JF Apex Research Highlights

Econframe Berhad - Opening new doors of opportunities

Summary

- Econframe engages as a total door solutions provider and commands approximately 60.0% market share in the metal frame doors segment in Malaysia.

- We project core earnings to accelerate from on-going business expansions within the sales for manufacturing segment and investment from the acquisition that was completed in recent times.

- Econframe is valued by pegging FY24F core EPS of 5.45 sen to PE of 22.0x, leading to a FV of RM1.21 (45.8% potential upside from current price).

Company Background

Econframe Berhad (Econframe) history traces back to 2001 and has now evolved into one of the leading providers of a total door system solution provider for residential, commercial, mixed, and industrial properties.

Several services offered include design and manufacturing of metal door frames, production of fire-resistant door sets, manufacturing of metal doors, and trading of wooden doors and ironmongery. Ironmongery and fire-rated doors are categorised under a separate brand called DUROE. Meanwhile, metal doors and window frames, iron doors, and wooden doors are all part of the Econframe brand.

Since May 2010, the group has been undergoing a transformation plan, during which they registered their trademark ECONFRAME and introduced their brand to the market. The group also initiated the trading of ironmongery and fire-resistant door sets as part of business expansion.

Econframe predominantly serves real estate developers, offering customised door and window frames, along with various associated products catering to diverse construction requirements. Notable clients include well established local property and construction players such as ECOWORLD, GAMUDA, IJM, LBS, SPSETIA, and among others. With contracts secured from reputable developers and contractors, the group faces lower risks of running into payments insolvency. It is worth noting that a significant portion of contracts comprises residential properties.

