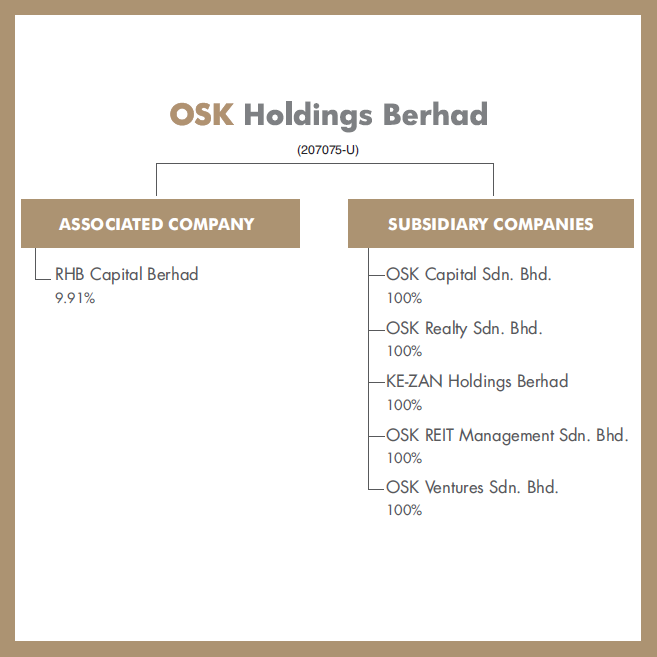

Since selling its core business OSK Investment Bank to RHB Capital in 2012 for RM1.95 billion, OSK Holdings (OSK) does not have a core business.

In return, OSK was paid RM147.5mil cash and 245mil RHB shares at RM7.36 per share. After dividend reinvestment, now OSK holds 9.91% of RHB (252.3mil shares).

Currently OSK involves in property investment and capital financing business which generate little revenue and profit compared to what its investment bank has contributed before. Sooner or later it will inject a new core business into it.

The new business can't be finance-related that compete with RHB within 6 years. However, It is not hard to guess what kind of business OSK will acquire soon.

OSK's controlling major shareholder, CEO & MD Tan Sri Ong Leong Huat (40.5%) is also a major shareholder in other listed companies such as OSK Property (73.8%) and PJDev (21.4%).

Ong LH has hinted that property development will be OSK's new core business back in April 2014. The news will be announced within 6 months from April.

All the discussion written below are just my inexperience and laughable opinion, which might be inaccurate and not true.

Anyway, I think I will learn something from OSK's corporate exercise.

Anyway, I think I will learn something from OSK's corporate exercise.

Will OSK Holdings purchase development land by itself and compete with OSKProp and PJDev in the property market? I don't think so.

So there is straightforward speculation that OSKProp and/or PJDev will be consolidated into OSK Holding.

The question is both or one of them.

If OSK acquires both companies then Ong LH may risk diluting his shareholding in OSK as OSK may need to issue new OSK shares to acquire those companies.

So I think OSK may acquire one of them which should be OSKProp as they have the same name and Ong LH holds 73.8% of it directly & indirectly.

The deal seems to be close as OSK's share price surged in the last 2 trading days while both OSKProp & PJDev's share prices are at new high.

All 3 companies owned by Ong LH above are still trading at a relatively low PE ratio even though their share prices have gained handsomely this year.

All 3 companies owned by Ong LH above are still trading at a relatively low PE ratio even though their share prices have gained handsomely this year.

| OSKProp | PJDev | OSK | |

| Price@27/6/14 (RM) | 1.98 | 1.66 | 1.83 |

| Shares (mil) | 243.7 | 456.1 | 969.1 |

| PATAMI (RM mil) | *55.5 | #97.0 | *195.6 |

| EPS (sen) | 0.228 | 0.213 | 0.202 |

| PER | 8.68 | 7.79 | 9.06 |

| OLH % | 76.52 | 21.40 | 40.54 |

| Equity (mil) | 434.7 | 999.0 | 2628.0 |

| Cash (mil) | 124.5 | 110.6 | 1.9 |

| Loans (mil) | 162.2 | 467 | 240.6 |

| Net D/E | 0.09 | 0.36 | 0.09 |

* PATAMI for FY13

# PATAMI for Last 4 Quaters

Currently PJDev has slightly lower PE ratio compared to OSKProp but PJDev has significantly higher gearing.

