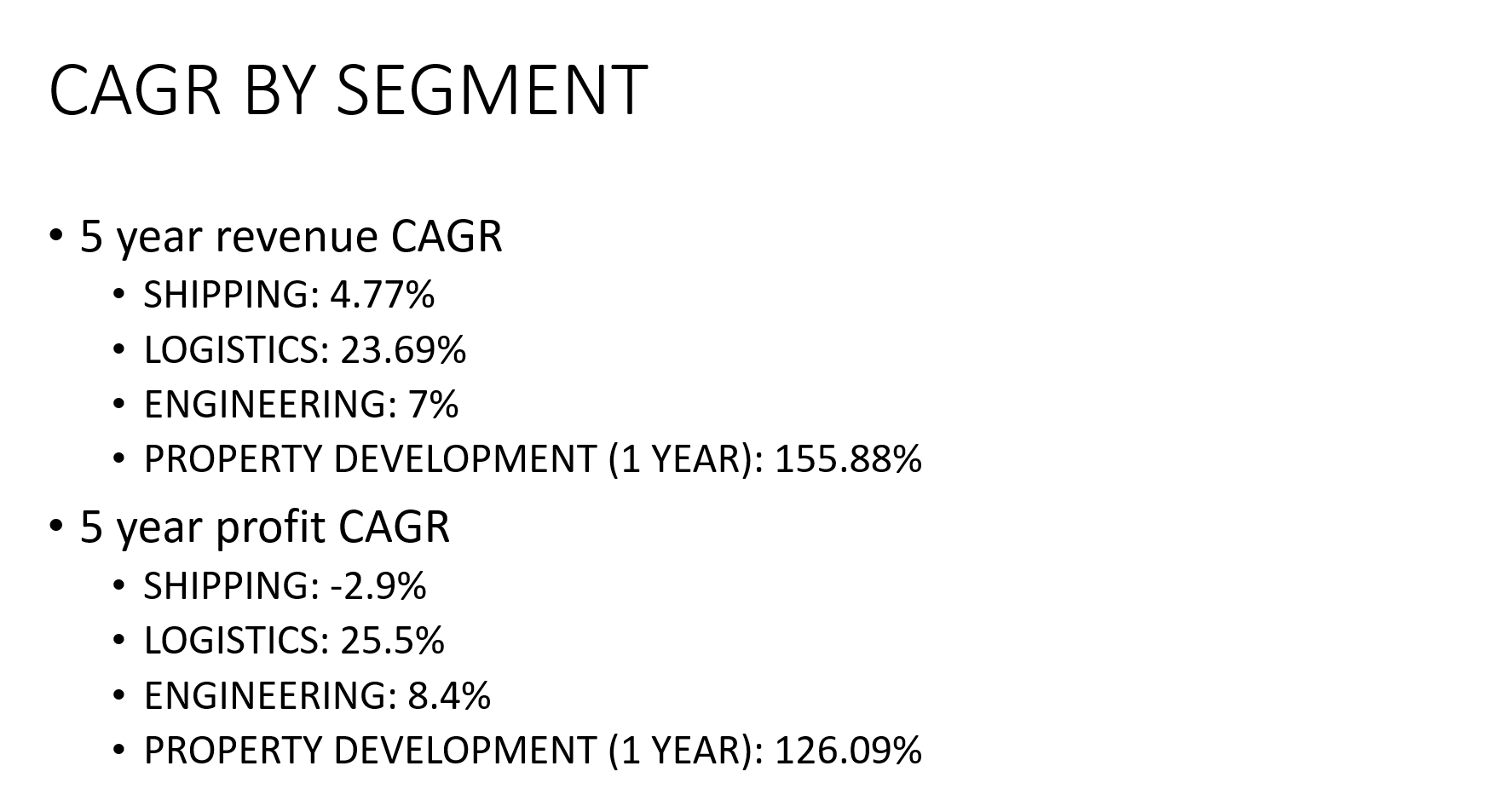

As for CAGR, we can see that their logistics business has been growing, at 20+%. Their shipping business has been on a decline.