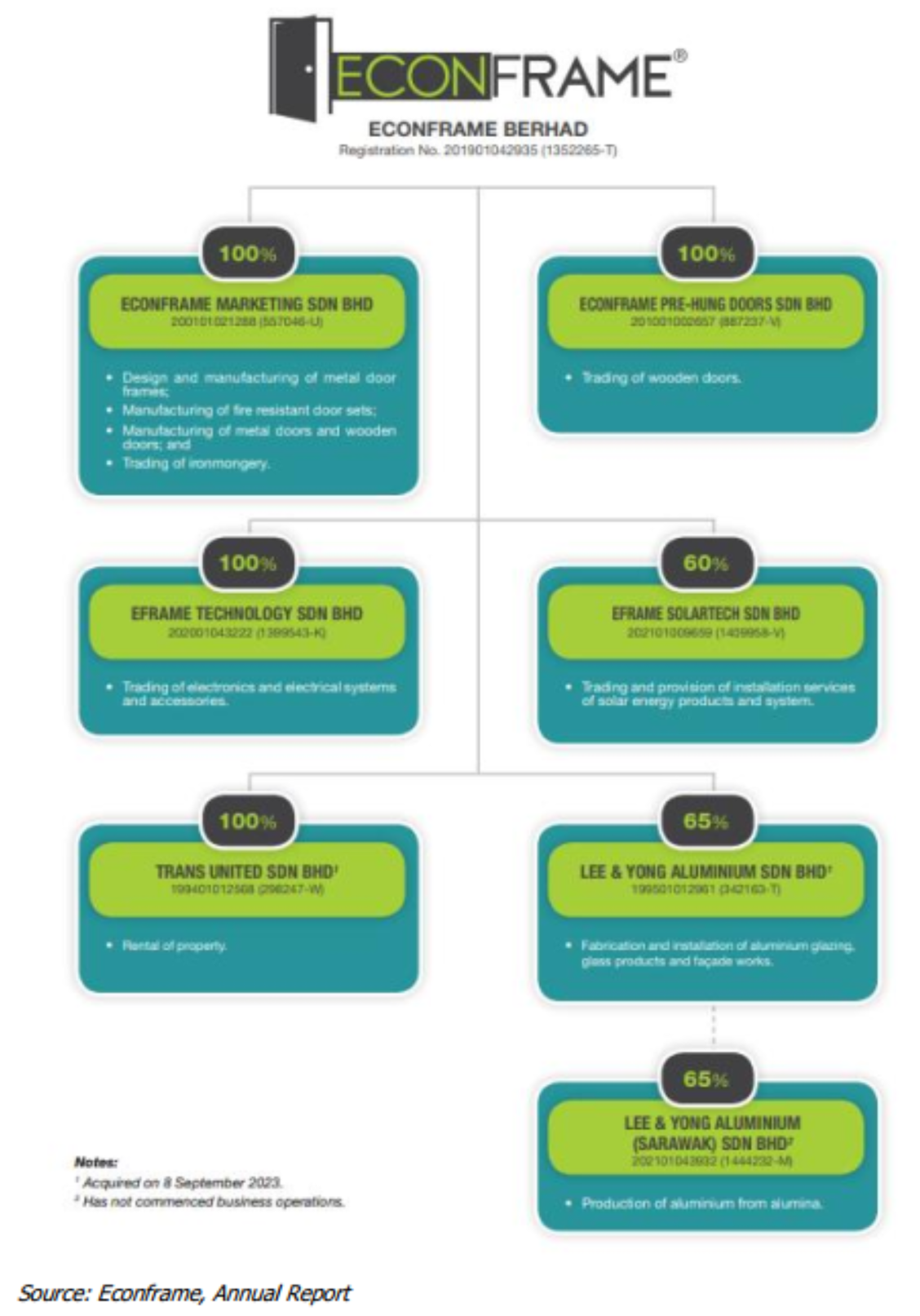

The group has been actively undertaking merger & acquisition activities in bid to achieve synergistic values, such as Lee & Yong Aluminium Sdn Bhd (LYASB) and Trans United Sdn Bhd (TUSB) in early 2023, with a profit guarantee of RM4.0m annually for three years. Additionally, a proposed acquisition of ETA World Sdn Bhd (ETAW) on 15 January 2024 marks another milestone which allows Econframe to tap into ETAW's expertise in industrial property development, capitalising on favourable market prospects.

Corporate Structure

Business Overview

Econframe provides comprehensive door system solutions for property developments. Notably, the group produces and markets their proprietary products, which encompass DUROE fire-rated doors and ironmongery, along with ECONFRAME metal door and window frames, iron doors, and wooden doors. Over the years, the group company has successfully marketed and sold a diverse range of over 100 different products.

Metal door frames

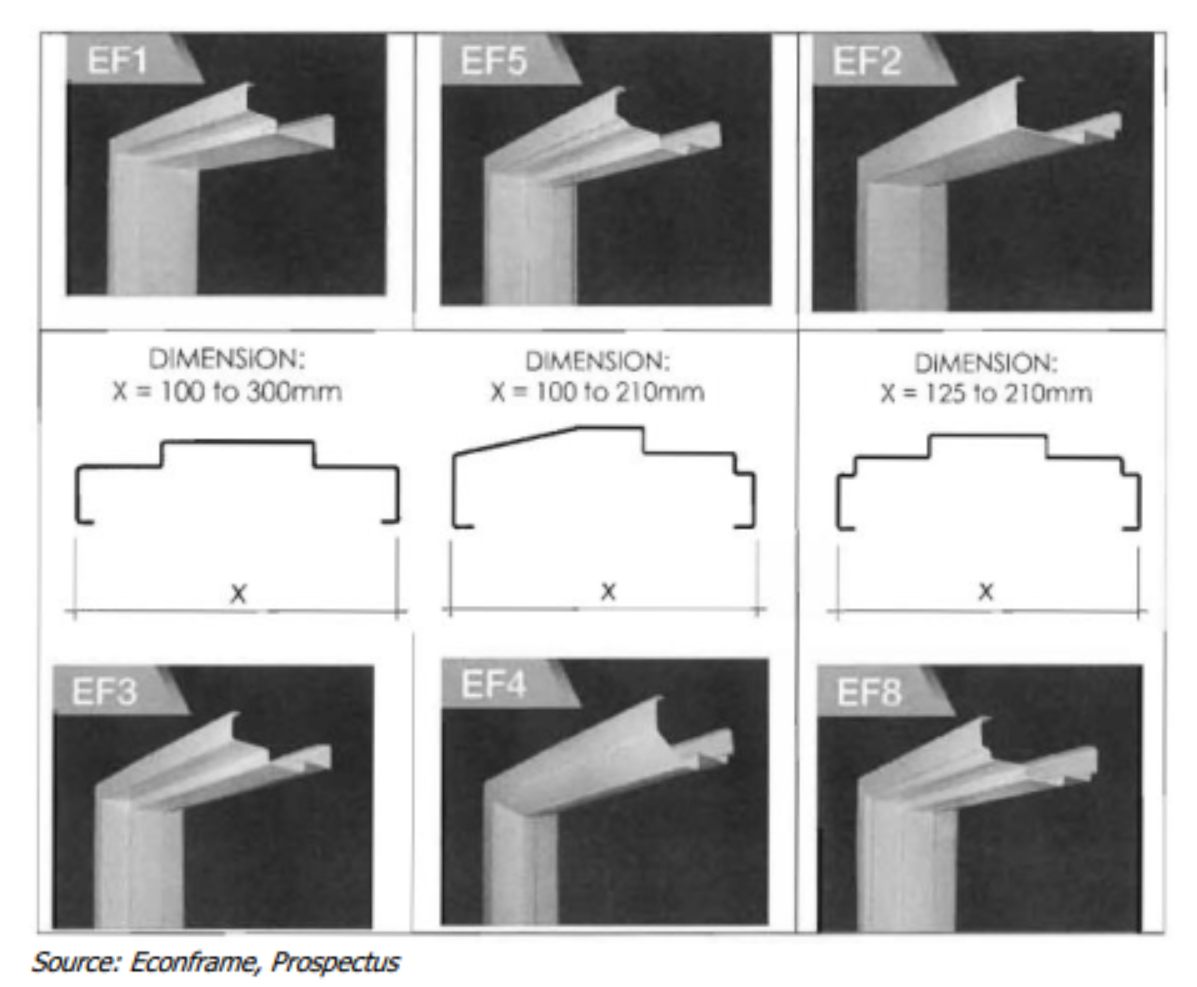

The group specialises in manufacturing metal door frames for new residential, commercial, mixed, and industrial properties. The frames are installed during construction phase, which provide support towards wall strength and can either be flush or protruding. Various factors such as wall type, thickness, installation method, material types, dimensions, aesthetics, and cost are deemed crucial considerations during the design stage.

