Random Trading

Sumatec - What is the end game of TSHS?

Random Trading

Publish date: Sat, 30 Aug 2014, 07:31 PM

Random Trading

0 44

Too dumb to be an expert, too green to called a veteran and certainly not an insider. what's left..... RANDOM!

Disclaimer - I'm too dumb to be an expert thus all the contents of this blog are just my random thoughts and may be incomplete or contain any informational errors. It is certainly not recommendation to buy or sell. You'll be responsible for your own decision. Please consult your investment consultants before making any investment decision.

Disclaimer - I'm too dumb to be an expert thus all the contents of this blog are just my random thoughts and may be incomplete or contain any informational errors. It is certainly not recommendation to buy or sell. You'll be responsible for your own decision. Please consult your investment consultants before making any investment decision.

Sumatec is arguably the most attractive stock to watch for the last 2 months. In fact, this counter has hogged the limelight for quite a long time last year. I'm intrigue by the story behind the huge surge in price and trading volume of the company so I try to look back when and how Tan Sri Halim Saad (TSHS), man of the hour, came into the company. Is going to be a long post so just bare with me here because is a long story.

On May 30 2013, Sumatec announced that the company proposed reduction of 21 sen of the share capital comprising ordinary shares of 35 sen to 14 sen a share. Then it would issued 335 Million new ordinary shares of 14 sen to 'selected investors' at 17.5 sen a share. After that it would proposed renounceable rights issue of up to 2,722,220,957 new Sumatec shares with free detached warrant (Warrant-B) with every 41 rights for every 10 shares with every 1 free warrant for every 4 rights subscribe. For details of the multi-proposal, you can refer to Bursa on this link :

The 'selected investors' that involved in the private placement of total 335 Million shares at 17.5 sen a shares that mentioned above comprises of :

TSHS - 150.4 Million shares with total amount to RM 26,320,000

Chua Ma Yu (CMY) - 30 Million shares with total amount to RM 5,250,000

Corston-Smith Asset Management (CSAM) - 59.6 Million shares with total amount to RM 10,430,000

Tekad Mulia Sdn Bhd (TMSB) - 95 Million shares with total amount to RM 16,625,000

So from here we know how TSHS came into the picture. CMY, the co-founder of RHB Bank is of course very well known in local investment community. One can easily find a lot of information on the tycoon by just googling the web. CSAM is a mystery since they are fund manager that acting on behalf of their client which they never reveal. TMSB is an investment holding company. You certainly needs to remember this name because it will appear again later in this article.

So from total 335 Million shares, TSHS got 44.9%, CMY 9% , CSAM 17.8% , TMSB 28.4%. I will collectively called them 'TSHS group' from here onward, of course I'm not saying they are actually a group or act in concert, is just that it makes it easy for me to analyze. (Better to have a disclaimer!!!)

TSHS group then subscribe the total rights entitled to them which amount to 1,373.5 Millions rights (41 : 10) at 17.5 sen a share with total 343.375 Million Free Detached Warrant-B (WB). After the rights subscription, the group holds total 1,708.5 Million shares + 343.375 Million WB with total cost of RM 298,987,500 or average cost of 17.5 sen a share and all WB for free.

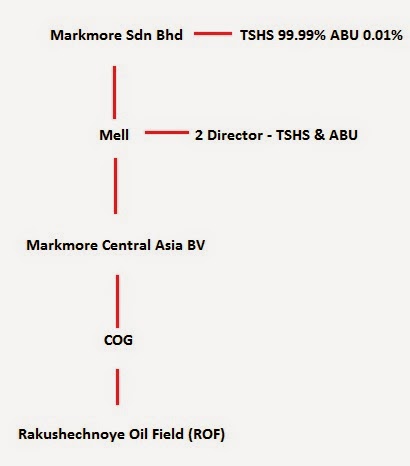

The abovementioned corporate proposal is a regularisation plan to revive Sumatec by using the proceed from the private placement and rights issue to buy Rakushechnoye Oil Field (ROF) in Kazakhstan. COG is a company that held the concession to ROF and it is a subsidiary of Markmore Central Asia BV (MCA). MCA in turn is owned by MELL, a company with 2 director which were non other than TSHS & Abu Talib bin Abdul Rahman (ABU). Please remember ABU because he is a very important figure that will appear again and again in this article. Mell is wholly owned by Markmore Sdn Bhd which is control by TSHS with 99.99% & ABU with 0.01%. (Yes, it clearly shows that who is the BOSS). Chart below clearly stated the inter-relationships of all the companies and peoples involve.

