https://dividendguy67.blogspot.com

S&P500 vs FBM KLCI

Background

I trade both the US and Malaysia markets, and it is important for me to understand the differences between both markets.

There are many ways to compare, my favorite is price comparison over the long term as a base-line.

I tend to focus on price only (as opposed to price+dividends) because as a price trader, dividend is not my focus, but I do pay attention to dividends, because as an US Options trader, the impact of price falls after ex-div date is important input and consideration too.

A simple illustrative comparison over the past 20 years

I like to use the past 20 years as illustration, because the results are quite typical over different periods. There may be exceptions, but they are far and few in between and it's good to get a sense on the long term base-line. As we are not one-time traders, but plan to trade over the rest of our lives, we must prioritize the long haul - the long term - the outcome of thousands of trades we will be making over our lifetime.

Key observations

- Over the past 20 years, the US S&P500 has beaten the FBM KLCI by quite a wide margin.

- An original $10,000 invested 20 years ago will have accumulated to $17.6k in KLCI, but would have grown to $51.9k in S&P500, excluding dividends, ignoring forex differences.

- From a CAGR perspective, that's the difference between earning 2.9% per annum in KLCI, vs earning 8.6% per annum in S&P500.

- It doesn't look like much difference (+2.9% vs +8.6%) but over 20 years, this makes HUGE differences. Nearly 3 times the final accumulation.

- Dividend yield helps narrow the gap (as KLCI dividend yield is higher and has tax advantages over US), but doesn't change the total return picture. S&P500 still trounced FBM KLCI returns by a massive margin. Additionally, during this period, the forex gap has widened even more because the Ringgit has devalued significantly.

Key Question #1 - Why didn't we invest in S&P500 20 years ago?

Short answer is - I wished, 20 years ago, I had a Mentor who would slap me in the face 20 years ago and get me to look at this chart much more seriously!!!

Key Question #2 - Why aren't you invested in S&P500 today?

20 years have passed and I have learnt a lot. My US account makes much more than 8.6% per annum returns, so, I don't think it's optimal for me to do this. However for many of my readers, I believe the majority do not beat 9% per annum in which case it may be a valid consideration for diversification reasons. Financial advisors in general consider this to be good financial planning, to diversify one's assets overseas. I am not a financial advisor, but looks to me, even for passive investors, diversifying say 5% or 10% or more of one's net worth overseas is not a bad thing. Many high net worth individuals diversify even more. And passive investing in the S&P500 over the long term like 10, 20, 30 years is not a bad thing to do.

Key Question #3 - Is it too high to invest now?

