Trading With A View

(Tradeview 2017) Value Pick No. 7 : Kronologi Asia Bhd. (0176)

tradeview

Publish date: Sat, 15 Apr 2017, 05:07 PM

tradeview

0 209

Author of Once Upon A Time In Bursa : The MONEY Equation. A corporate strategist, lawyer & avid investor who has two great passion in life: Financial Markets & Real Estate. A true fundamentalist and financial writer motivated to tip the scale in favour of retail investors. Believe the stock market can be force for good.

Contact for update : tradeview101@gmail.com

Telegram: https://telegram.me/tradeview101

Contact for update : tradeview101@gmail.com

Telegram: https://telegram.me/tradeview101

Dear fellow readers,

This is my No. 7 Value Pick for 2017.

Once again, these writings are just my humble highlights (not recommendation), feel free to have some intellectual discourse on this. You can reach me at :

Telegram channel : https://telegram.me/tradeview101

Website / Blog : http://www.tradeview.my/

Facebook : https://www.facebook.com/tradeview101/

or Email me at : tradeview101@gmail.com

_____________________________________________________________________________

Value Pick No. 7: Kronologi Asia Berhad (Initial Valuation RM 0.45)

Following the superb performance of Scope Industries Bhd, which moved from 16 sens to 27 sens in 1 month (68% gain since released of article), there were many request by my readers to focus my writing on more small cap stocks. Let me clarify beforehand, this is not adhering to the request but rather I came across this counter after a friend highlighted the strong growth since their IPO 2 years back.

Once again, we will give an upfront warning, as this is a small cap stock, this stock has higher risk compared to our other value picks. So for those who have low risk tolerance, you can skip this.

Kronologi Asia Bhd, is in the business of Data Storage and Recovery Solutions & Technology. In layman terms, Krono provide Data Backup, Consultation, Server Maintenance, Recovery services to companies. Think of them as your office work data archiver / gatekeeper.

The company consist of a team of IT professionals with substantial experience in their respective fields. From how I look at it, the team running the company is very professional. Just to name a few, the Executive Director / CEO /CTO, Mr Teo has over 20 years of experience in storage solutions, software programming and network architecture. Executive Director / Director of Operations, Mr Tan brings with him a wealth of IT experiences having worked for a HK listed IT firm and US based 3Com, both in their Singapore operations. He was also one of the pioneers of a successful regional IT System Integration company, Sandz Solutions. In short, the management of Krono knows what they are doing.

