A huge surprise! KGB clinched its largest job win worth RM420m, doubling its existing order-book which was already at all-time high levels before this. The job entails a turnkey construction of a new semiconductor fab in Kuching for a US listed memory company which will begin immediately as the US client is scrambling for capacity to keep up with the surge in memory chip demand. This brings YTD order wins to a new high of RM764m while order-book hits a record RM822m, nearing its current market cap. KGB remains our top hidden gem pick owing to its healthy job pipeline and secular growth story. Maintain OUTPERFORM with a higher TP of RM2.50.

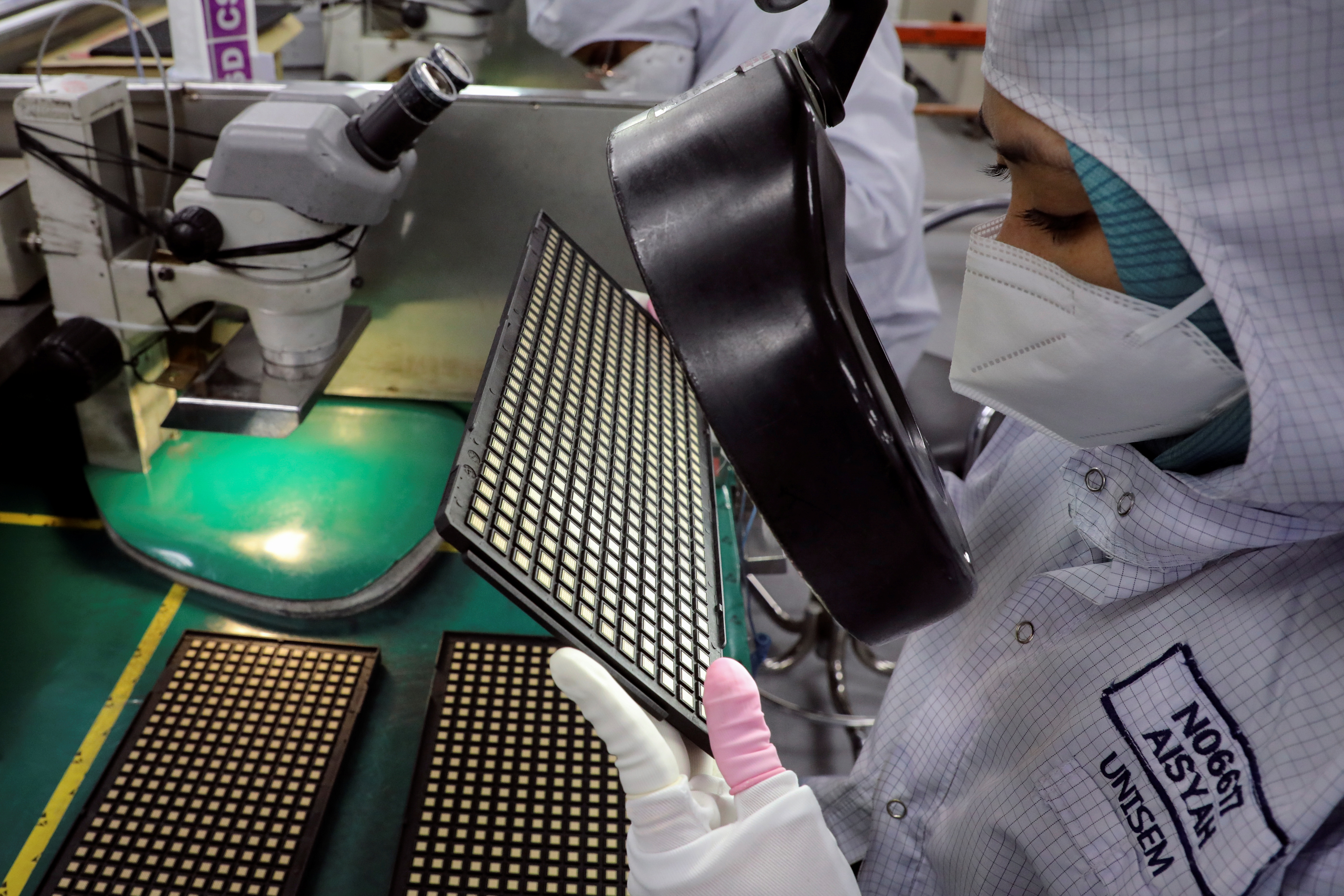

Largest job win; 4x its typical contract size. Kelington Group (KGB) surprised us with its single largest job award ever worth RM420m (4x the size of typical contracts) from a US listed semiconductor manufacturing company at Sama Jaya Free Industrial Zone in Kuching to undertake a turnkey construction for an entire new semiconductor fab, focusing on memory chip. KGB is tasked with handling the whole project, involving all three of its business segments (UHP, Precision Engineering and General Contracting). The job will begin immediately and is slated to be completed by end-2022 as the US customer is urgently in need of new capacity to accommodate the surging demand for its memory and data storage products. This is in line with our observation on the tech space that chip shortage will remain in the foreseeable future as the surge in semiconductor demand continues to outpace capacity expansion.

Orderbook nears current market cap. Inclusive of this recent win, KGB has secured a record-breaking RM764m (vs. FY19 of RM490m) new job wins in 2021, exceeding our expectation of RM500m. Meanwhile, its outstanding order-book has ballooned to another all-time high of RM822m, which is more than double of FY20 revenue. Interestingly, its order-book has grown very close to its current market capitalisation.

Sufficient resources to take on more jobs. The recent completion of one of its large projects in Penang couldn’t have been timelier as this frees up resources for the group to take on the new turnkey job in Kuching. Note that the relationship of higher revenue recognition and overhead expense is nonlinear, which means KGB is able to enjoy economies of scale and better margin as we anticipate the group to achieve back-to-back record revenue and earnings for FY21 and FY22.

Still, more to come. Reiterating our positive view, we expect more fab expansion to come and KGB is in a favourable position to benefit from more UHP jobs, with the management showing no signs of slowing down in terms of securing new jobs. The group’s tender-book remains elevated at RM1.1b.