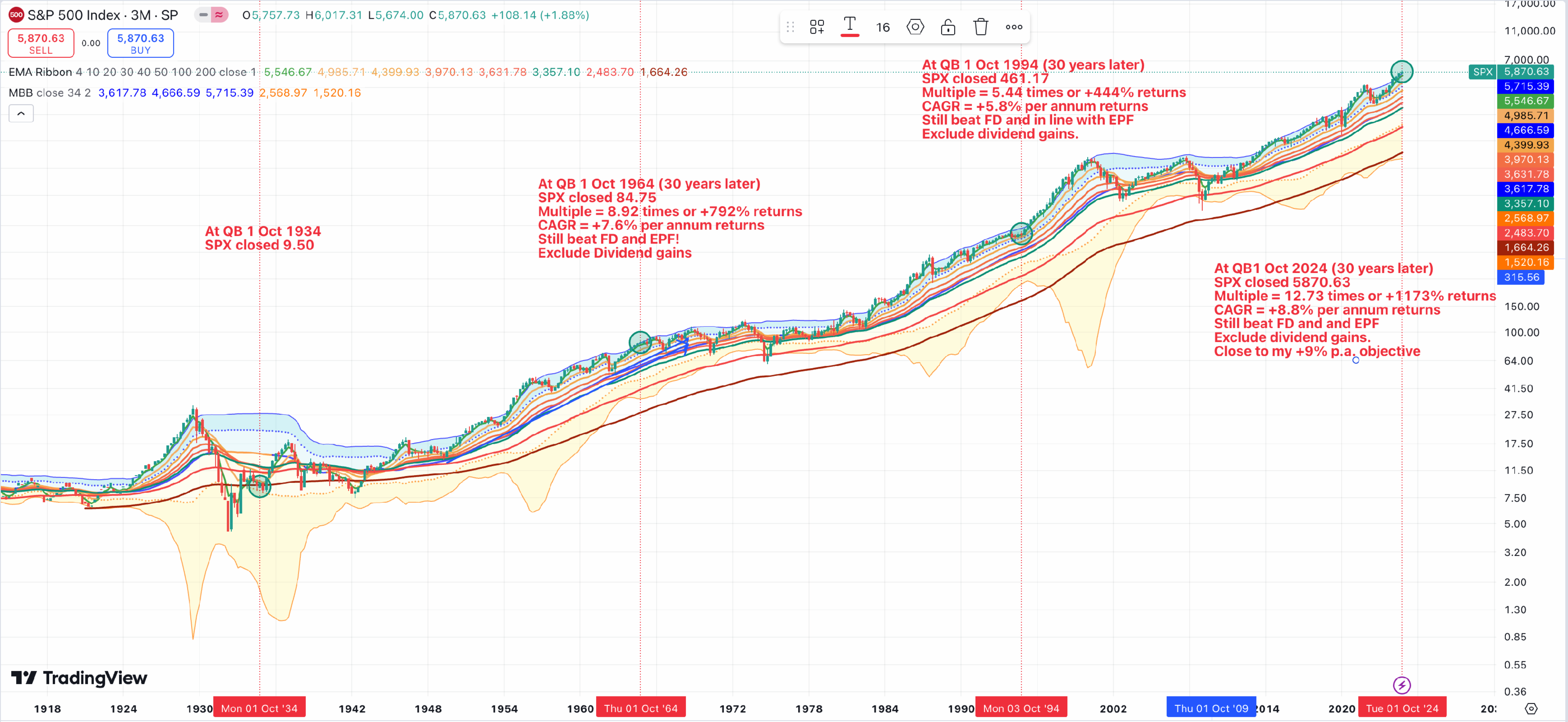

Take a look at this long term chart that compares the S&P500 over successive past 30 year periods over the past 100+ years.

Key observations.

- 30 years ago, on Quarter Beginning (QB) 1 Oct 1994, the SPX closed 461.17. Today it closed 5870.63, or 12.7 times bigger. The CAGR (Compounded Annual Growth Rate) is 8.8% per annum returns, close to my 9% per annum investment objective.

- The thing is excluding dividends and forex gains, 8.8% is a very good return over 30 years. With dividends (despite 30% WHT), it is still better than 8.8%, maybe close to 10% per annum. including forex gains, even higher, as our Ringgit is terrible. This makes a strong case for passive investing.

- However, most people look at 5,870 level and say - gee, that's too high. I'll wait until it drops. It is 100% valid view, provided you do take action when it drops.

- However, most people who says they'll wait until it drops, never took any action. Vast majority of readers of this article (typically hundreds to several thousands) - unfortunately - will not take the action. I'd be pleasantly surprised if this article triggered > 1% to take action. If you do take action, just drop a short comment to let me know. (My base case is noone will comment they took action :-). This is just reality based on past comments, but let's see. Prove me wrong! ).

But isn't 5,870 too high?

- It depends if you are a true long term investor or not.

- It depends if you can set aside your investment, and not look at it for 10 years, 20 years, 30 years or longer.

- It depends if you are a sophisticated investor/trader and your investment objective.

- For this type of investment, it must be monies you don't plan to use nor touch over the next 10, 20, 30 years. If you need the monies, you should not invest in the stock market which can give you unrealized paper losses.

The point about this chart is that regardless of when you enter - whether you enter at the bottom or at the top - the longer time passes, the CAGR will come closer together.

In other words, it really doesn't matter too much where you enter. What matters is "how long" you've been in the market for SPX. Your result matters a lot more if you entered and stick with it for say 30 years, than entering at the low of 1994, vs the high of 1994.

In other words, the day you enter makes little difference vs how long you've been in the market.

That is just the reality of S&P500.

Hard to believe, but prove it to yourself.

1994 Low = 435.86. 30 year CAGR = 9.05%

1994 High = 482.85. 30 year CAGR = 8.68%.

Difference is only 0.37% per annum - smaller than what mutual funds/unit trusts charge you in fees every year which can run up to 1.5% per annum.

In other words, it didn't matter which day you enter, as long as you entered!

Summary and Conclusion

The primary purpose of this article is more to remind me than anything else.

- It is to remind me to show this to my children one day when they become financially independent and start to save monies.

- It is to help them diversify their assets when they start having a Net Worth after they become financially independent.

- Certainly, pay off all your debts where the interests are higher than what you can earn in EPF first. Then, invests in EPF early - e.g.top up your EPF when you can.

- And when you start having positive Net Worth, immediately open a US online brokerage account and then start investing early in S&P500, even before you open a Bursa online account. Diversify and stay in the S&P500 market for as long as you can - 30, 40 years are ideal. Just ignore price fluctuations.

- If by that time, another country like China has surpassed the US, then, consider to do the same and diversify in both countries than just Malaysia.

- And later, open a Bursa account because your liabilities are likely to mostly be in Ringgit for the rest of your life.

- Whilst the USD tend to appreciate relative to Ringgit over long periods of time, nobody knows the long term future and just in case, Ringgit should still be more relevant to you.

- In Bursa, long term investing in high quality dividend stocks is a good hedge and a good way to diversify against EPF and FDs. Do also own the property you live in instead of paying rent.

- More importantly, a good business like good quality dividend stocks (good banks, TENAGA, etc.), bought during market crashes are great way to own good quality investments over the long term. Diversify in case you are wrong.

A secondary purpose is to remind me when trading the US markets.

- The base line returns for DIY investor in the US market is at least 10% per annum.

- The moment you get less than 10% per annum returns, or under-perform SPX - is the time you have to take a very serious look at your own ability as a trader.

- My investment objective is 15% per annum in the US markets. This gives at least a 5% buffer so that I have good chances to beat S&P500 every year into the future.

- It didn't matter that you are beating this by miles already in 2024. Every year have a reset. Come 1 January 2025, it is reset time again, and you have to prove to yourself again next year, and so on. Unless you passively invests in S&P500, then, you can relax one day and ignore this yearly reset as a trader, but by that stage, be prepared to leave this as a legacy too as none of us lives forever.

All the best to those who took action!

Disclaimer: As usual, you are solely responsible for all your trading and investment decisions. Owning overseas assets carries additional forex risks.

More articles on https://dividendguy67.blogspot.com

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

Dragon Leong blog

2

RHB Investment Research Reports

3

Haha and Hehe

4

5

6

MQ Market Updates

7

8

RHB Investment Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....