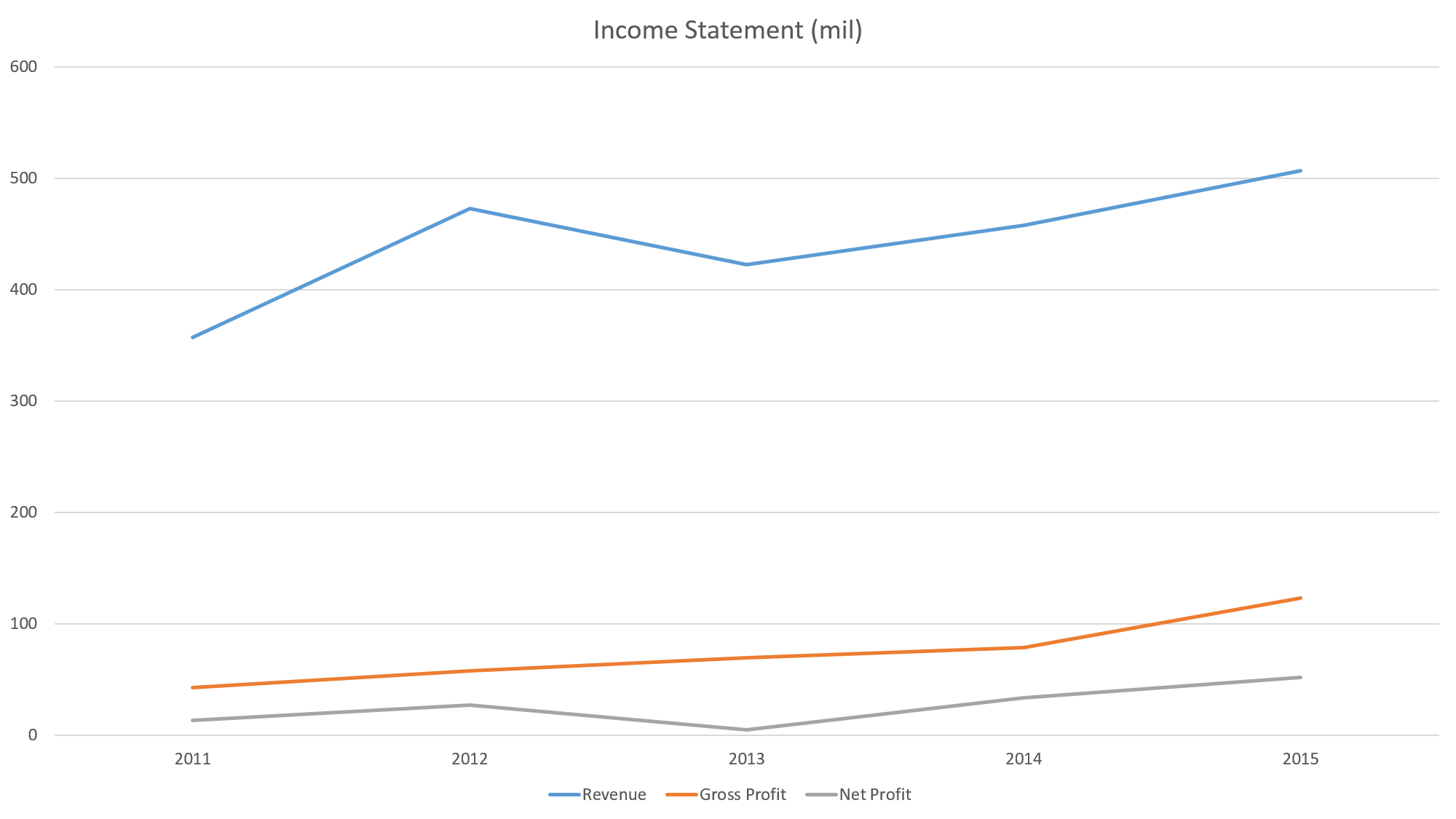

Income Statement

Comments: A sharp drop in net income in 2013.