Collaboration with architects, contractors, and property developers helps establish profiles and dimensions, accommodating customisation based on specific project requirements. Metal door frames, sold under the ECONFRAME® brand, can be standalone or part of a total door system solution.

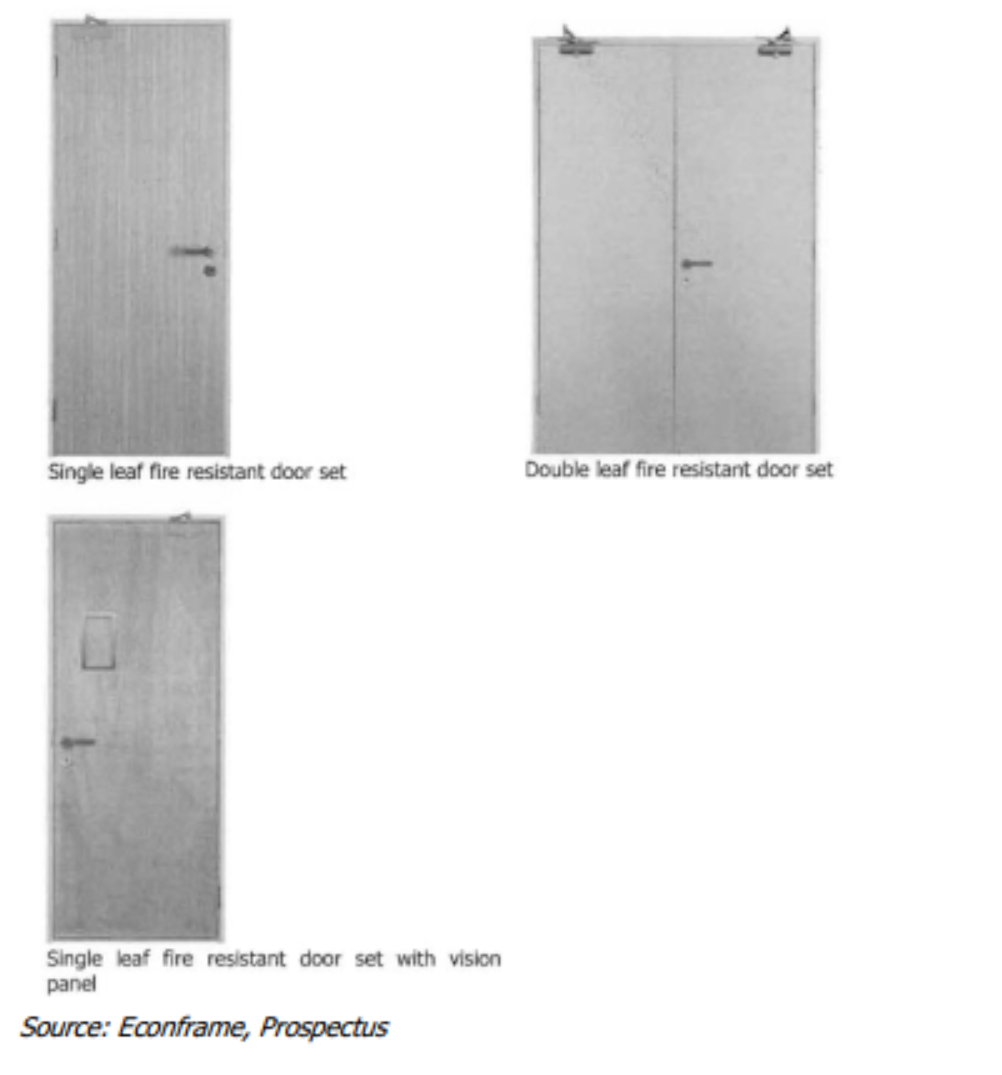

The group has also manufacture 7 types of fire-resistant door sets that adhere to meet SIRIM guidelines, with components certified for fire ratings. These door sets, rated for 1 or 2 hours, undergo safety testing and are approved by BOMBA. Sold under the DUROE® brand, they bear the 'MS' mark in SIRIM's product certification. The fire-resistant doors are constructed with fire-resistant boards, insulation, and outer layers for aesthetics. Rigorous testing, including furnace tests, ensures compliance with fire resistance and duration standards.

In this segment, the group also offered leaf double fire-resistant doors, providing the option of integrating a vision panel or door viewer into the door panel. Leaf fireresistant doors refers to single-door fire-resistant doors, while the term "double door" are fire-resistant doors consisting of two doors.