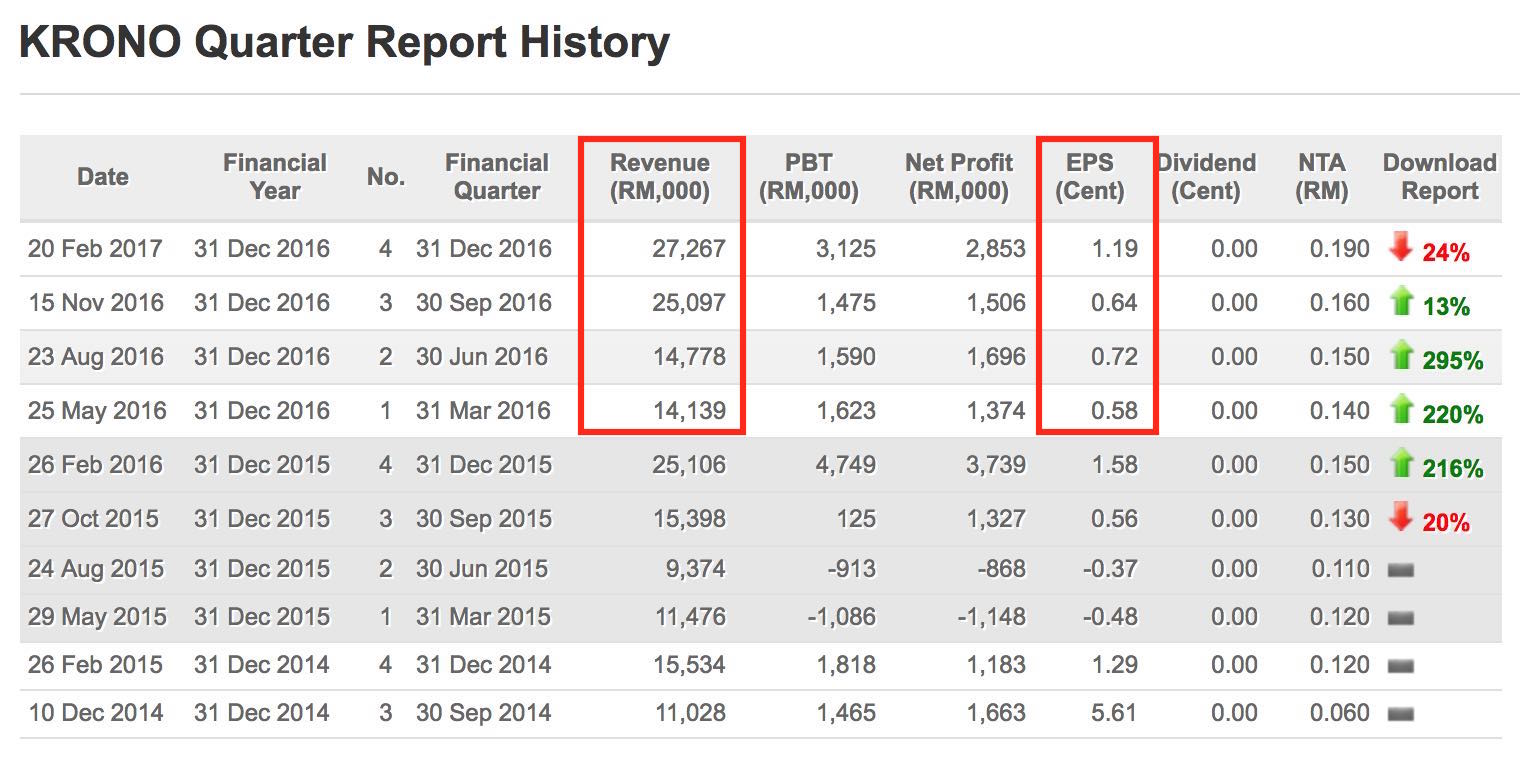

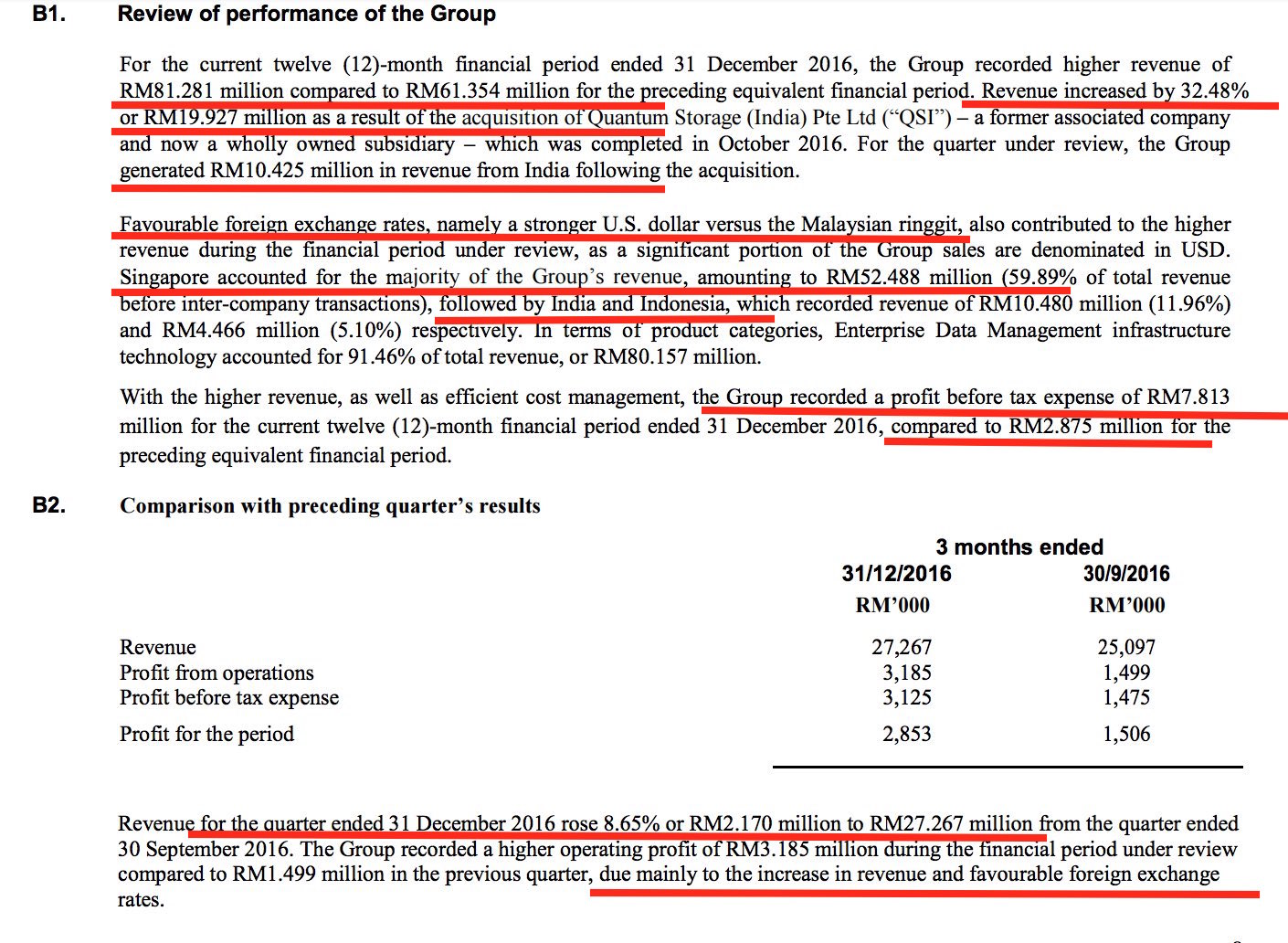

As Krono is a relatively new company, looking at the 2 years profit trend, Krono has shown steady increase both top and bottomline from RM61 to RM81 million in revenue and RM3 to RM7.4 million in net profit. Profit margin almost doubled from 5% to 9.1%. All indicators point towards continuous growth. However, it is imperative to understand the reason behind the growth.

