Kenanga Research & Investment

Daily technical highlights – (MIECO, AEMULUS)

Mieco Chipboard Bhd (Trading Buy)

• Furniture companies in Malaysia have benefited from the prolonged work-from-home situation globally as seen in the better earnings of LIIHEN, SPRING, HOMERIZ and POHUAT. Likewise, we believe MIECO stands to benefit from the aforementioned trend as well, given the group’s involvement in the manufacturing and distribution of particle boards, which are mainly supplied to the domestic market. These chipboards are commonly used as a core material for home and office furniture.

• QoQ, the group’s revenue increased to RM113.5m (+78% QoQ) in 3QFY20, given the resumption of business following the previous quarter’s Covid-19-related disruptions. Meanwhile, its bottom-line turned from a net loss of RM12.2m in 2QFY20 to a net profit of RM8.1m in 3QFY20, mainly due to: (i) better selling volumes, and (ii) higher average selling prices given the pent-up demand in the furniture segment.

• Chart-wise, the stock has formed a healthy uptrend after starting a rally in mid-August this year. Given the shorter-term key SMA still treading above the longer-term key SMA and an uptick in RSI indicator, we thus believe the upward journey remains intact.

• With that, our overhead resistance levels are positioned at RM0.870 (R1; +10% upside potential) and RM0.975 (R2; +23% upside potential).

• Our stop loss level is pegged at RM0.735 (-7% downside risk).

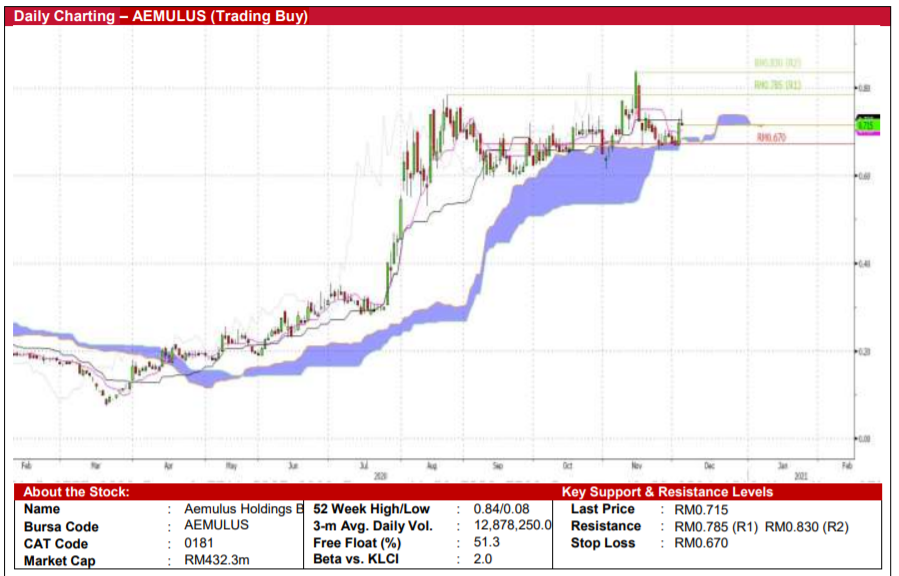

Aemulus Holdings Bhd (Trading Buy)

• AEMULUS is a company that is involved in the production of electronic stress tester machines.

• Given that China’s semiconductor supply chain has been disrupted by trade pressures imposed by the U.S. government, the Chinese government has set up “Big Fund Phase II” to reduce its reliance on the U.S. semiconductor supply chain. This, in turn, will ultimately increase capital expenditure in the sector in China.

• With that, we believe AEMULUS would benefit from the aforementioned development, as its JV agreement with Tangren Microintelligence (a China-based company) would help the group to broaden its reach in the China market.

• The stock has retraced from its all-time high of RM0.84 on 13th November 2020 and continued to find support on the “Bullish Kumo Clouds”. Ichimoku-wise, we believe the stock will continue to trend higher as its Bullish Kumo Clouds is still on the rise.

• Should the buying interest resume, our next resistance levels are set at RM0.785 (R1; +10% upside potential) and RM0.830 (R2; +16% upside potential).

• Meanwhile, our stop loss level is pegged at RM0.670 (-6% downside risk).

• Fundamentally, the group is projected to turn from a net loss position to a net profit of RM8.1m in FY21E and RM14.4m (+77% YoY) in FY22E based on consensus numbers. This translates to forward PERs of 53x and 30x, respectively.

Source: Kenanga Research - 4 Dec 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 1 of 1 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

2

3

4

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

5

Good Articles to Share

6

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

7

Good Articles to Share

8

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

moneykj

Go for Digistar

2020-12-04 08:56