Kenanga Research & Investment

Daily technical highlights – (MGB, KPOWER)

MGB Berhad (Trading Buy)

- MGB - a 59.8%-owned subsidiary of listed LBS Bina - is in the business of supplying construction materials in the affordable housing segment. Its share price has seen a downtrend since early-March 2019 possibly dragged by higher start-up costs from its first Industrialised Building System Plant (to produce IBS components from precast concrete panels, concrete wall panels, concrete slabs to column and beam) in 1QFY19, which has resulted in a decline in its FY19 net profit to RM13.4m (-42.2%,YoY).

- However, given the group’s recent contract win worth up to RM215m (thus bringing YTD orderbook to RM1.57b) with possibly more contract wins in the future on the back of rising demand for affordable housing, we thus believe the group’s forward earnings could improve as MGB ramps up its plant utilisation to derive economies of scale.

- Ichimoku-wise, the stock appears to be staging a “Kumo breakout” backed by an above average trading volume. With that, we have plotted our resistance levels at RM0.540 (+15% potential upside) and RM0.600 (+28% potential upside).

- Meanwhile, our stop loss is set at RM0.41 (-13% downside risk).

- Fundamentally speaking, the group has posted a net profit of RM2.4m (-27% QoQ) in 1QFY20. The stock is trading at a low 1-year forward price-to-book valuation of 0.6x, which is at 2SD below mean or 40% discount compared to its average peers valuation of 1.4x.

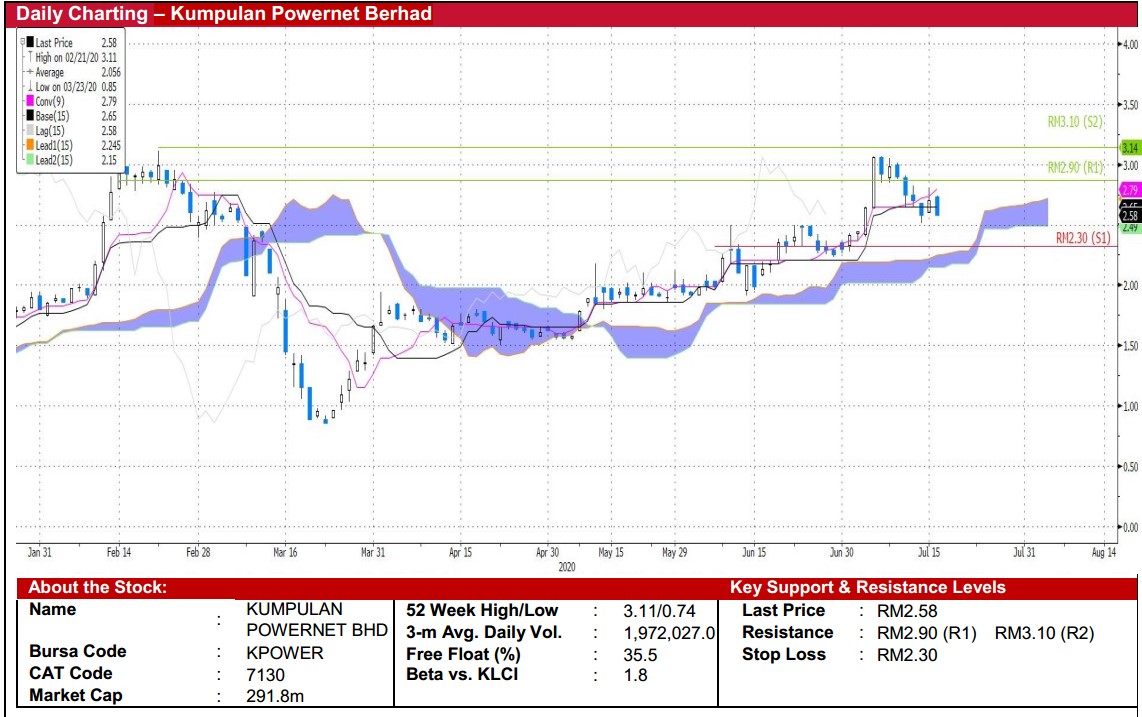

Kumpulan Powernet (Trading Buy)

- Post a reverse takeover exercise by a new management team comprising: (i) SERBADK founder, Mohd Abdul Karim Abdullah, and (ii) Grand Deal Vision SB in June 2019, the Group’s business activity has since been re-positioned to focus on renewable energy segment which is gaining traction amid the rising awareness of ESG (Environmental, Social and Governance) investing.

- The group has also completed a private placement exercise of up to 29.3m shares (representing 35% of the company share base) as of 30th June 2020 to raise proceeds of RM55.4m, which has enhanced the group balance sheet to tender for more projects ahead.

- Also, following its recent tender-book win of RM174m on 26th June to undertake the supply, construction and completion of the civil works in relation to the development of hydropower facilities in Laos, the group’s current orderbook value has risen to >RM1b.

- Technical-wise, the Ichimoku cloud is displaying an upward bias. Should the upward momentum persist, our overhead resistance levels are seen at RM2.90 (+12% potential upside) and RM3.10 (+20% potential upside).

- Our stop loss level is pegged at RM2.30 (or 11% downside risk).

- From a fundamental perspective, KPOWER has recorded earning of RM2.7m (+42%, QoQ) in 3QFY20, bringing its 9MFY20 profit to RM5.5m. KPOWER is currently trading at a forward PER of 25x (slightly below its 1-year forward mean)

Source: Kenanga Research - 17 Jul 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

save malaysia!

3

Follow Kim's Stockwatch!

4

save malaysia!

5

6

Good Articles to Share

The 'Fast Money' traders share the stocks they are thankful for this holiday season

7

save malaysia!

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....