Kenanga Research & Investment

Daily technical highlights – (KAWAN, PWROOT)

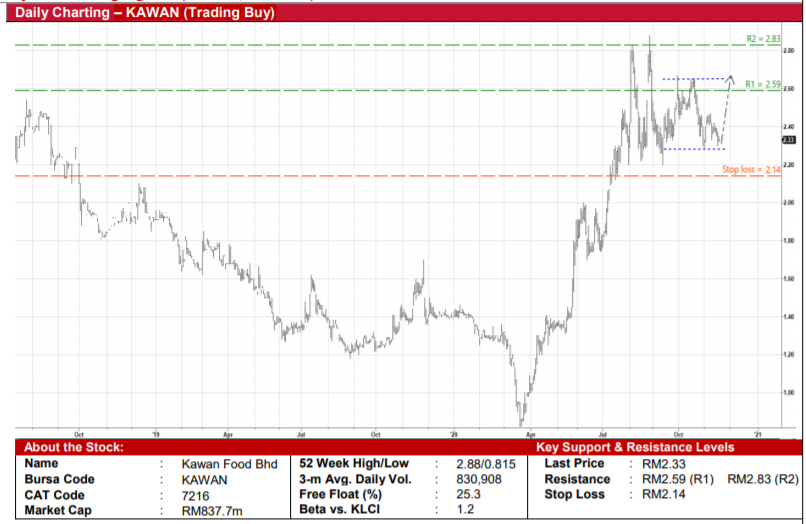

Kawan Food Bhd (Trading Buy)

• The prevailing share price weakness – which saw the stock slipping towards the lower end of a trading band – presents a buying-on-weakness opportunity for KAWAN, a manufacturer and an exporter of frozen food products (covering 36 countries) that stands to benefit from the shift in consumer preference to eat more at home following the Covid-19 outbreak.

• On the chart, after sliding from a high of RM2.65 a month ago to close at RM2.33 yesterday, KAWAN shares could stage a technical rebound soon.

• That being the case, the stock will likely climb to test our initial resistance threshold of RM2.59 before challenging the next resistance level of RM2.83. This represents upside potentials of 11% and 21%, respectively.

• Our stop loss price is set at RM2.14 (or 8% downside risk).

• Fundamentally speaking, the Group is set to beat its FY19’s earnings performance of RM12.0m after announcing net profit of RM15.5m (+258% YoY) in the first six months of 2020.

• An added positive is the Group’s sound financial position with net cash holdings and quoted investments of RM53.7m (or 14.9 sen per share) as of end-June this year.

• Based on consensus earnings forecasts of RM36m in FY20 and RM45m in FY21, KAWAN is currently trading at forward PERs of 23x this year and 19x next year, respectively.

Power Root Bhd (Trading Buy)

• As a manufacturer and distributor of beverages specialising in staple drinks (such as coffee, tea, chocolate malt drinks and herbal energy drinks), PWROOT faces relatively inelastic demand for its products amid the Covid-19 pandemic.

• Reflecting this scenario, during the April – June quarter (when there was an extensive national lockdown), the Group showed resilience by posting net profit of RM10.7m (-12% YoY) on the back of sales of RM83.9m (-11%) in its 1QFY21 results.

• Prior to the Covid-19 business disruptions, PWROOT saw its bottomline rising YoY in the most recent three financial years, up from RM9.7m in FY March 2018 to RM51.7m in FY March 2020.

• Going forward, consensus is projecting net profits of RM49m in FY21 and RM58m in FY22, which translate to forward PERs of 19x and 16x, respectively.

• In addition, the Group’s balance sheet is strong with net cash backing of RM87.9m (or 20.9 sen per share) as of end-June this year.

• The strong fundamentals could set the stage for PWROOT to reward its shareholders with consensus DPS expectations of 11.5 sen for FY21 and 13.3 sen for FY22, implying dividend yields of 5.1%-5.9%, respectively.

• From a technical perspective, the stock is currently riding on a bullish momentum as indicated by the DMI+’s crossover of the DMI-. The positive bias stance is also backed by the share price cutting above its 150-day SMA line recently.

• Therefore, PWROOT shares could continue the upward trajectory by rising towards our resistance thresholds of RM2.44 (R1; 9% upside potential) and RM2.69 (R2; 20% upside potential).

• We have placed our stop loss level at RM2.03 (or 9% downside risk from its last traded price of RM2.24).

Source: Kenanga Research - 19 Nov 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

4

Good Articles to Share

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....