Fire resistant door sets

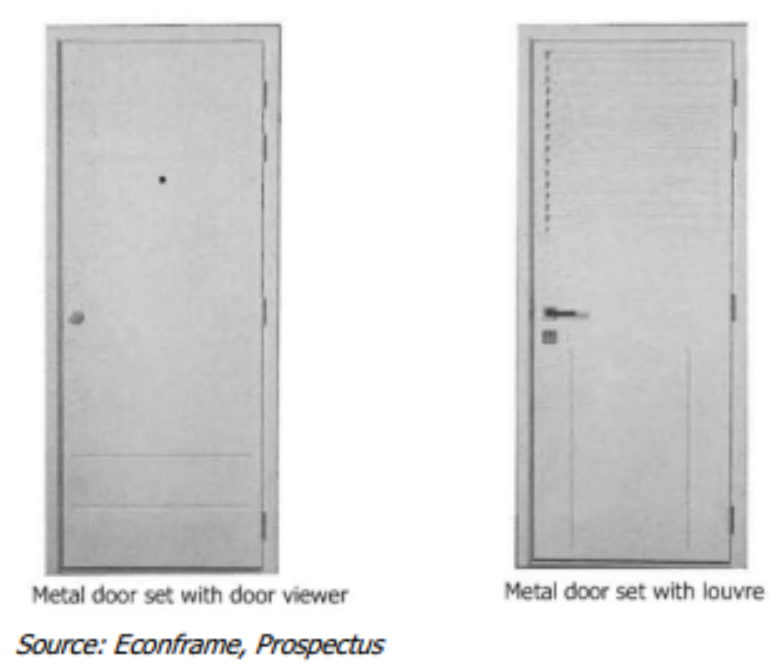

The group offers customisable metal doors with design flexibility in terms of width, height, and thickness. Metal doors are manufactured in-house, featuring an outer layer of galvanized steel sheets, including Zincalume®, electro-galvanized, and 1.2mm thick galvanized iron, filled with a honeycomb core. Marketed under the ECONFRAME® brand, the doors are sold independently or as part of a complete door system along with metal door frames and ironmongery.

