MoneY is KinG

PTRANS (0186) – Double Digit Growth Rate in FY2019

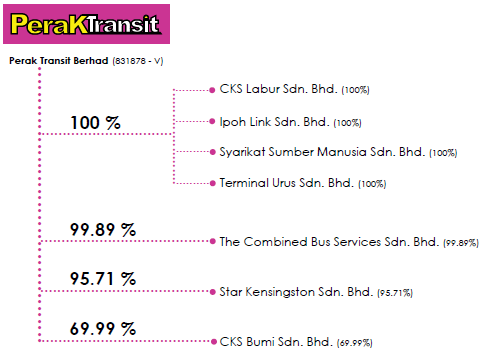

Perak Transit Berhad is a Malaysia-based company, which operates as the investment holding company of Perak Transit Group. The Group is principally engaged in the operations of Terminal AmanJaya, an integrated public transportation terminal located in Ipoh, Perak, Malaysia. Perak Transit Group's major business activities are classified into three segments: Its terminal operation segment, including the leasing of advertising and promotions (A&P) and retail spaces at the terminal and the renting of the terminal's equipment, utilities and facilities; its public bus services segment, pertaining to the operation of express and stage buses and the provision of bus chartering services, and its petrol station operations segment, referring to the management of petrol stations. Besides, the Group provides human resource management services and manages a basement car park.

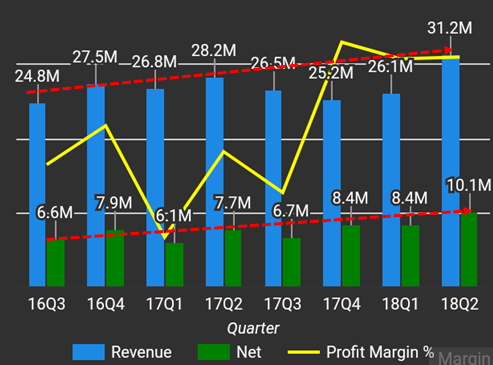

BRIEF: For the six months ended 30 June 2018, Perak Transit Bhd revenues increased 4% to RM57.4M. Net income increased 35% to RM18.6M. Revenues reflect an increase in demand for the Company's products and services due to favorable market conditions. Net income benefited from Other Operating Income increase of 60% to RM1.6M (income). Dividend per share totaled to RM0.01.

Based on the recent Q2 2018 result, Ptrans is recorded the highest quarter for revenue and profit. This profit generated is only based on current terminal Amanjaya. Results high possibility can double digit up after Kampar terminal is done in Q4 2018. You can see the profit trend is keep increasing. Ptrans can consider as one of growth company in ACE market.

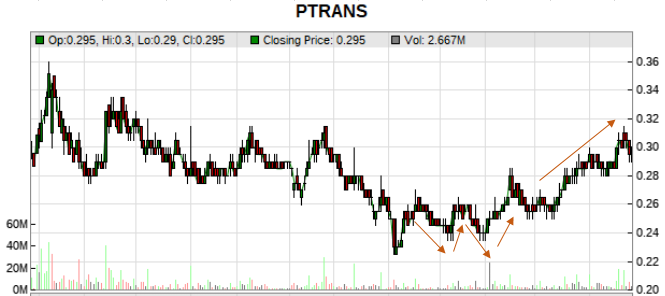

Based on the chart, bottom “W” is form up, and support is around 0.285. Next resistance is at 0.32. Cut loss if fall below 0.26. Based on current investment bank analysis, TP is 0.41, but believed the TP is much higher due to monopoly business in Perak state, PER around 16X for small cap company plus FY2019 profit estimated around RM50m (RM12.5m per quarter). Therefore, TP FY2019 is set at 0.59. 100% increase based on current price.

Advantages of Ptrans:

1. Monopoly business in Perak state.

2. Going to transfer from ACE to main board listing in Q3 2018, this is the main cartelistic to move the share price.

3. Terminal Kampar will be completed in Q4 2018.

4. Stable share price plus good dividend pay-out.

5. Consistent fuel price is benefit to transportation and petrol station business.

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on MoneY is KinG

3A Resources (0012) – Company focused on F&B Ingredients in Malaysia Market

Created by issic622 | Nov 10, 2017

FPGROUP (5277) – Another Shining Star SemiConductor in Penang Base Company

Created by issic622 | Oct 05, 2017

BIOHLDG (0179) - Strong Sales in China & Indonesia Following New Product Launches

Created by issic622 | Jun 14, 2017

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

RHB Investment Research Reports

4

CEO Morning Brief

Anwar Launches UK’s Most Sustainable New Town in Bristol by YTL

5

TA Sector Research

6

MQ Market Updates

7

Rakuten Trade Research Reports

8

Mercury Securities Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....