Under the Joint Investment Agreement (JIA), Sumatec will act as contractor to concession owner COG to develop the oil field under Production Sharing Contract (PSC) until 25 Aug 2025 which first 2 years Sumatec will get all the profit while 3rd years onward will be 50:50 between Sumatec & COG.

Under the terms of JIA, Sumatec would paid a signature bonus of RM 31 Million, Cost Reimbursement of RM 263.5 Million and refundable performance deposit of RM 124 Million which is deducted from future oil royalty as well as USD 5 royalty per barrel to COG. Total initial outlay will be RM 418.5 Million.

Thus, basically TSHS need not pay a dime for Sumatec shares but by indirectly swapping it with the oil field concession and with some RM 280 Million spare cash since his portion of investment in Sumatec only cost RM 134.25 Million.

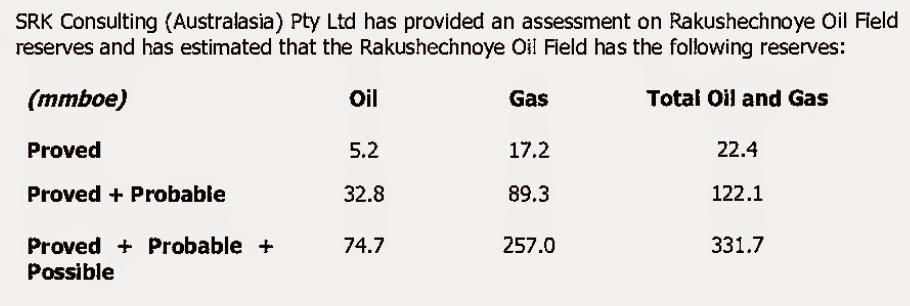

So, how good is this oil field? Here is the estimated oil reserves :

mmboe - Million barrel of oil equivalent

Proved reserves: 22.4 mmboe, Probable reserves: 99.7 mmboe, Possible reserves: 209.6 mmboe

Ya, proved reserves only constitute to 6.75 % of total estimated reserves andPROBABLE + POSSIBLE reserves constitute the rest of 93.25%, WOW!!!

It certainly needs to be very 'Probable' and very 'Possible' to justify the investment of Sumatec.

How is the performance of this oil field? Well, to date, the oil field has contributed RM 4.852 Million and RM 7.237 Million respectively for the last 2 quarters. It is certainly not much but is enough to lift the company from PN17 status. Granted, the profit might increase further with more oil well in production but Sumatec certainly need to hurry up because they only enjoy full profit for 2 years then it will only be 50% from 3rd year onward.

So, up till now, TSHS got some RM 280 Million cash + 767 Million Sumatec ordinary shares total amount to RM 356.655 Million (with last closing price of 46.5 sen) + 154.175 WB total amount to RM 60 Million (with last closing price of 39 sen) in return for his concession in an oil field that yield total RM 14 Million for the last 6 months. NOT BAD!!!! Isn't it? Oh ya... the oil field has potential..... so we can't value it that way. TRUE? I think I better leave it for you to judge since I don't know how to value PROBABLE & POSSIBLE PROFIT.

If you ask me how much is the entry cost of TSHS investment in Sumatec, I think on paper it is 17.5 sen a share with free WB. In real term? I seriously don't know how to calculate.

So what now? Sumatec again propose another rights issue with free warrant at an indicative price of 40 sen. you can read more about the proposal from my previous post :

so I'm not going to too much details of the proposal here. The proceed of the rights issue is to actually buy an oil field instead of JIA or PSC. The propose acquisition of the oil field cost USD 350 Million and will be satisfied by cash and shares. Some 727,272,727 shares will be issued to one of the vendor ABU and TSHS will subsequently buy all the shares from ABU for 55 sen a share. YESYESYES!!! this ABU is the same ABU that mentioned above. Still remember our ABU? May be is just a coincident the both gentleman have the exact same name. It could be. The total payment to the vendors are USD 99.45 Million + 727,272,727 shares and USD 95.55 Million to one Dr. Murat Safin. (Both can scream HUAT AH.......)

So on paper, TSHS is actually pumping more money into the company by subscribing the rights issue entitled to him for RM 153.4 Million + purchase from ABU for RM 400 Million. Since TSHS is going to buy at 55 sen a share even after the rights issue, so what are we waiting for?????

OHH!!! But wait, What IF........

Just HYPHOTHETICALLY say...... if TSHS & ABU are actually same interest party!!! I'm just saying hypothetically, I'm not saying it is. (I have made my disclaimer here again). Under this scenario, they actually get the USD 99.45 Million (RM 318.24 Million with 3.20 currency conversion rate) to subscribe for the rights issue of RM 153.4 Million with some RM 164.84 Million pocket change and the RM 400 Million is just left hand in, right hand out! NICE.... So what is TSHS investment in Sumatec shares this round again??? Under this scenario, I will say.... looks to me is free capital outlay again in exchange for another oil field. How good is this oil field??? just refer to my previous post from the link above then you know what is my opinion on it.