Metal door sets

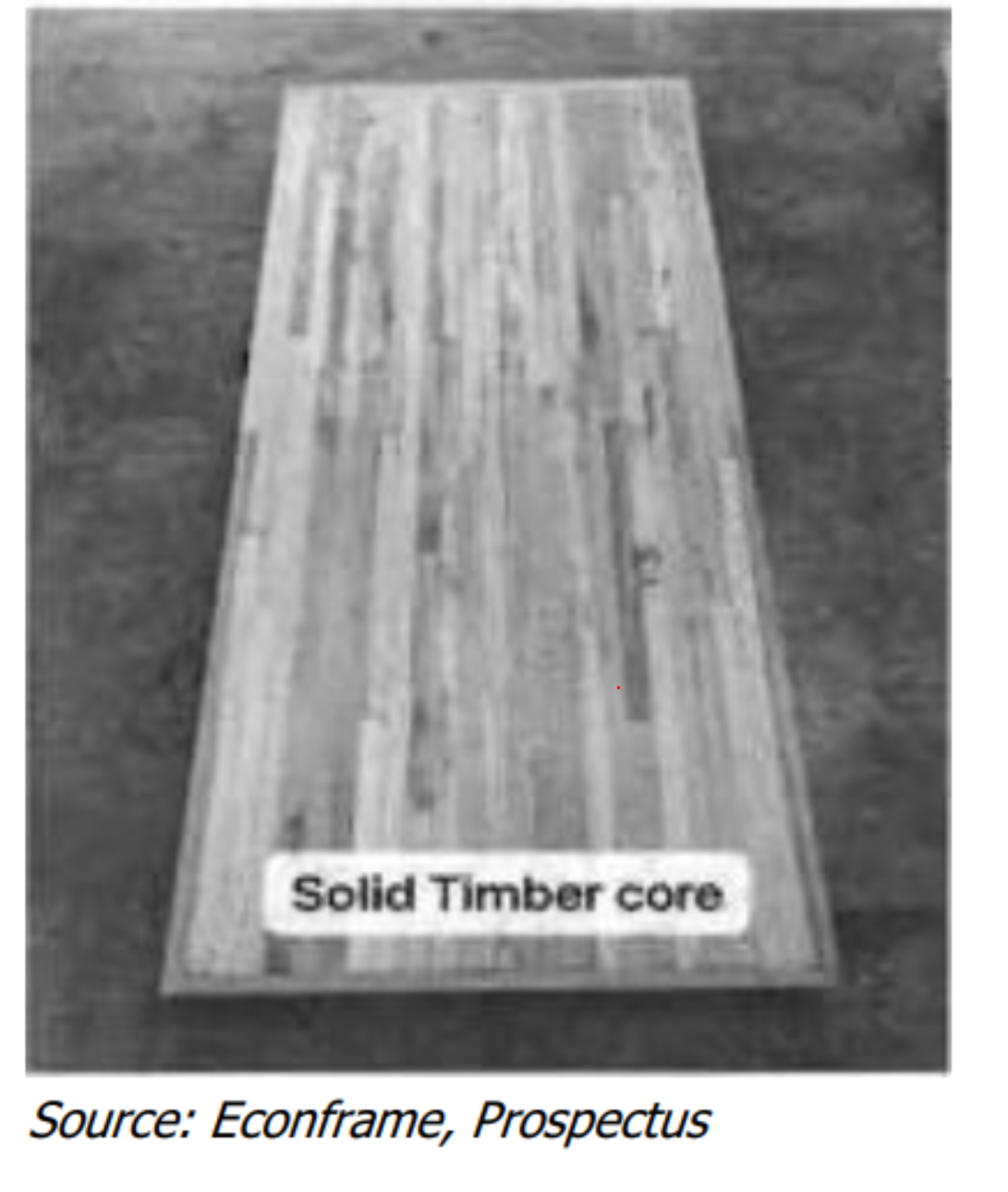

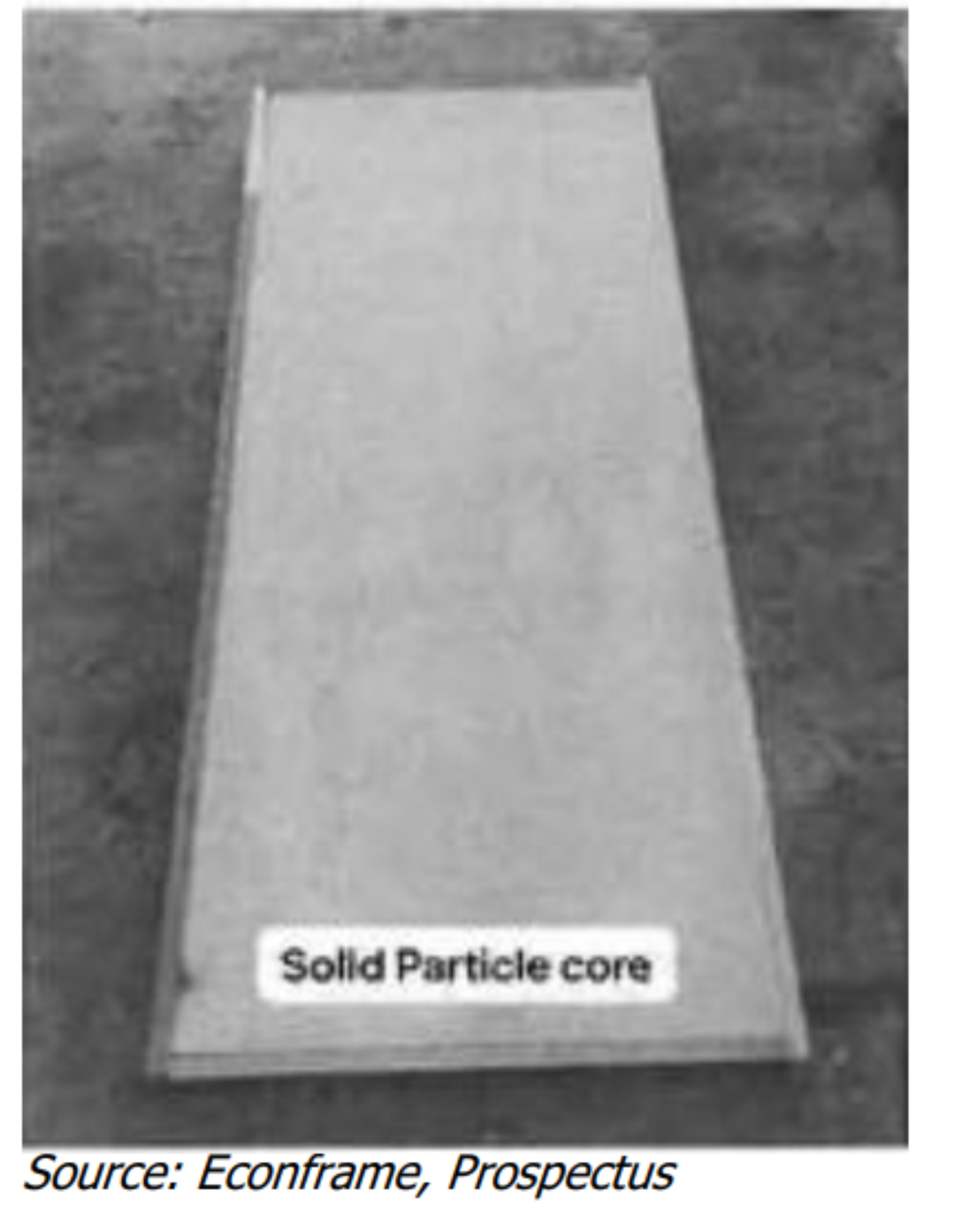

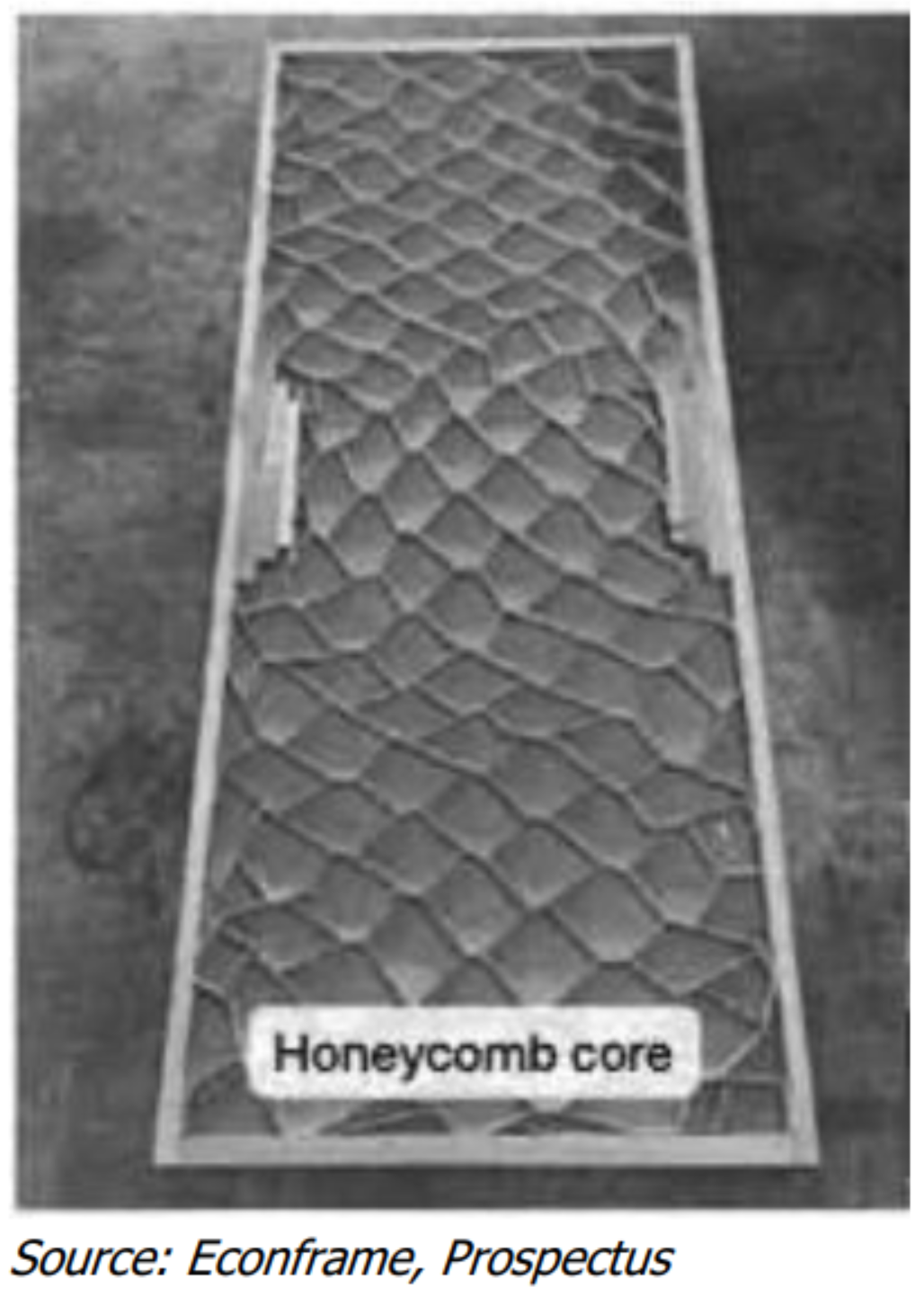

Besides, the group also offers customisable wooden doors with diverse designs, core options, and door skin materials under the ECONFRAME® brand. Manufactured by outsourcing to suppliers, selection of door type and material depends on desired protection, architectural compatibility, and cost considerations. The doors feature a hardwood frame filled with three core construction types namely (i) solid timber core, (ii) solid particle core, and (iii) honeycomb core which each serving distinct functionalities and applications.