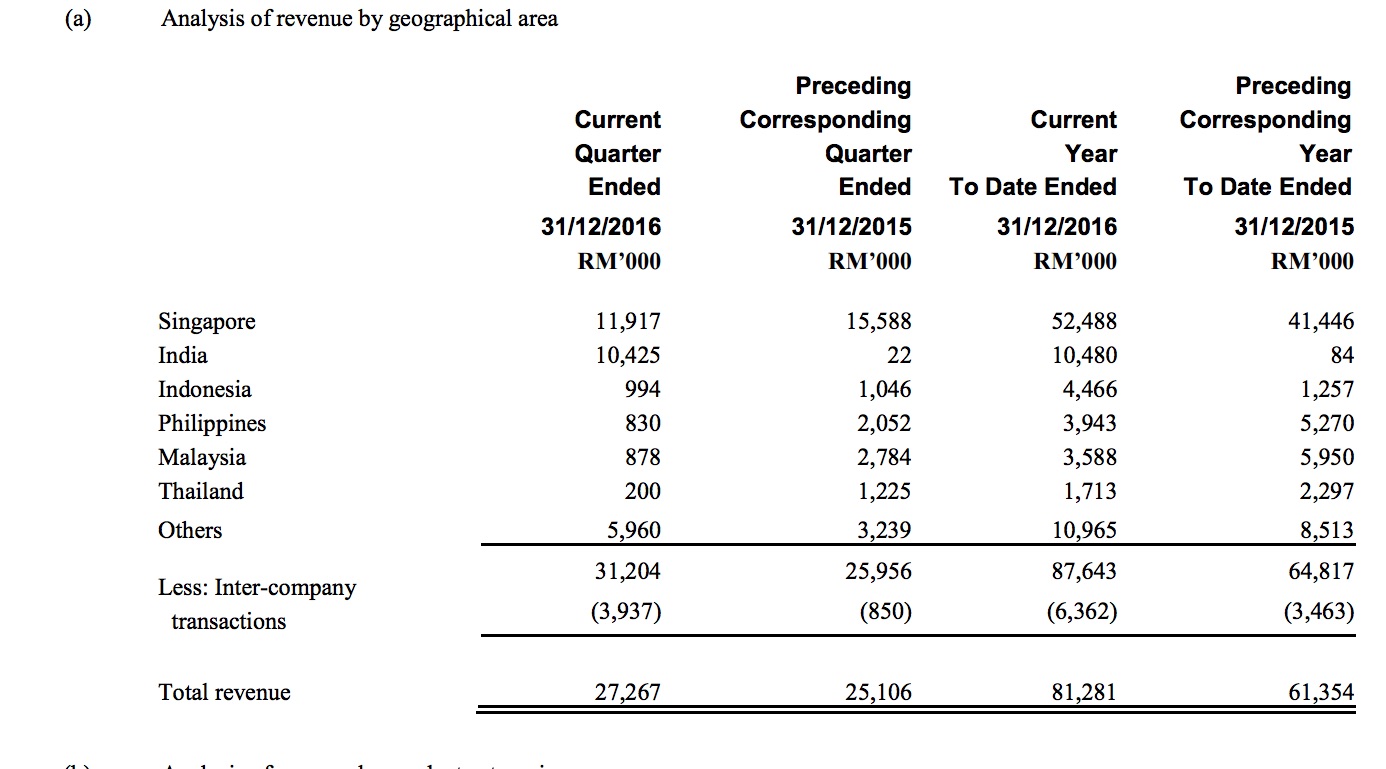

Back in August 2016, Krono acquired the remaining 80% stake in Quantum Storage (India) Pte Ltd for RM26mil. This is one of the key reason for the growth of Krono. With a new subsidiary and board members / management level, Krono has been improving. The key sector for Krono is to tap on the burgeoning data storage and management business in Asia. It is reported that Krono is a long-term partner of US-based Quantum Corp which in turn is a global player in data protection and data management - promoting Quantum products, solutions and branding in South Asia.

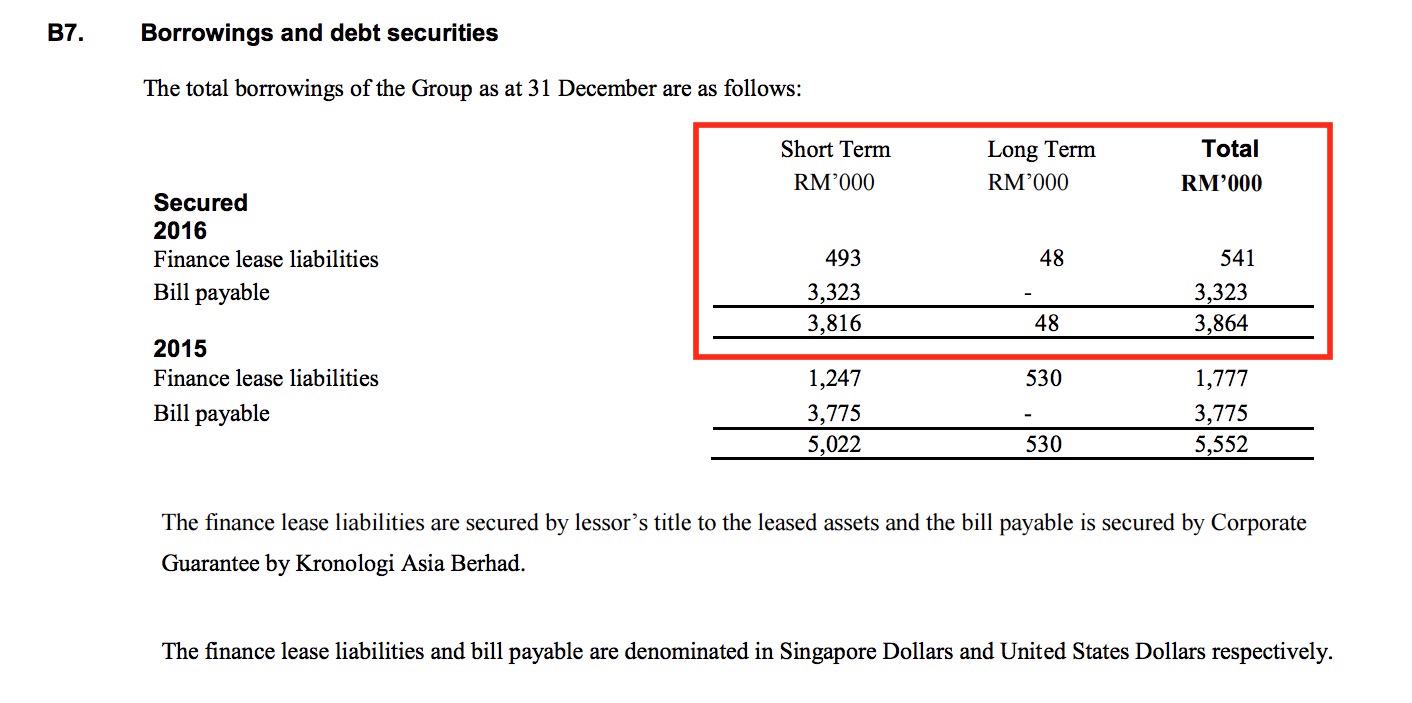

Krono acquisition of Quantum Storage for RM26mil, was satisfied by new shares and RM15.2mil in cash on a staggered payment basis. The acquisition was to capitalise on big data, and India's growth in the sector of data storage. Ex: 4K ultra HD technology, Satellite imagery, CCTV etc. The pivot towards Digital cities, Smart Cities and to boost IT usage in businesses and organisations will help the company grow in the long term. This acquisition comes with a profit after tax guarantee of US$1mil (RM4mil) each year of financial years 2016 and 2017. The RM15.2mil cash portion of the acquisition is being funded from RM6mil of IPO proceeds and a further RM9.2mil from internally generated cash. The company has RM8.7mil in cash as at Dec 31, 2016 with a reducing debt position. Additionally, Krono's balance sheet is relatively strong compared to many other tech stocks out there. It is a net cash company despite having gone through an acquisition.

