SUPER BULLISH STOCKS

Super Positive Momentum Stocks

FOR 9 November 2021 ---

KGB & KGB WB

KGB will on the way to lauch a new high of challenging on the old current high and closed with great conviction above RM1.89 .

Will you be the ones , who enjoy the acceptance of joining the party to celebrate with joy.

![How? Invest in Stocks Malaysia [works GREAT from 2021]](https://www.howtofinancemoney.com/wp-content/uploads/2018/04/Stocks-investing-niching-down-micro-sector.gif)

========================================================================

|

Kelington Group Berhad./ 0151 Date |

Price Target

|

Upside/Downside

|

Price Call

|

Source

|

Link

|

|---|---|---|---|---|---|

| 06/10/2021 | 2.01 | 0.270 (15.52%) | BUY | MalaccaSecurities | |

| 06/10/2021 | 2.50 | 0.760 (43.68%) | BUY | KENANGA | |

| 01/10/2021 | 2.50 | 0.760 (43.68%) | BUY | KENANGA | |

| 30/09/2021 | 2.50 | 0.760 (43.68%) | BUY | KENANGA |

=========================================================================

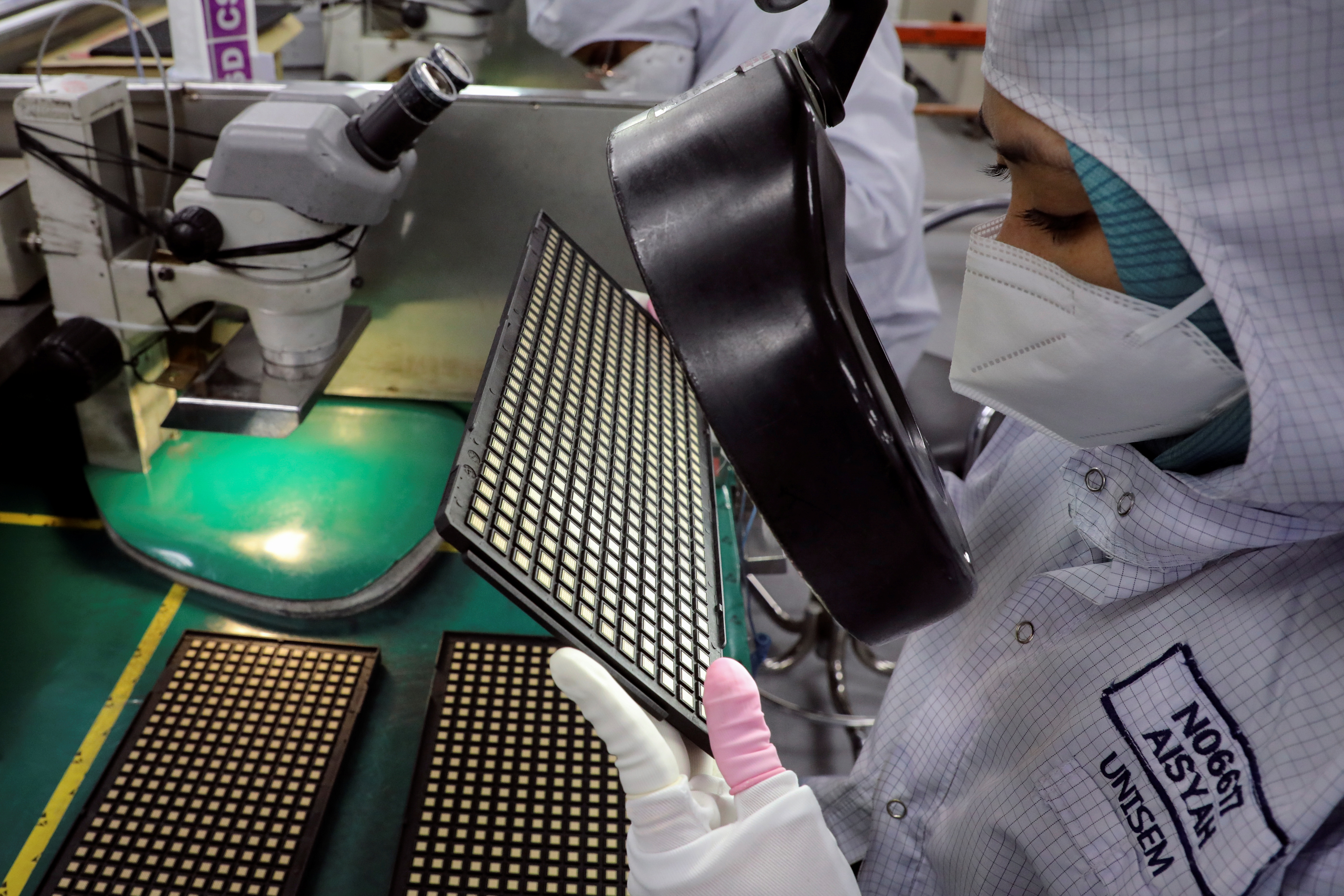

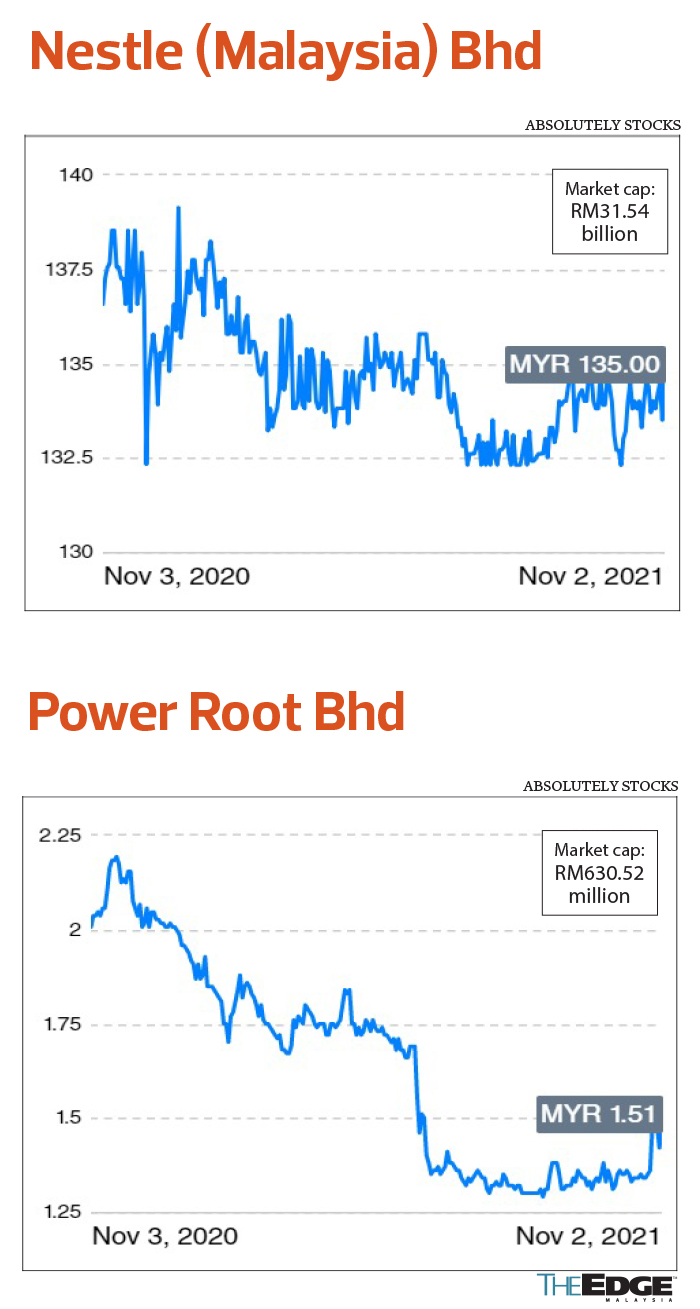

Brokers Digest: Local Equities - Food and beverage, Mr DIY Group (M) Bhd, Kelington Group Bhd, MI Technovation Bhd

The sugar tax may lead to a steep rise in price of pre-mixed products. (Photo by Shahrill Basri/The Edge)

Food and beverage

NEUTRAL

CGS-CIMB RESEARCH (NOV 1): In Budget 2022, the government announced that excise duty on sugary drinks will include pre-mixed preparation beverages (2-in-1 or 3-in-1) effective April 1, 2022. A flat excise duty of 47 sen per 100g will be imposed on pre-mixed products that have sugar content of more than 33.3g per 100g. This includes: i) mixed chocolate or cocoa preparations, ii) mixed malt preparations and iii) pre-mixed coffee and mixed tea preparations. At this juncture, we are unable to ascertain whether the threshold of sugar content is inclusive of natural sugar or solely added sugar.

Companies under our coverage that will be affected are Nestlé (Malaysia) Bhd and Power Root Bhd as they are key players in pre-mixed beverages such as coffee, tea and cocoa. Based on our initial estimates, 50% of Power Root’s domestic sales and 25% to 30% of Nestle’s sales will be affected by this measure.