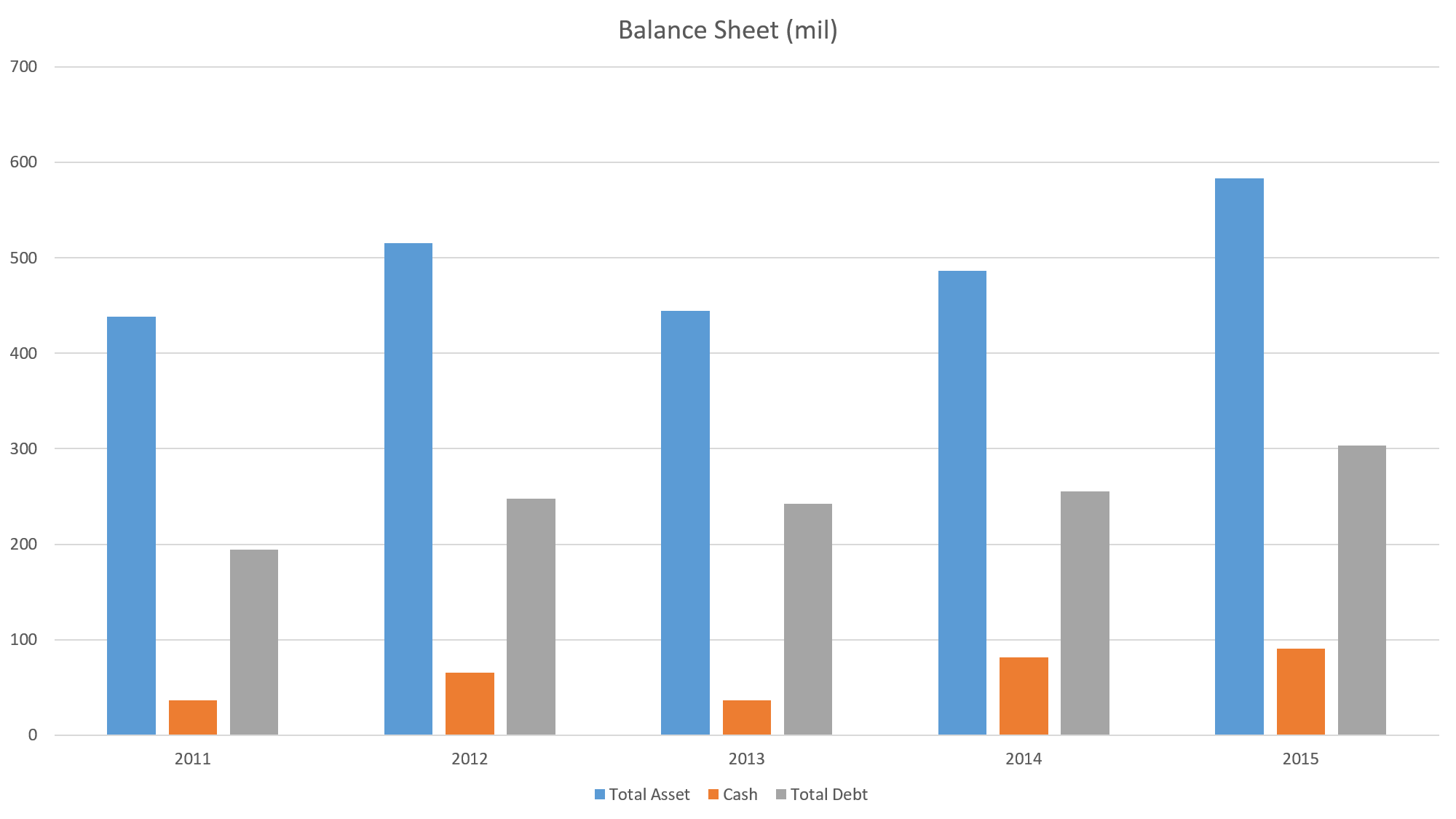

Balance Sheet

Comments: Why 2013 Dropped? Since 2013, assets has been increasing.

