ee

Is The Semiconductor Cycle Poised For An Upswing? [Goreng Goreng]

gorenggoreng88

Publish date: Fri, 20 Sep 2019, 10:17 AM

Research from https://www.fundsupermart.com.my/m/research/article/11329

The semiconductor industry is best defined by its cyclical swings, and many an investor has tried to profit from its ups and downs. It takes a discerning eye to identify when is the best time to enter the market, and when to exit it. In this article, we explore where we think we are currently in the semiconductor cycle and try to see whether we can profit from it.

Understanding the Semiconductor Cycle

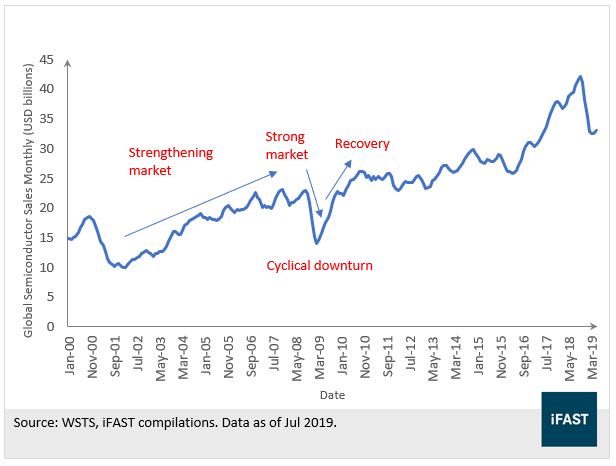

Figure 1: The semiconductor cycle

The semiconductor industry is one that is plagued by cycles; the reason for this is intuitive. A cycle begins with a strong market, where semiconductor companies enjoy strong profits in a market where demand exceeds supply. A favourable market environment encourages semiconductor suppliers to invest in new capacity to meet forecast demand. However, suppliers tend to overestimate end demand in the near-term, resulting in excess capacity. To reduce capacity, semiconductor suppliers resort to price-cutting, which lowers profits for the semiconductor industry as a whole – resulting in a weak market, where semiconductor firms experience weak financial results and therefore weak share price performance.

At the same time, companies cut back on factory utilisation to limit further inventory build. Then, just as semiconductor companies tend to overestimate demand, they also tend to cut back by too much during times of weakness, leading to supply shortages, which takes time to be corrected by a ramp-up in utilisation. In the meantime, prices move higher, and semiconductor companies enjoy stronger profits. The interim period becomes a strong market where semiconductor companies enjoy higher prices and therefore profits.

Where Are We Currently In the Semiconductor Cycle?

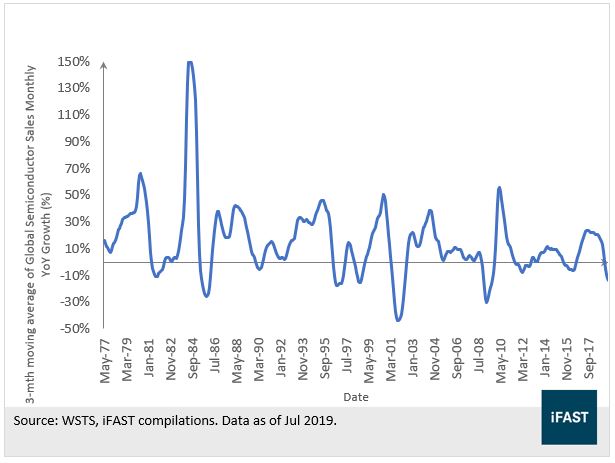

Figure 2: The semiconductor cycle 1977-2019 expressed by global semiconductor sales growth

As we can see in Figure 2, going back to 1977, the semiconductor industry has experienced 10 upcycles and 10 downcycles. On average, upcycles tend to last approximately 3 years (38.7 months) while downcycles tend to last approximately 1 year (12.1 months). We can see a trend that the upcycles seem to be getting shorter, pointing to the impending maturation of the semiconductor industry. If history is any guide, we appear to be about 7 months into the current downcycle, indicating that the next upcycle may be starting soon.

Table 1: Semiconductor industry’s length of cycles

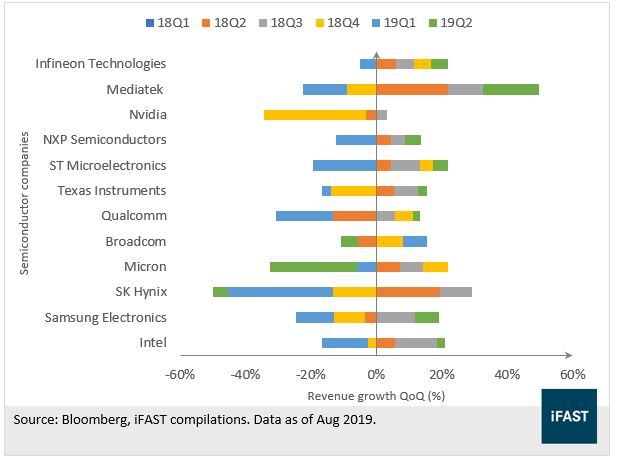

Figure 3: Semiconductor companies are seeing revenue growth in 2Q 2019, possibly signaling an end to the industry downcycle.