In our view, pre-mixed producers are likely to take two approaches to this matter: i) raise their selling prices to fully pass on the additional sugar tax, and ii) lower the sugar content in their products to below the threshold for excise duty. Our early channel checks reveal that F&B producers are confident they can reduce the sugar content of certain products with R&D efforts while keeping the flavour of the products. In the event the sugar level cannot be reduced, they will maintain product availability with higher selling prices or launch lower sugar content options.

Based on our back-of-the-envelope calculation, we expect effective selling prices (per 1kg) to increase by RM4.70 (9.3% to 30.5% for products priced from RM7.70 to RM32.90) for every pre-mixed beverage that has sugar levels of more than 33.3g for every 100g of pre-mixed product. In our view, the price increase is steep (assuming the sugar tax is fully passed on), which may lead to lower sales volume due to reduced consumer affordability.

We currently have “hold” calls on Power Root and Nestlé. We also retain our “neutral” call on the F&B sector. Key upside/downside risks include sharp increase/decrease in sales volume.

Mr DIY Group (M) Bhd

Target price: RM4.10 OUTPERFORM

KENANGA RESEARCH (NOV 3): In the nine months ended Sept 30 (9MFY21), Mr DIY’s sustainable Patami of RM297 million accounted for 66%/65% of our/consensus full-year estimates. We consider the results as broadly within our expectations given the Enhanced Movement Control Order in 3QFY21. An interim DPS of 0.7 sen was declared for the quarter, raising cumulative DPS declared to 2.1 sen, (accounting for 88% of our estimate).

The key to Mr DIY’s sustainable profitability is its agility in offering a variety of quality products at affordable prices, coupled with its flexibility in product mix to sustain sales and margins. We expect 4QFY21 results to be stellar, underpinned by the higher percentage of stores in operation and more store openings to achieve the targeted 175 for FY21. Management guided for 180 new stores in FY22.

Post-results, we make no changes to our FY21E/FY22E earnings of RM451 million/RM707 million. We believe the impact from the one-off prosperity tax will be negligible given that Mr DIY has about 14 subsidiaries and most are likely to have a chargeable income of less than RM100 million.

===================================================================

Kelington Group Bhd

Target price: RM2.06 BUY

RAKUTEN TRADE RESEARCH (NOV 3): We see huge growth potential for KGB’s ultra-high purity (UHP) segment as more fabrications come on stream amid a global chip shortage as capital expenditure is rising rapidly in Asia. With its record high tender book of RM1.1 billion, KGB is focusing on bidding for semiconductor wafer fabrication projects in China and Singapore, which are its largest revenue contributors. As at last month, the group had an outstanding order book of RM979 million, of which 58% comprised data projects in Malaysia.

KGB also manufactures liquid CO and dry ice. It has signed a 15-year supply agreement with Petroliam Nasional Bhd to purchase waste CO to sell to re-fillers and the F&B industry or process it into dry ice. The group is in the final stage of securing the halal certification from Jakim to start the qualification process for the F&B industry. We believe there will be some contribution from this segment soon, backed by pent-up demand post-Movement Control Order.

The company has a healthy balance sheet, with net cash per share of eight sen as at 1HFY21. There is room for further expansion with a low gearing ratio of 0.3 times.

=====================================================================

MI Technovation Bhd

Target price: RM5.04 OUTPERFORM

PUBLICINVEST RESEARCH (NOV 3): The key takeaway from MI Tech’s recent virtual briefing is China’s role as a key growth driver for the group’s equipment and material business units in the next two years. We gather that management plans to offer total solutions to Chinese clients for both semiconductor equipment and material products, which would help improve margins and cross-sell products. Nevertheless, final-quarter numbers for this year will be softer due to the ongoing supply destruction and deferment by customers, owing to revised capacity schedules. We cut our FY21-23 earnings forecasts by 4% to 10%.

Top line for the third quarter ended Sept 30 surged 77% year on year to RM114 million. China, Taiwan and South Korea are the top three markets.

The group also witnessed gradual upward average selling price revision for its Taiwan-based solder balls due to the cost hike in materials. It plans to penetrate the South Korean and Japanese markets and aims to slowly phase out the low-margin solder ball business.

Following the successful maiden sale of a laser-assisted bonding machine to a reputable South Korean phone maker, the group is aiming for a 20% to 25% market share as it has started qualification for another potential client.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play

====================================================================

LEFTOVER FOOD WASTE