Solid Timber core

Solid Particle core

Honeycomb core

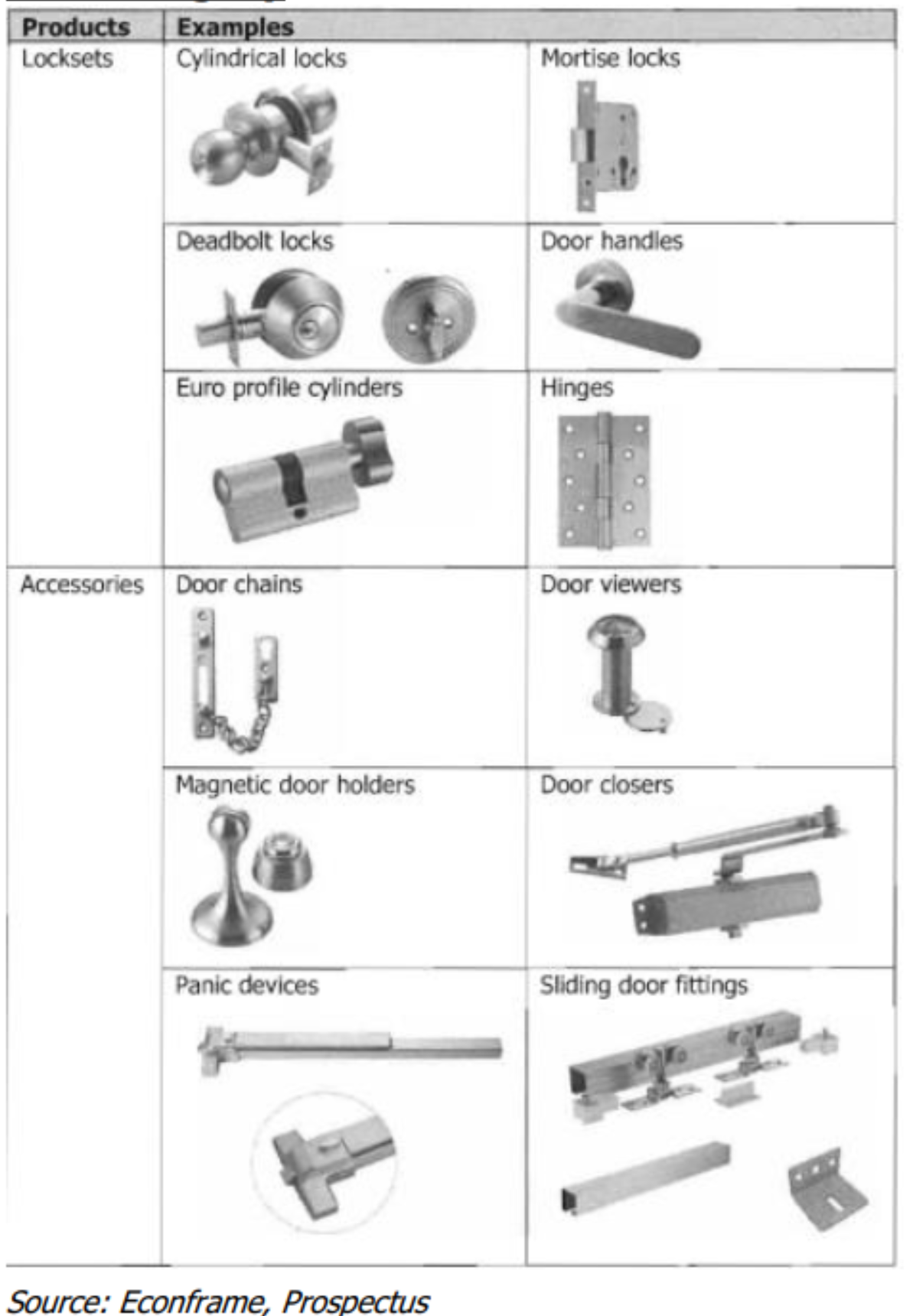

The group provides an extensive selection of ironmongery, consisting of door system components crafted from steel, stainless steel, brass, or aluminum, including locksets and door accessories.

Ironmongery

Industry Overview

Given the group’s revenue relies heavily on real estate developers, business and financial performance are closely tied to the Malaysia real estate market. The Malaysia real estate market is estimated to be USD36.76bn in 2024, projected to reach USD50.69bn by 2029, growing at a CAGR of 6.64% during 2024-2029. Looking ahead, developers remain cautiously optimistic over the medium to longterm prospects, anticipating robust demand from the young demographic.

After a decade of surging house prices, Malaysia's housing market has cooled over the past two years due to substantial oversupply, resulting in RM18.48bn (USD4.41bn) worth of unsold high-rise units in major cities. In bid to combat overbuilding, the government implemented measures, including higher stamp duty from 3% to 4% on properties above RM1.0m (USD238,578) and an additional 5.0% real property gains tax (RPGT) on sales of properties owned for six years or more. These measures were temporarily relaxed in response to the Covid-19 pandemic's

impact on the property market.

Presently, growth of Malaysia's construction sector has created opportunities for increased demand for window and door frames. The industry is anticipated to experience a boost in the foreseeable future, propelled by growing investments in residential, commercial, and industrial projects, both from the government and private sectors. Looking ahead, we reckon that Econframe will remain active merger & acquisition activities in related to core business as one of the avenues to expand business operations.

We gathered that the Malaysia window and door frames market is expected to grow at a CAGR of 8.9% during the forecast period (2020–2025). Expansion of Malaysia's construction industry has created an opportunity for an increased demand for window and door frames. The market is set to benefit from the growing consumer preference for green buildings and energy-efficient solutions, including advanced features in smart windows. Additionally, strong economic growth in major ASEAN countries such as Indonesia and Singapore are poised to contribute to the market's

growth over the next five years.