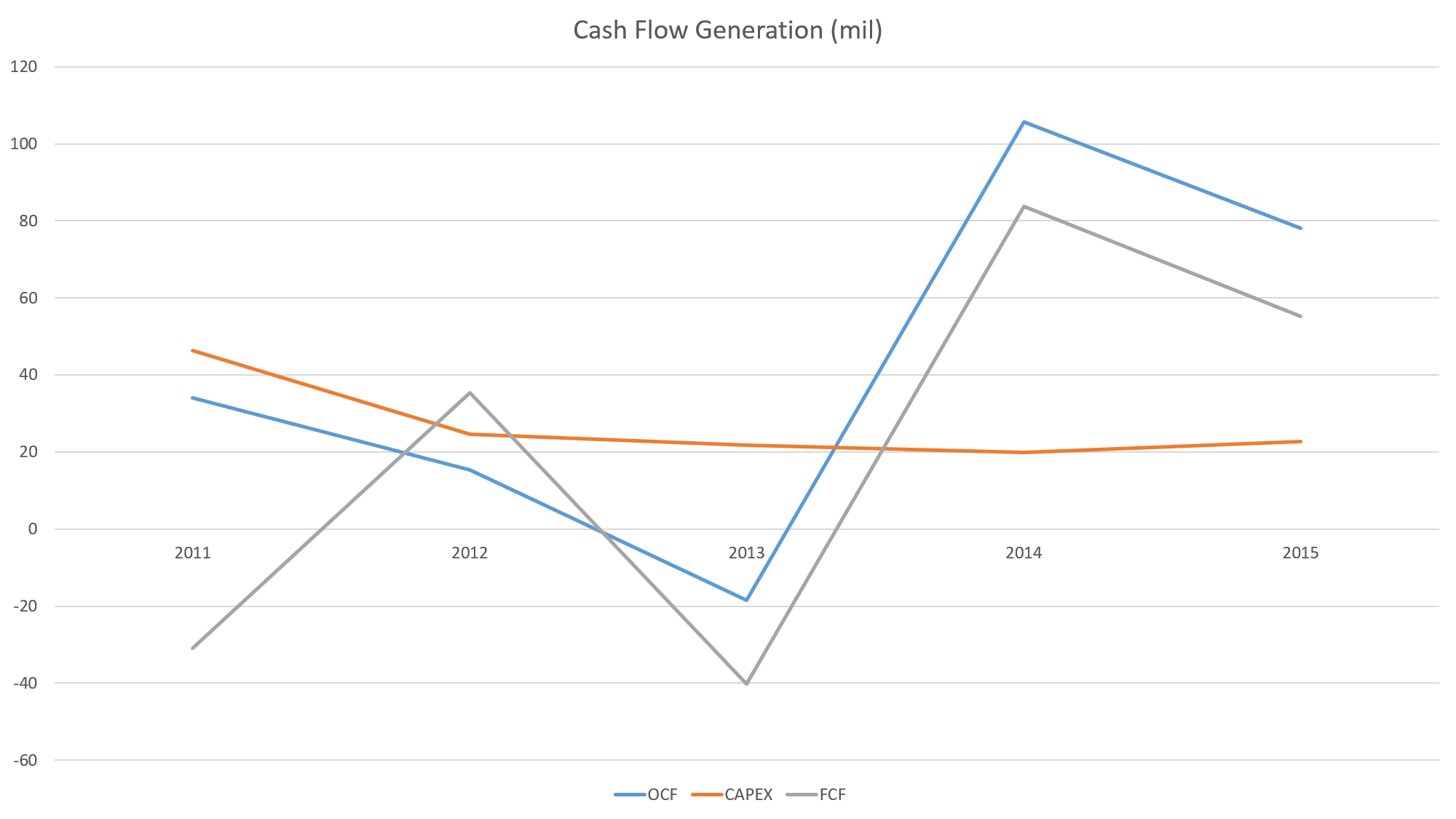

Cash Flow Statement

Comments:

Capex consists of purchasing of property plant and equipment + purchase of prepaid land lease payments. I would assume theat their yearly maintenance capex is around 20m for their transport business, which requires regular maintenance, whilst in 2011 they paid for land lease, which I believe it is for their property development arm.

In 2013, they have been clearing a lot of trade payables, which means paying money that they owe to their suppliers, therefore we can see a dip in the operating and free cash flow. In 2015, they have made a lot of deals but have yet to collect the $, so their trade receivables ballooned to 48m. This means they have to pay for tax for these sales but they have yet to make the money.