Raise FY21E-22E earnings by 4% and 33% to RM32.3m and RM47.0m, representing growth of 85% and 46%, respectively.

Maintain OUTPERFORM with a

higher Target Price of

RM2.50 (previously RM1.50)

on FY22E PER of 33x (+1SD to 3-year peer mean), justified by the group’s healthy job pipeline and secular growth story.

Risks to our call include: (i) slower revenue recognition due to Covid-19, (ii) downturn in semiconductor sales, and (iii) delay in liquid CO2 ramp up.

Source: Kenanga Research - 15 Sept 2021

=========================================================================

Please note : the number of huge

quantities of shares

the main directors are buying in

KGB WB , with official disclosures .

=======================================================================

=======================================================================

BREAKING NEWS

BREAKING NEWS

BREAKING NEWS

Technology - Riding on the Chip Crunch

|

Date: 01/10/2021

|

Source |

: |

KENANGA

|

|

Stock |

: |

KGB |

|

Price Target |

: |

2.50 |

| |

Price Call |

: |

BUY |

|

|

|

|

|

Last Price |

: |

1.73 |

| |

Upside/Downside |

: |

+0.77 (44.51%) +0.77 (44.51%) |

In line with global move towards 5G adoption, Malaysia is also switching off its 3G connectivity to free up the 2100Mhz and 900Mhz for redeployment towards 4G and 5G. With demand for consumer electronics and automotive (especially EVs) showing no signs of slowing, wafer fabs in Asia continue to see the need to expand their capacity, further reinforcing our investment thesis on Kelington Group (OP; TP RM 2.50 ), as a prime beneficiary.

TSMC and other wafer fab players had in recent earnings call stated that they are planning to build more capacity for the automotive industry which typically takes 12-18 months, this explains why automotive semiconductor players (e.g. Infineon, ST Micro and Renesas) are already locking in orders 1-2 years in advance.

Such development continues to favour our

hidden gem pick, KGB / 0151

Kelington Group (OP; TP: RM2.50),

as a prime candidate to benefit from fab expansions in Asia. Even with share price surging more than 3.2x (inclusive of free warrants) since our non-consensus initiation report on 11 Nov 2020, it still remains as our

***high conviction buy ***

as the group is expecting more ultra-high purity gas system (UHP) job awards from fabs in China and Singapore.

![How? Invest in Stocks Malaysia [works GREAT from 2021]](https://www.howtofinancemoney.com/wp-content/uploads/2018/04/Stocks-investing-niching-down-micro-sector.gif)

.png)