SEE_Research

The Trilogy of FAST & FURIOUS Shows, PART 2 - DAYANG / 5141 @ KLSE

SEE_Research

Publish date: Sun, 29 Dec 2019, 01:35 PM

Just like the movies, the famed Fast & Furious is ALL ABOUT SPEED.

Get ready for Part 2 of this Trilogy series!

Part 1: POS / 4634

Part 2: DAYANG / 5141 (NOW SHOWING)

Stock for 2020

Summary - Review

For 2019 - this stock has performed very well in terms of price uptrend

from low RM0.515 (3 Jan 2019)

recent high RM2.49 (13 Dec 2019)

new high RM2.54 (23 Dec 2019)

------------------------------------------------------------------------------------

To illustrate the mighty potential of this stock, DAYANG:

From Junior Commissioned Officer > Second Lieutenant

in the progression > Lieutenant

and next year 2020 will be promoted to Captain and subsequently courageous Lieutenant Colonel of the famed Gurkha Riffle

that is world-famous for extreme bravery.

This famed Captain always carry with him a special weapon called Khukuri.

In this case, DAYANG / 5141 possesses the special Khukuri - its subsidiary PERDANA PETROLEUM BERHAD / 7108.

This PERDANA PETROLEUM group owns and operates 17 offshore support vessels (OSVs).

Compared to other DAYANG competitors, they have to outsource their offshore support vessels to other companies as they do not own such facilities.

Special weapon Khukuri. Image Credit: GETTY

A weapon so special, it has the ability to enhance its user to take down up to 40 robbers and even save a girl's life!

One thing's for sure, you don't want to be the enemy when the Khukuris are out of their sheaths!

------------------------------------------------------------------------------------

Part of the story DAYANG is the Durian and the scent of money

Durian, the thorny king of fruits, is beginning to earn big bucks for the country, with last year’s production value topping RM5bil.

No wonder more people are venturing into the durian business.

Demand from China since the middle of last year has driven both smallholders and large companies to take a second look at expanding or acquiring more land bank to cultivate this fruit. New players are also emerging.

There are over 200 varieties of this fruit, more than what Thailand has. Apart from the famous and pricey Musang King, the other favourites are IOI, D24, Black Thorn, and Red Prawn.

In China, the Musang King frozen fruit is said to be sold at a price of at least RM300 a kg.

For now, only 1% of the population in China has tasted this fruit, indicating a huge potential.

The farm price of Grade A Musang King durian has gone up from RM9 per kg to RM33 per kg last year.

Apart from demand from China, processed durian is gaining popularity in products such as durian pulp, paste, ice cream, chocolates, cakes and snacks. In China, durian is being used to flavour cookies, coffee, crepes and pizza.

------------------------------------------------------------------------------------

Summary of KLSE

A) Main Board Summary, as per 21 Dec 2019.

There are 16 sectors comprising of 785 active companies

PN17 22

Subtotal 807 active companies

B) ACE Market

There are 10 sectors comprising of 129 active companies

C) LEAP Market 28 active companies

GRAND TOTAL (A+B+C) 964 active companies

For now, KLSE investors only come to know on

DAYANG - which is less than 1% of the total investment.

What is going to happen?

When the investing proportion increases from less than 1% to 5% in the year of 2020,

Excerpt from Mr Koon Yew Yin's blog 25 Nov 2019, 2.41pm -

Mr Ooi Teik Bee has sent out his circular with a target price of Rm 3.00.

...

MIDF’s target price is Rm 2.69.

...

Dayang’s 1 quarter EPS -0.41 sen, 2nd quarter 5.71 sen and 3rd 11.1 sen. Assuming its 4th quarter EPS is the same as its 3rd quarter 11.1 sen, its annual EPS will be 27.5 sen. Just based on P/E 10, Dayanag’s price should be Rm 2.75.

...

Dayang’s long term growth prospect

As long there is oil, Petronas will continue to pump oil for sale. Even if the oil price dropped drastically, Petronas will still continue to pump because all the cost of the oil rigs has been paid and accounted for. Dayang being the largest oil rig maintenance contractor will have more contracts. Dayang should have very good profit growth prospect which is the most powerful catalyst to push the share price higher and higher.

In the last few months, I have been searching for any stock to diversify in vain. I cannot find another stock with similar quality as Dayang.

------------------------------------------------------------------------------------

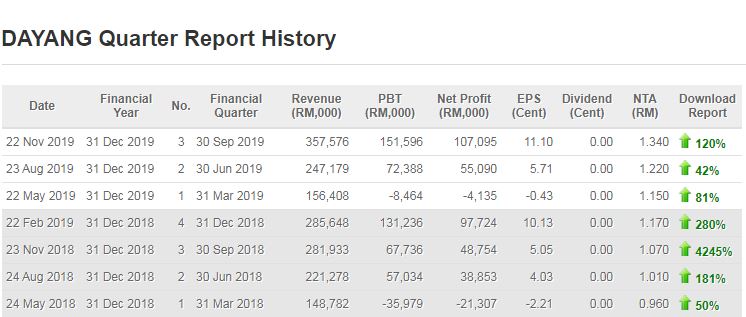

22 Nov 2019 EPS (Cent) 11.10

23 Aug 2019 EPS (Cent) 5.71

22 May 2019 EPS (Cent) -0.43

22 Feb 2019 EPS (Cent) 10.13

-------------------------------------------

TOTAL 26.51 x PER 13.22 = RM3.504622

The intrinsic value should be RM3.504622

13.22 - Lowest P/E value, Source Malaysia P/E

It would not be surprising for first quarter of 2020 DAYANG,

can revisit its glorious high of RM3.66 created on 7 March 2014 or even surpass it.

Stay tuned for Part 3 of this exciting trilogy series!

Part 3 - Coming Soon in 2020.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on SEE_Research

THE FAST & FURIOUS MODE ON Super duper momentum stock for June 2024 / KGB / Kelington Group Berhad

Created by SEE_Research | Jun 08, 2024

THE FAST & FURIOUS MODE ON

Super duper momentum stock for

June 2024 /

KGB / Kelington Group Berhad

The Trilogy of Fast and Furious Mode/ Part 7 / SUPERIOR BUL_ S CR _ PS by call vin ta boh liau _

Created by SEE_Research | Feb 26, 2023

Featured Posts

Latest Videos

.png)

Apps

Top Articles

1

Mercury Securities Research

2

The Alpha Trader

4

5

save malaysia!

6

7

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

slts

talk cok, life is not tat easy

last yr eps to be repeated.

why not talk bigger cok,

estimate next yr eps to be 0.26 x 2= 0.52

2019-12-29 15:01