FINANCIAL RATIOS

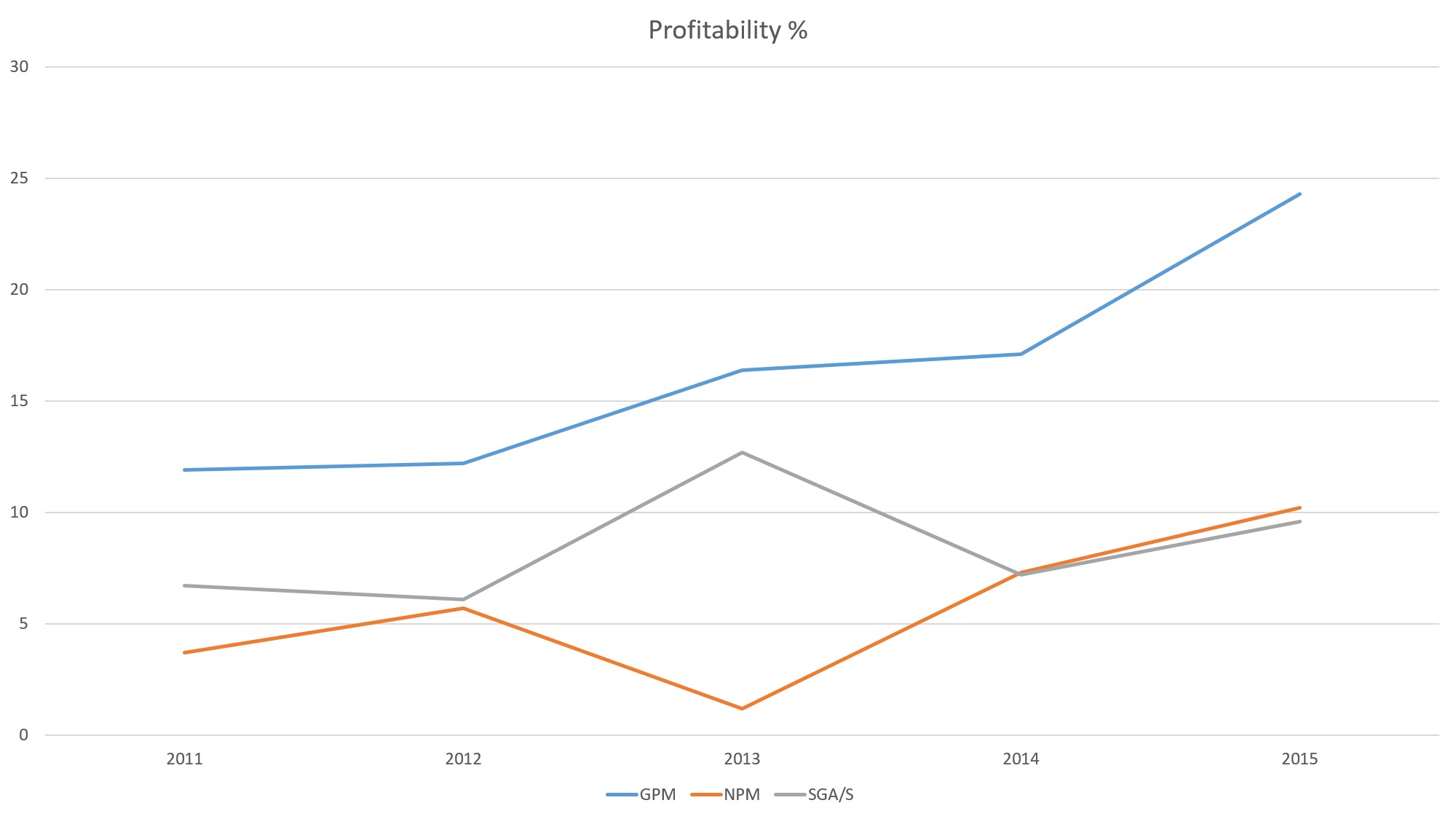

Profitability

Comments:

In 2013 their expenses increased to 12% over sales, which result in the net profit margin to sharply decline. Refering to below, debt has increased sharply.

Gearing & Liquidity Ratio

Comments:

Debt to Equity is within comfortable range.

Cash Ratio is not too good, which means they have limited spare cash, and are unable to pay off all their current liabilities immediately.

Current Ratio is good, they have more than enough current assets to cover their current liabilities, in case of bankruptcy.