Most of the biggest semiconductor companies experienced declines in their sales in 4Q 2018 and 1Q 2019, as seen in Figure 3. At the same time, most of the companies are beginning to show signs of recovery in 2Q 2019. This is an indication that 4Q 2018 may be the beginning of the current semiconductor downcycle, with 2Q 2019 possibly being a return to normalcy for the industry.

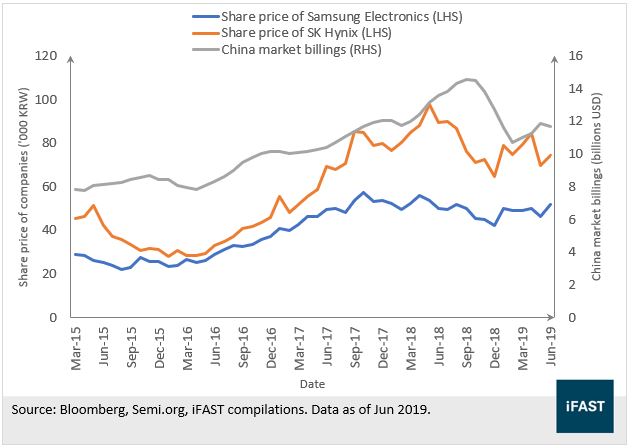

Figure 4: There is a relatively strong correlation between China market billings and the share price of semiconductor companies, indicating that an improvement in the former would lead to an upcycle recovery

Apart from improving revenues, global semiconductor sales also appear to be bottoming having experienced a slight dip in 1Q 2019. Market billings of China, in particular, rose to $11.8bn for May, after falling to $10.7bn in February. China is the biggest consumer of semiconductors worldwide, so a recovery in sales in the region is a refreshingly positive factor for global semiconductor demand. If Chinese semiconductor billings continue on an upward trend, it may signal the end of the downcycle and a hopeful recovery into the end of 2019.

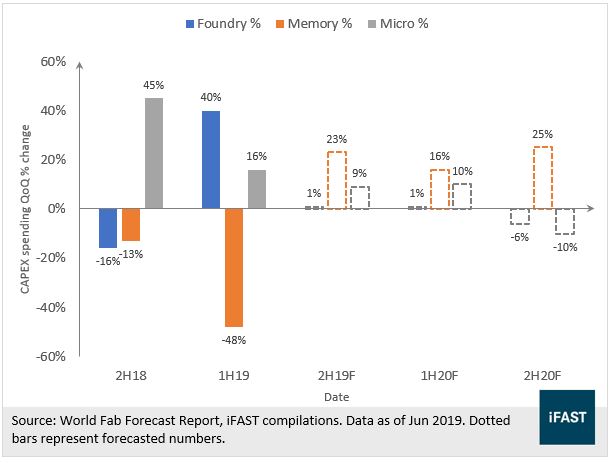

Figure 5: Semiconductor companies are expected to ramp up CAPEX going forward, signaling the end of the industry downcycle

There is also the matter of capital expenditure, otherwise known in the industry as CAPEX. CAPEX is a leading indicator as regards to the performance of the industry, as semiconductor companies will only ramp up spending when their internal forecasts show there is increasing demand. In 2017 and 2018, semiconductor companies invested heavily in CAPEX as it was a strong market and forecasts showed increasing demand. However, real end-demand deteriorated in late 2018, leading to a cut in capital expenditures, as shown in Figure 5. The reduction in capital expenditures was most prominent among memory companies, which showed a -48% decrease in fab equipment spending during 1H19, with investments in sector components 3D NAND and DRAM plunging 60% and 40% respectively.

Despite the reduction in spending, overall spending in 1H19 was partially offset by a 40% jump in investments by leading foundries, showing that the major manufacturers are still committed to capital expenditures amidst heady times. Micro spending also grew 16% in the first half of the year with a 9% increase projected in the second half. Memory investments are poised to turn the corner in 2H19 with growth of 23%, bringing the industry CAPEX back to a recovery stage. We expect that the recovery of capital spending towards the end of the year means that semiconductor companies are seeing increasing demand in the quarters to come, which might spell the end of the downcycle.

Given the above, we think that the downcycle that started in 4Q 2018 is approaching its end and that there are enough signs (revenue trend, China semiconductor billings and CAPEX forecasts) to show that the semiconductor cycle will likely witness a turnaround by 2H 2019.

