Mercury Securities Research

Cahya Mata Sarawak (2852) - The Forgotten Child

MercurySec

Publish date: Thu, 25 Jul 2024, 09:14 AM

MercurySec

0 435

An official blog in i3investor to publish research reports provided by Mercury Securities Research team.

All materials published here are prepared by Mercury Securities Sdn. Bhd.

Mercury Securities Sdn. Bhd.

L-7-2, No.2, Jalan Solaris,

Solaris Mont Kiara, 50480, Kuala Lumpur

Tel: 603-6203 7227

Email: mercurykl@mersec.com.my

All materials published here are prepared by Mercury Securities Sdn. Bhd.

Mercury Securities Sdn. Bhd.

L-7-2, No.2, Jalan Solaris,

Solaris Mont Kiara, 50480, Kuala Lumpur

Tel: 603-6203 7227

Email: mercurykl@mersec.com.my

Stock Highlights

Natural monopoly due to market forces. We believe concerns over potential new cement players in Sarawak are overblown. CMS' key cement division has long enjoyed being a natural monopoly in Sarawak due to the high barriers of entry. This is mainly because the overall cement demand in Sarawak is not large enough to support a two-player market, especially now with CMS committing to build a second clinker plant to triple its capacity from 0.9 MT/pa to 2.8 MT/pa eventually (100% self-sufficient). Any new entrants would also be deterred by the geographical challenges in Sarawak (suitable plant location, distribution network, etc.).

Dispute resolution with SESCO a near-term catalyst. The ongoing dispute with Sarawak Energy (SESCO) has had a negative impact on sentiment and earnings for CMS. Since May 2023, SESCO has cut electricity supply to CMS' phosphate plant, leading to no revenue generation but incurring losses from commissioning costs and inventory write-downs. The phosphates division recorded RM19m losses in 1Q24, compared to the RM38m net profit reported by the group. Arbitration proceedings are scheduled to begin hearings next month on 26-29 August.

Deeply undervalued. Based on consensus forecast, CMS is currently trading at an undemanding valuation of 7.6x FY24 P/E (ex-net cash of RM527m) and 0.45x FY24 P/B. Its valuation has been heavily discounted largely due to perceived political risks, which we believe were partly misunderstood especially for its key cement division. In our view, a favourable dispute resolution with SESCO will drive further earnings upside, while a potential increase in stake held by the Sarawak state government (who currently owns 5.7% via SEDC) could help to significantly narrow the “political risks” discount.

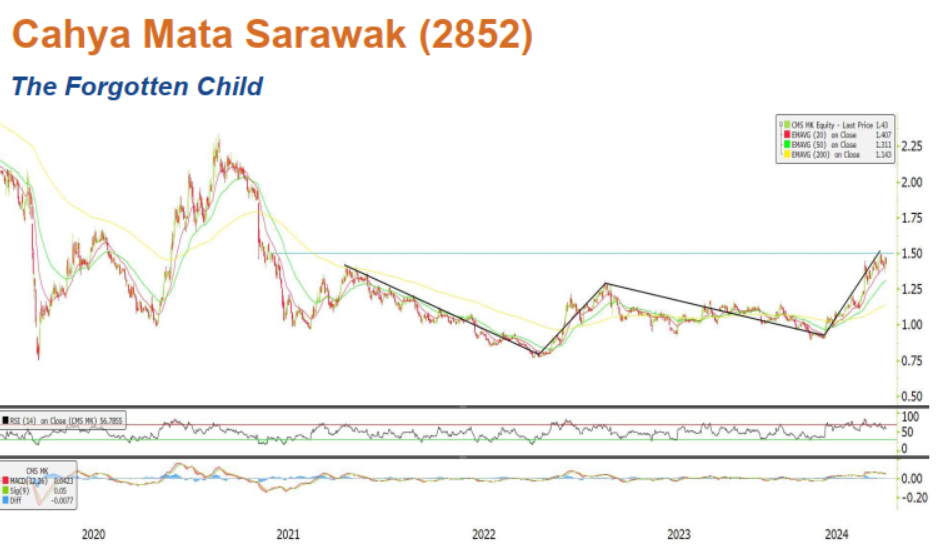

Testing RM1.50 resistance. CMS has performed strongly since April, rising from a low of RM0.91 to a high of RM1.50. The stock formed a significant W pattern starting since November 2021, indicating an upcoming potential breakout. Consolidation activities have also been seen within the range of RM1.36-1.50 recently. A break above the resistance level of RM1.50 could drive the stock to the next resistance level at RM1.78. Stop loss at RM1.32.

Source: Mercury Research - 25 Jul 2024

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Mercury Securities Research

Discussions

Be the first to like this. Showing 1 of 1 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-12-20 16:30:00

EMA 5

5 Mins

SELL

2024-12-20 16:15:00

EMA 5

5 Mins

BUY

2024-12-20 15:35:00

EMA 5

5 Mins

SELL

2024-12-20 14:50:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-12-20 14:30:00

TURTLE SYSTEM 20

5 Mins

BUY

Apps

Top Articles

1

Rakuten Trade Research Reports

2

Stock Market Enthusiast

Top 3 AI/Data Center Newsflow for the 3rd Week of December - #TENAGA, #YTL, #YTLPOWER

3

Stock Market Enthusiast

4

save malaysia!

5

Mercury Securities Research

6

7

8

Good Articles to Share

S&P 500, Nasdaq dip as rate cut fears linger despite easing inflation

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Yaw Yang Lee

Now you say undervalue????sudah siap collect???

2024-07-25 19:41