KIMHIN: Another Fantastic Quarter, Potentially Limit Up

KIMHIN: Another Fantastic Quarter, Potentially Limit Up

It had been a very good last week for my stock investment. Another counter in my 2017 stock pick competition reported excellent result:

http://klse.i3investor.com/servlets/pfs/70717.jsp

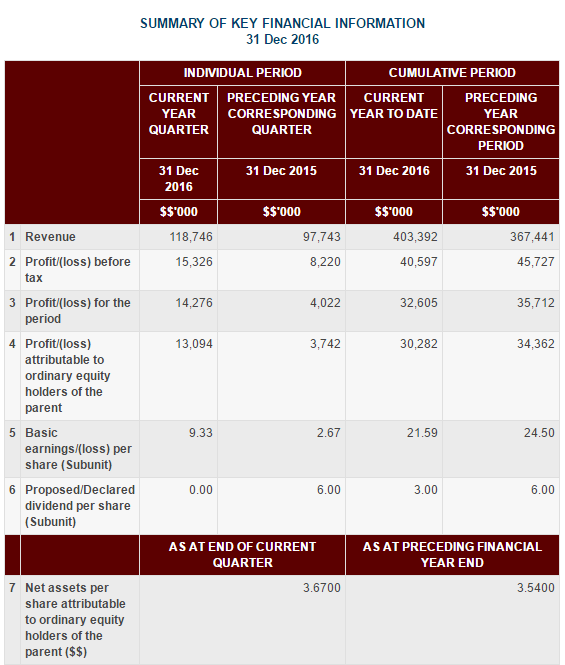

Last Friday, KIMHIN recorded increase revenue and EPS 9.33 this quarter, much higher than corresponding last year quarter of EPS 2.67.

The quarter report reveals revenue up was mainly contributed by better performance in all geographical segment except Malaysia operation and contribution from recently required subsidiary in Australia, Outset Holding Pty Limited in Sept 2016. The same contributions also helped KIMHIN to archieved EPS 9.74 in previous quarter.

I am optimistic KIMHIN can continues to register EPS over 9.0 in subsequent quarters. It could be more as their business operation is growing in Australia and China. If we annualize EPS 9.0 per quarter and apply conservative PE of 9, the fair value would be RM 3.24. Current price is only RM 1.91. Furthermore, its NTA is much higher at 3.67 and dividend yield stands at very good rate of 4.72%.

With relatively small total number of share, KIMHIN potentially get limit up on Monday.

Trade at own risk,

Hopefully, AllWin

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

Featured Posts

Latest Videos

Apps

Top Articles

2

save malaysia!

3

BFM Podcast

4

BFM Podcast

5

BFM Podcast

6

BFM Podcast

7

BFM Podcast

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

JacNgu

dream on. limit up.

2017-02-26 22:24