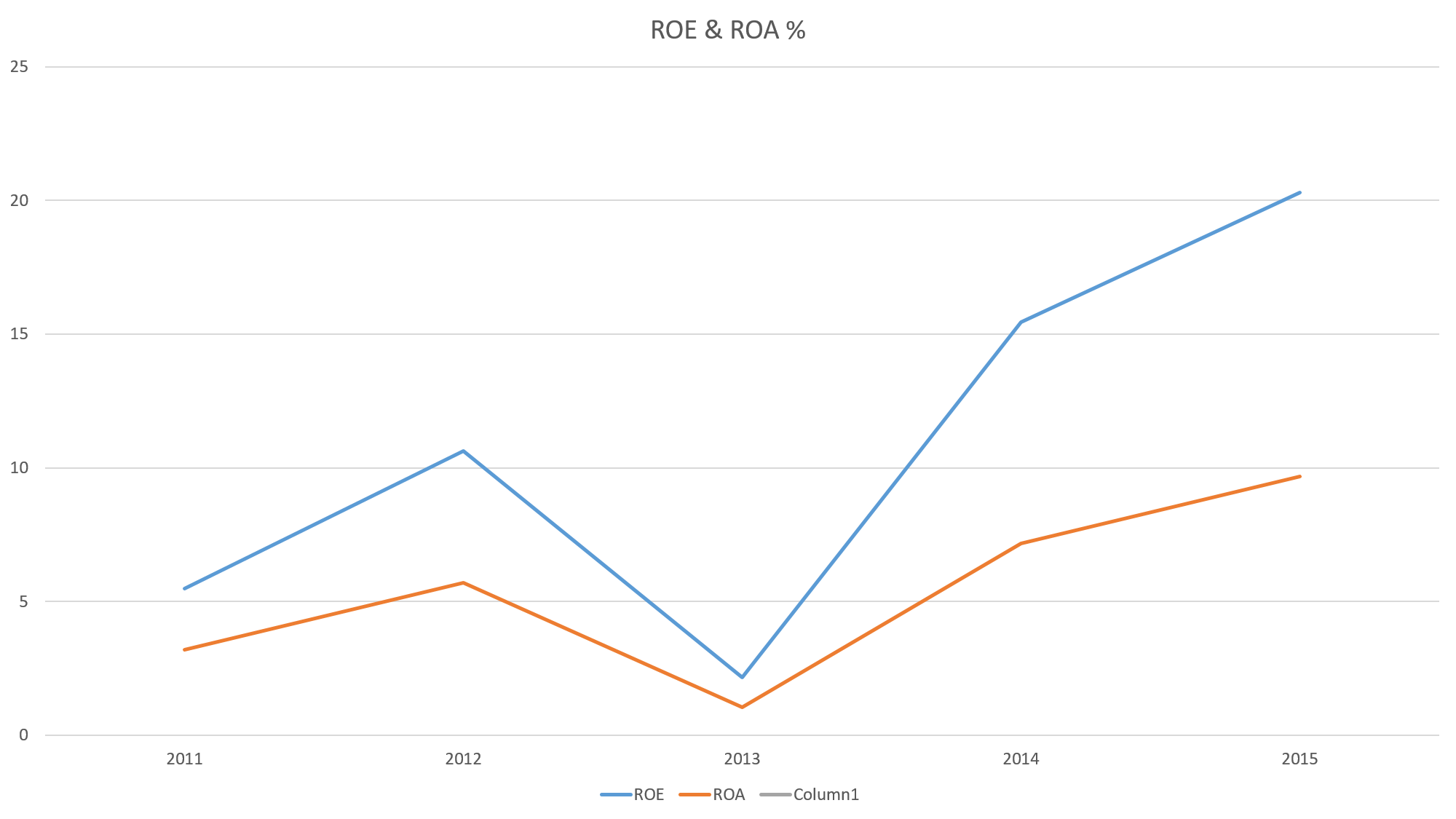

ROE & ROA

Comments: Except for 2013, their ROE has been steadily increasing.

