Kenanga Research & Investment

Daily technical highlights – (TGUAN, SCGM)

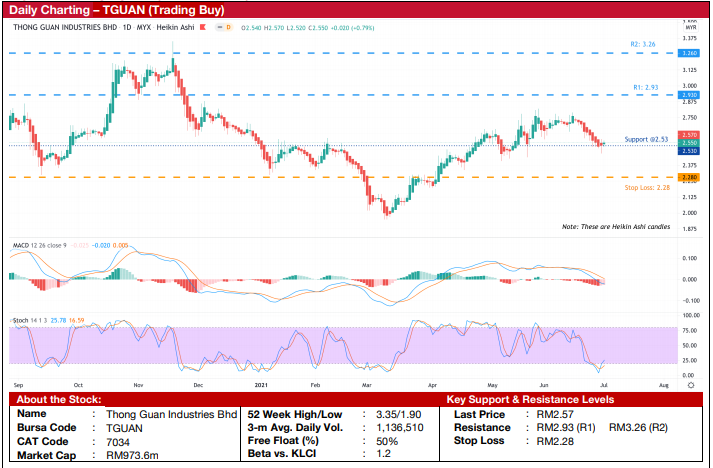

Thong Guan Industries Berhad (Trading Buy)

• TGUAN manufactures stretch films, garbage bags, courier bags and a variety of other plastic packaging. It serves customers around the world and is planning to drive growth in North America and Europe by growing sales volume and acquiring new customers.

• Resin prices have been gradually falling after peaking in March 2021. Despite the drop in the main raw material cost, plastic manufacturers’ selling prices have remained elevated, which would boost profit margins in the coming quarters.

• In FY20, TGUAN achieved a net profit of RM76.3m. Moving forward, our research team is estimating net profit of RM87.4m in FY21 and RM94.8m in FY22, implying 15% and 9% YoY growth, respectively. This translates to forward PERs of 11.1x this year and 10.3x next year, respectively.

• Technically speaking, the stock began to chart an uptrend pattern since March 2021, forming higher lows on its way up. While the stock has pulled back 8% from RM2.78 since mid-June 2021, we reckon it has recently found support at RM2.53.

• The Heikin Ashi candlesticks show that the short-term correction may be coming to an end as the latest two candlesticks indicate that a price reversal is on the horizon. We see the current price weakness as a good buying opportunity.

• With the MACD and stochastic indicators showing signs of upward momentum, we believe the share price could potentially challenge our resistance levels of RM2.93 (R1; 14% upside potential) and RM3.26 (R2; 27% upside potential).

• We have pegged our stop loss at RM2.28 (11% downside risk).

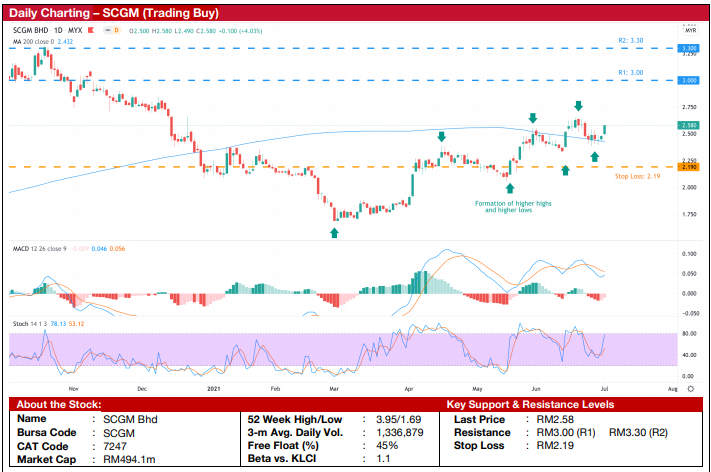

SCGM Berhad (Trading Buy)

• SCGM manufactures food & beverage packaging, namely takeaway trays and plastic containers for fresh foods in supermarkets. In 2020, SCGM has diversified into the manufacturing of face shields and face masks.

• Like other plastic manufacturers, since March 2021, SCGM has benefited from falling resin costs and elevated selling prices, allowing them to expand margins. In addition, SCGM’s high-margin products are also experiencing strong sales, boosting further its margins.

• Since the re-implementation of lockdowns following the resurgence of Covid-19 cases in Malaysia and Singapore in April 2021, SCGM has seen strong orders for its takeaway packaging products and face masks.

• The Group recently announced a core net profit of RM34m for FY ended April 2020. Moving forward, our research team is estimating that SCGM will achieve net profit of RM37.4m in FY21 and RM40.2m in FY22. This translates to forward PERs of 13.2x this year and 12.3x next year, respectively.

• Technically speaking, the stock remains in an upward trend, signalled by: (i) its formation of higher lows and higher highs since March 2021, and (ii) its recent crossing above the 200-day SMA.

• With the MACD and stochastic indicators showing signs of strengthening momentum, we believe the share price could potentially challenge our resistance levels of RM3.00 (R1; 16% upside potential) and RM3.30 (R2; 28% upside potential).

• We have pegged our stop loss at RM2.19 (15% downside risk)

Source: Kenanga Research - 2 Jul 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Bond Weekly Outlook - MGS/GII likely to rise amid ongoing US economic resilience

Created by kiasutrader | Nov 22, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

2

4

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

5

6

7

Good Articles to Share

Iran to hold nuclear talks with three European powers in Geneva on Friday, Kyodo reports

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....