Investment Highlights

Superior margins supported by premium and reputable brand name. With a reputable brand name known for premium-quality products and the ability to customise based on customer requirements, Econframe serves notable property developers such as Ecoworld, LBS, Gamuda, Sime Darby, and among others. Commanding approximately 60.0% market share in metal door frames in recent times is a testament of their proven credentials. The premium quality and expertise in customisation enhance Econframe's industry reputation and provide superior margins. Econframe enjoyed double-digit PAT margins in past financial years, thanks to the reliability of its in-house brand name and customisation expertise.

Horizontal expansion provide synergy. Econframe completed the acquisition of Lee & Yong Aluminium Sdn Bhd (LYAS) which specialise in fabrication and installation of facade aluminium glazing and glass products in September 2023. The acquisition offers synergies to Econframe's operations which allows the group to expand geographical reach, particularly in the east and south regions. Additionally, the group can cross-sell products to customers, enabling higher sales from secured projects which adds value to sales. The acquisition also came with a profit guarantee contribution of at least RM2.6m (based on Econframe’s stake) for three years. We view the acquisition as one of the key catalysts that will contribute to future earnings growth.

Stepping foot into industrial properties. Additionally, Econframe is venturing into the design and construction of industrial properties by acquiring a 70.0% stake in ETA World (ETAW). Leveraging onto ETAW's expertise, the group aims to capitalise on the promising prospects of the industrial properties market. The increasing foreign investments and growing awareness of sustainability, including ESG considerations, are driving demand for industrial properties. With the completion of the acquisition, earnings growth will emanate from a solid order book of RM165.6m which comes with a profit guarantee of RM7.0m annually for three years.

Benefitting from the resilient outlook on property sector. According to data from the National Property Information Centre (NAPIC), we gather that property transaction volume demonstrated improvement alongside with reduction in overhang units. Signs of recovery in the property market, combined with the government's ongoing efforts to boost homeownership, stabilisation of OPR rate, and positive developments in major infrastructure projects, may potentially lead up increase supply from property developments. The aforementioned projected trend is beneficial for Econframe, which serves property developers and stands to gain from increased construction activity in the property sector.

Lean balance sheet with strong earnings growth. The lean balance sheet of the equipped with substantial cash holdings (RM31.7m) and passable low debt (RM 0.4m) allows the group to undertaken necessary fundings for future expansions, when necessary. We reckon that the group will remain active, both organically and through acquisitions, leveraging the resilient outlook of the property sector and resilient balance sheet.

Financial Highlights

In FY23, Econframe's revenue and core net profit surged to RM75.9m (+27.8% yoy) and RM13.1m (+16.2% yoy), respectively. This marks the group’s annual best financial performance in comparative to the previous corresponding financial years (FY21 and FY22), primarily attributed to robust sales in manufacturing segment.

Moving forward, we forecast core net profit to register at RM19.6m and RM24.6m for FY24F and FY25F respectively. The said growth will be anchored by the contributions from the aggressive merger and acquisition completed by the group together with stronger sales.

Meanwhile, we note that the group has maintained a negligible gearing level over the years, and we anticipate this trend to continue in the coming years. Also, we do not expect any dividends in place, given that the group will remain focus onto preserving cash for future expansions purposes.

Valuation & Recommendation

We favour Econframe for to its established brand name and strong market share in its product offerings. Additionally, the strategic expansion efforts will create synergistic value are noteworthy mention. We also like the group’s historical strong

earnings growth, superior profit margin, and healthy balance sheet.

Our target price at RM1.21 is derived by pegging P/E multiple of 22.0x to FY24F EPS of 5.45 sen. The assigned P/E was based on the stock’s 3-year mean of PER.

The assigned PER is deemed fair in consideration Econframe’s pole position in the metal door frames which commands approximately 60.0% market share and of strong prospects in earnings growth for coming 2 financial years with superior double-digit margin.

Investment Risk

- Slower-than-expected economic growth and demand of property resulting pull back on the supply of the developers.

- Failure to deliver anticipated profit guaranteed from the recent acquisitions’

- activities.

- Fluctuation in raw material prices may impact margins.

Source: Apex Securities Research - 29 Jan 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on JF Apex Research Highlights

Padini Holdings Berhad - Ending the Year With a Solid Performance

Created by kltrader | Aug 28, 2023

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2025-01-21 09:20:00

ADX

10 Mins

SELL

2025-01-21 09:20:00

ADX

5 Mins

SELL

2025-01-21 09:00:00

ADX

30 Mins

BUY

2025-01-21 09:00:00

ADX

10 Mins

BUY

2025-01-21 09:00:00

ADX

5 Mins

BUY

Apps

Top Articles

1

Mercury Securities Research

2

HLBank Research Highlights

3

RHB Investment Research Reports

Market Strategy - Data Centre-Artificial Intelligence Party Pooper

4

RHB Investment Research Reports

5

PublicInvest Research

6

HLBank Research Highlights

7

Mercury Securities Research

8

Kenanga Research & Investment

Renewable Energy - Big News, Another 2GW LSS Incoming (OVERWEIGHT)

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....