We like Krono for many reason. Firstly, it has a change in management / board members which turned the business around. Secondly, it is in a tech sector of growth which is easy to understand and shows actual revenue and profit growth. Thirdly, the company have a good mix of revenue from various geographical location which shows demand in various countries outside of the home country. Hence, we believe the future prospect is intact. We are cautiously optimistic for it to maintain its profitability in the coming QR. If Krono successfully pull it off, there may be a rerating to the stock.

The 2017 prospects by Krono looks promising as well. Given the management confidence of being able to deliver a positive performance to FY 2017, I think it is worthwhile to consider investing in the company for the long term basis.

With the latest QR, it is now trading at a narrow band. Since middle of 2015, Krono has fallen from 40+ sens to a low of 10 sens before rebounding to recent high of 39.5 sens. If Krono can maintain their growth, there is no reason it cannot challenge it's historical high. Currently at 35 sens, it is trading at a multiple of 13x. It's NTA stands at 19 sens with ROE of 14.5% for the past years. We believe in the long term growth trajectory of Krono and estimate the coming Q with EPS between 0.7 to 1 sen. Should that happens, the full year EPS will be around 3 sen and applying a multiple of 15x (factor in the net cash position and tech sector), there is a possibility that Krono can move towards 45 sens. For now, this will be the initial TP pending observations of coming quarter results.

*Please note this is a penny stock with erratic earnings. Hence the risk is higher. For those who do not have such appetite, feel free to skip.

________________________________________________________________________________

Telegram channel : https://telegram.me/tradeview101

Website / Blog : http://www.tradeview.my/

Facebook : https://www.facebook.com/tradeview101/

or Email me at : tradeview101@gmail.com

Food for thought:

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Trading With A View

NST Business x Tradeview No.3 - Adam Yeap, Owner of 212 Hospitality and co-founder of Wonderbrew

Created by tradeview | Oct 18, 2021

NST Business x Tradeview No.2 - Muzahid Shah, CEO of SteerQuest Sdn. Bhd.

Created by tradeview | Sep 28, 2021

News Straits Times Business x Tradeview - Sharing Stories of Retail Investors & the Stock Market

Created by tradeview | Sep 15, 2021

Tradeview (2021) - Peterlabs Holdings Berhad Long Term Value Stock (Update)

Created by tradeview | Jun 01, 2021

Tradeview Commentaries - The Glove Surge, A Mirage or A Path To Oasis?

Created by tradeview | Apr 08, 2021

(Tradeview 2021) - Are Research Analysts' Reports Worth Their Salt?

Created by tradeview | Mar 17, 2021

Discussions

3 people like this. Showing 8 of 8 comments

Personally feel Tradeview is a better bet than Calvin Tan. If you follow the former you will know why I said that.

2017-04-30 21:24

Agree with Venfx. Tradeview is a pro, Calvin is a joke. Nothing to compare.

2017-05-01 09:17

When we called Kronologi at 35 sens, our TP based on its fair valuation is 45 sens. It hit the TP last week and further exceeded the FV to hit a new 52 week high of 49.5 sens. To us, it is normal for profit taking as it is within expectation considering the sharp increase in such a short span of time. The first support is 45 sens followed by a strong support at 40 sens. FYI to all. Those that missed Krono can consider collecting on retracement.

2017-05-02 09:44

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-22 16:20:00

EMA 5

5 Mins

BUY

2024-07-22 16:10:00

EMA 5

10 Mins

BUY

2024-07-22 16:00:00

EMA 5

10 Mins

SELL

2024-07-22 16:00:00

EMA 5

5 Mins

SELL

2024-07-22 16:00:00

ADX

5 Mins

SELL

Apps

Top Articles

1

https://dividendguy67.blogspot.com

2

save malaysia!

3

save malaysia!

4

5

Koon Yew Yin's Blog

6

南洋 - 凭单专栏/温世麟

7

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Erudite

Thanks for this tradeview

2017-04-30 20:41