Both have warrants which will dilute their future EPS. Once fully converted to mother shares, OSKProp's (Year 2017) EPS will be diluted by 30.7% while PJDev (Year 2020) will be diluted by 31.7%.

If OSK is really going to acquire OSKProp and make it its core business, I guess it should be a good news to shareholders of both companies.

Should speculators & investors buy OSK Holdings, OSK Property or PJDev now?

I have no experience in the rational of such business transaction so my opinion might be wrong.

Firstly, how to value OSKProp as an acquisition or merger target?

If we use book value or net asset per share, OSKProp's latest figure is RM1.81 at end of Mac14. Current share price of RM1.98 is 1.09x higher.

OSKProp has RM938mil of unbilled sales in Mac14 and its future development in Sg Petani alone carries a potential GDV of RM3bil. It has approximately 1,540 acres of land for development, with 1,500 acres in Sg Petani (Annual Report 2013). How many times book value is fair to acquire OSKProp?

OSK Investment Bank was sold to RHB at 1.77x book value about 2 years ago.

Can enterprise value being used here?

EV of OSKProp = 1.98(243.7) + 17.5 + 162.2 - 124.5 = RM537.7 mil or RM2.21 per share. It is still 11.6% below current share price.

| OSKProp | PJDev | |

| EV | 537.7 | 1097.5 |

| EBIT | 86.6 | 146.0 |

| EV/EBITDA | 6.2 | 7.5 |

| EV/share | 2.21 | 2.41 |

OSK will need to pay more about RM1bil to take over PJDev from EV point of view.

OSKProp has slightly lower EV Multiple (EV/EBITDA) compared to PJDev, which means OSKProp is more attractive for a take-over as it takes only 6.2 years to pay off the cost compared to PJDev's 7.5 years.

As OSK is low in cash (only RM1.9mil), it must borrow to fund the acquisition unless it divests its investment in RHB which is unlikely at the moment.

OSK should have no problem to borrow as its investment in RHB is worth RM2.1bil and net debt to equity ratio is merely 0.09x currently.

If it borrows the entire EV of RM537.7mil of OSKProp from financial institution to fund the acquisition, its net gearing will only increase to 0.30x which should be fairly comfortable for a property developer.

This does not include the 101.6 million OSKProp-WC warrants though.

So if it does not issue new OSK shares for the acquisition, then I think it is good news to current OSK shareholders as not only net profit will rise tremendously, there will be no dilution of shareholding.

Nonetheless, I'm not sure how many percent of OSKProp that OSK will acquire should it happen. Will it acquire 100% and delist OSKProp? Ong LH has already owned 73.8% in OSKProp & 76.5% in OSKProp-WC.

Will it issue new OSK shares to existing OSKProp shareholders as part of the deal?

Is it possible that Ong LH who currently enjoys 73.8% profit sharing in OSKProp would want to reduce it to only 40.5% after consolidating into OSK without issuing additional OSK shares to OSKProp shareholders?

Will OSK acquire PJDev instead of OSKProp, or both, or neither of them?

I think it is very likely that the share price of those involved in the deal with increase, unless the deal tabled is unfair or does not meet the expectation of small shareholders.

How is Ong LH's reputation?

Last year Ong LH has attempted 2 take-overs of his companies which failed eventually.

Those offers were not good.

Anyway, I think OSK Holdings might be a good stock to hold in anticipation of new business injection.

* This article is just for sharing. Readers should not take it seriously :)

Last year Ong LH has attempted 2 take-overs of his companies which failed eventually.

- July13 - offered RM1.68 for OSK, share price at that time RM1.65, net asset per share RM2.58.

- Dec13 - offered RM0.58 for OSKVI, share price at that time RM0.52, net asset per share RM1.06.

Those offers were not good.

Anyway, I think OSK Holdings might be a good stock to hold in anticipation of new business injection.

* This article is just for sharing. Readers should not take it seriously :)

skyland

Good company but the owner are too stingy. I will avoid...good luck

2014-06-29 17:46