The Semiconductor Industry Has Tailwinds In The Long-Term

While slowing global aggregate demand and the uncertainty stemming from US-Sino trade war is clouding the earnings prospect of the semiconductor industry in the near term, the industry is still one of the bright spots for the market over the long-term, with decent tailwinds behind it. Having gone through an explosive growth catalyzed by the huge surge in demand from PC and smartphone markets, the next phase of growth is now driven by various new and exciting technologies, which include the Internet-of-things, artificial intelligence, automotive, data centres and wearables.

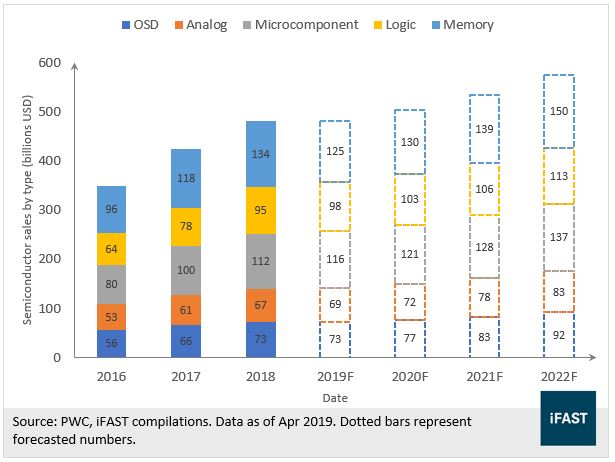

Total semiconductor sales are expected to rise from just shy of $500 billion in 2019 to nearly $600 billion in 2022. The automotive market is expected to grow the fastest, with a compound annual growth rate (CAGR) of 11.9% through 2022 on the back of stronger penetration of electric and hybrid vehicles. Meanwhile, the industrial market is seeing increasing demand for chips in both the security and healthcare-related sectors and is expected to grow at an annual CAGR of 10.8% throughout that period.

Figure 6: Despite the recent slowdown, the semiconductor industry is expected to grow healthily into 2022.

The consumer electronics market is projected to grow by a CAGR of 6.0% through 2022. Also, the communications market is expected to grow by a CAGR of 2.2%, a decent showing for a largely saturated market with plateauing characteristics. The data processing market is expected to grow by a CAGR of 2.1%, which will stem from sales of servers and storage devices.

All in all, there is still room for growth for the semiconductor market as a whole. Secular tailwinds mean that investors who are in for the long-term have the opportunity to benefit from the next wave of growth in the semiconductor industry.

Conclusion

To sum up, it appears that we could be approaching the end of the semiconductor downcycle, which presents a buying opportunity for investors. Historical data supports that the cycle could turn by end-2019 to early-2020, supported by the recovery of CAPEX and a rebound in global semiconductor billing. Also, the long-term prospects for the industry remain bright, with the advent of new technologies and breakthroughs coming over the next few years. Investors who wish to capture the upswing may consider it worthwhile to have exposure to the semiconductor industry for the growth opportunities it offers.

Investors who wish to gain exposure to the impending upswing of the global semiconductor industry may consider investing in the Eastspring Investments Small-Cap Fund, which has a 16.99% weighting in stocks with significant exposure to the semiconductor industry.

A comparison of 3 M'sian Gem Featured In Forbes Asia's 200 Best - ELSOFT, VITROX, PENTA

5G network likely to spur demand for semiconductor components [Goreng Goreng]

Ooi Kok Hwa: We are heading tech rally like Y2K due to Digital Transformation [Goreng Goreng]

Ooi Kok Hwa: Bull market in stocks has years to run

Ooi Kok Hwa: The share market will be extremely bullish!

Goreng Goreng Goreng.....

More articles on ee

Semiconductor industry set for growth or further slowdown? [Goreng Goreng]

Created by gorenggoreng88 | Oct 29, 2019

A comparison of 3 M'sian Gem Featured In Forbes Asia's 200 Best - ELSOFT, VITROX, PENTA

Created by gorenggoreng88 | Aug 27, 2019

Pentamaster diversifies to broaden income base [Goreng Goreng]

Created by gorenggoreng88 | Jun 17, 2019

5G network likely to spur demand for semiconductor components [Goreng Goreng]

Created by gorenggoreng88 | Jun 12, 2019

Rebound seen in smartphone sales; boost for some M'sian tech firms [Goreng Goreng]

Created by gorenggoreng88 | May 02, 2019

Global semicon sales down 5.7% y-o-y in January to US$35.5b, says SIA [Goreng Goreng]

Created by gorenggoreng88 | Mar 05, 2019

Global semicon sales crossed 1 trillion mark in 2018, says SIA [Goreng Goreng]

Created by gorenggoreng88 | Feb 18, 2019

Featured Posts

Latest Videos

Apps

Top Articles

2

BFM Podcast

3

BFM Podcast

4

BFM Podcast

5

BFM Podcast

6

save malaysia!

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

No trading signals available.

Stock

Time

Signal

Duration

No trading signals available.

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....