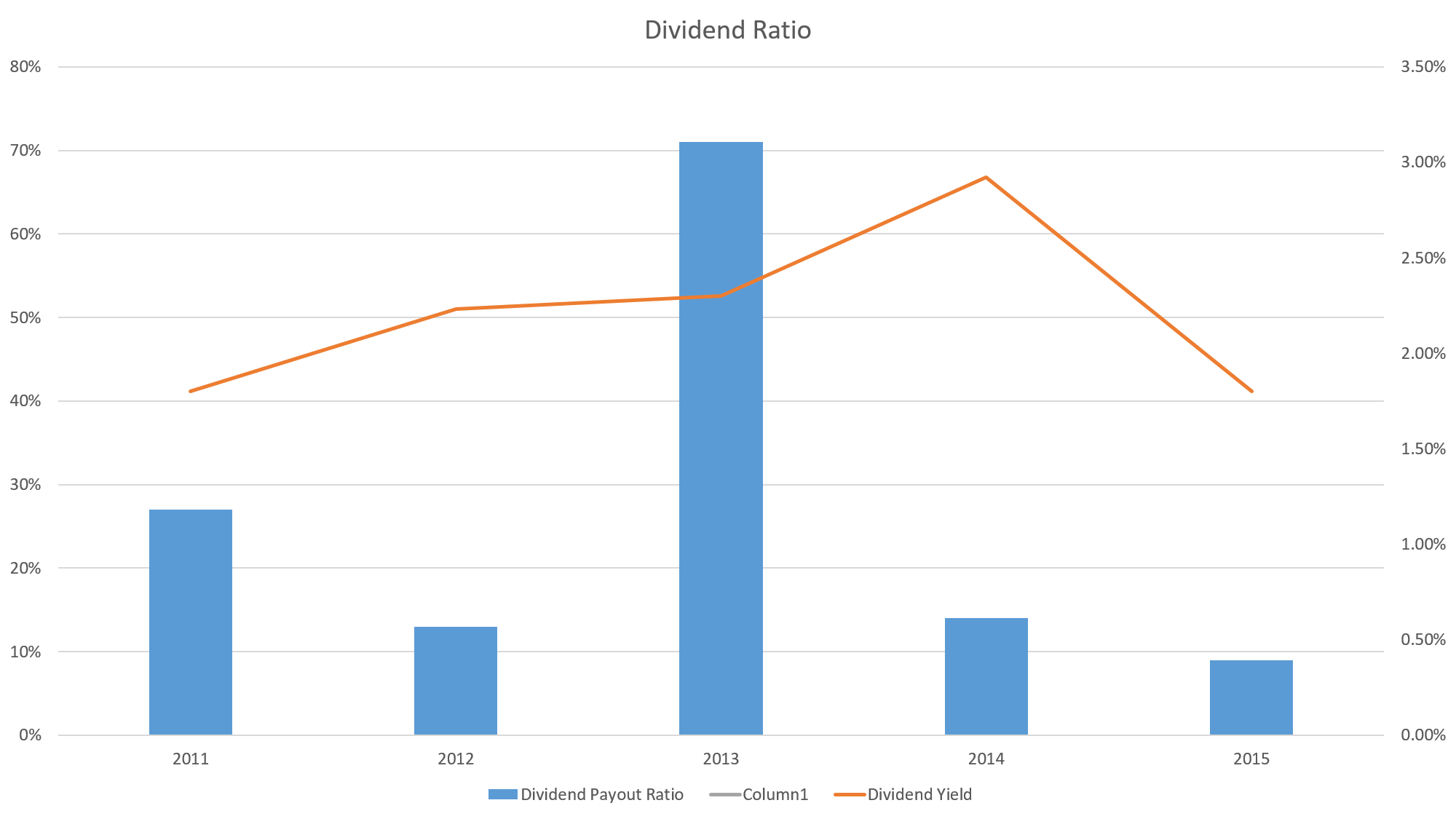

Dividend Ratio

Comments: The dividend yield has been at a steady 2-3% range. Take note that this is applicable even as the share price is going up. Which means that the dividend is growting in line with the increase in share price. If you have bought at RM 1 in 2013 which fetched around 2.5% yield, going forward, with the price at $3, your yield will be at 7.5% which is higher than the current FD rates, not taking into account the capital gains!

VALUATION

Historical Share Price

Historical Valuation

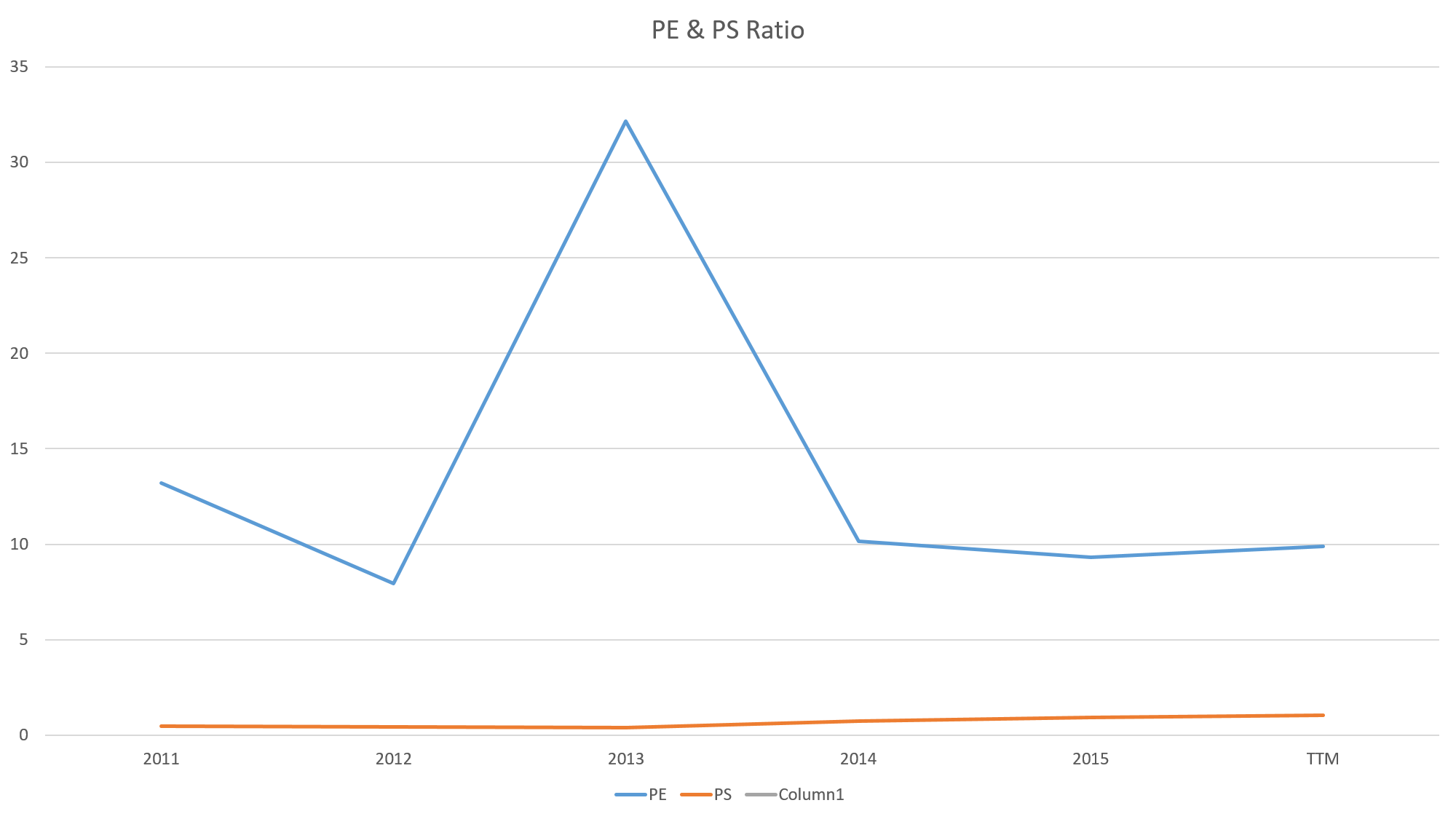

Comments:

Comparing the share price and PE, we can see a spike in PE ratio during 2013. Looking from the income statement, it appears that in 2013 there is a sharp fall of net income. From the chairman's comments, we can see that it is due to the completion of some projects.

Discounted Earnings Model

Using the discounted earnings model:

Intrinsic Value based on a 5% growth for 10 years, 6% min. rate of return, EPS at 28.46 cents (including net cash per share) = RM 2.70; -0.93% Margin of safety (FAIR VALUE)

Comments:

I am projecting a very conservative growth rate at 5% in line with the current market conditions, however I am actually quite confident that based on their current dominating strength of over 50% market share, they will be able to weather this unstable market, and actually achieve 10% yearly growth. So I am being very conservative here. In addition, their business actually hedges on both sides of oil direction, if the oil price slumps they are able to enjoy high margins from transportation businesses, whereas if oil prices increase, they are able to do more oil-engineering businesses.

In 2013 which we can see sharp drops in profits, and this is attributable to "impairment of goodwill" and "completion of equipment supply contracts"; and we can see this from the PBT by Segment chart, and most of these are a result from the engineering side. Hopefully this is a 1 time problem and they have corrected their mistakes.

Ask yourself, do you see that this company will stop doing business or be overtaken by another competitor in the next 5-10 years? If yes, who? If no, good!

ADDITIONAL INFO:

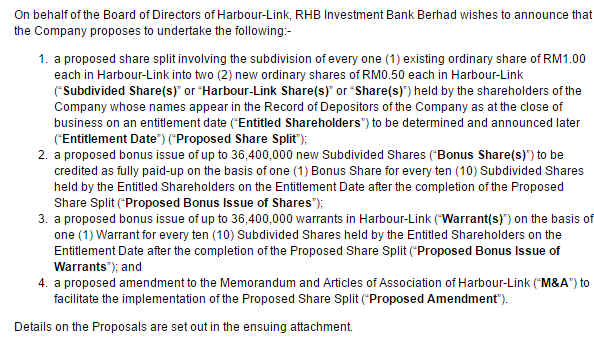

The management has been proposing a stock split of 1 to 2, which means the current price will be halved. In addition, there will be bonus shares of 1 to 10. Furthermore, they will be issuing 1 warrant for every 10 shares. These sounds like goodie bags given, as I can't see the catch (it is not issuing new rights to raise additional funds).. The real catch is that the price will definitely fall after the split, which might affect the psychology of Mr. Market.

End

"Price is what you pay, value is what you get"

Please leave some comments on how to improve my writing! :)

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

2

3

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

4

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

5

Mercury Securities Research

6

BFM Podcast

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Ven Felix

Richard Lim, a very good write up. Like !

2016-01-28 16:17