Under this scenario, if he subscribes for all the rights issue entitled to him (he already undertaking them) ultimately TSHS will possess 1877.8 Million shares of Sumatec ordinary shares with 154.175 WB and 383.52 Million new warrant (WC) + FREE CASH of total RM 280 Million from 1st round and RM 164.84 Million from 2nd round which total amount to RM 444.84 Million. The price for all these assets is just 2 oil fields with HUGE PROBABLE & POSSIBLE RESERVES!!!!

How committed is TSHS in this company? On paper he really invest a lot..... The truth......

The only question I have in mind is what is his end game? He certainly can't sell any shares in open market or even marry deal since investors will see it as sign that he is bailing out. So how this will play out. Honestly do he needs to sell to make money from this 'investment'? To me he already made plenty. That's why I don't even want to mention how the share price perform in this article because I don't think it matters too much to him.

He is not selling but someone does :

Source: I3investor.com

Yes, is a long list. To save your trouble, the 3 repeated names Chan Yok Peng, Tekad Mulia Sdn Bhd (TMSB) and WAN KAMARUDDIN BIN DATO' BIJI SURA @ WAN ABDULLAH share the same address. I made some rough calculation, they collectedly disposed off some RM 72 Million worth of ordinary shares and RM 24 Million of WB.

What is TSHS end game??? I don't know. Is he in this company for long term? May be!!!

Anyway I'm just going to say HUAT AHHHH...... TSHS & HAPPY MERDEKA TO ALL!!!!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Random Trading

Discussions

7 people like this. Showing 50 of 57 comments

This is most appropriate for stayer : http://www.youtube.com/watch?v=MpGgCrcfWBg

Enjoy !

2014-08-30 23:38

Honestly, my intention of this article is not to say whether Sumatec is worth investing or not because I can never know what is TSHS motive in his investment. I think only he knows about it. This article is just my way of putting all the facts that I can get about how this counter become what it is today from some 2 years back. Often times we trade stocks just looking at its current state because we are too close to it but forget about the bigger picture about the history of it. Here is how I try to remind myself about what had happened to this counter for the last 2 yrs. Whether to invest or not is up to individual investor. But the facts remains the facts.

2014-08-30 23:49

Rt, this sumatec story to hype up n keep doing right is to fund the methanol plant which is a real asset. Not some 10 yr leased of probable.

2014-08-31 00:03

:) haiya most of scandal begin with accounting mislead... youngman read many2 case study before making any story :) take time to understand ...why TSHS making such move, gen-y still a lot to learn ^^

2014-08-31 00:12

@Random Trading.... some points for your info and to fill up your "jigsaw puzzle".

1. CSAM founder is Datuk Shireen Ann. She is the only Malaysian in the list of 2014 Forbes Asia Most Influential Businesswoman. CSAM mostly invest in equities, IPO and pre-IPO. She was proposed to be appointed as director for Sumatec (refer to Sumatec corporate brochure). In the same brochure also proposed Datuk Johari Razak for director (accepted the position some 2 month ago).

2. Tekad Mulia, Chan Yok Peng & Wan Kamaruddin - they are from Sumatec old management, and the deal is for them to reduce their share holding in Sumatec. That's why their names in the Bursa announcement on director disposal. The proceeds..... please check CNASIA.

3. By convention, an oilfield/reservoir is valued by its 2P, Proved + Probable reserves. In layman term, use car as an analogy, standard performance stated in catalogue as PROVED, ie once you drilled, then you got the oil. The car engine is added with turbo system, that is PROBABLE, ie to enhance the oil production rate (by well intervention, workover, infill drilling etc. like what Sumatec is doing now to increase to 2000bpd by year end). Engine overhaul as POSSIBLE. Worth to note another term C, CONTINGENT. With the advance of drilling technology, the C can be upgraded to P.

4. The risk of Sumatec business - apart from world oil price fluctuation, is the drilling enhancement activity (workover programme). The real/true characteristic of the well can only be progressively studied/known during drilling/production. This is evidence as shown in the Q2 report where Sumatec is facing a hiccup in workover program. The advantage of this is it serves as learning curve for Sumatec as stated in the report, the action taken to mitigate the hic-cup. This experience is useful in dealing with well and/or Buzachi field.

5. The Gas Development & Production Agreement, GDPA was not bundled together in regularisation plan. It was an additional agreement for gas development and production, 2014 to 2016 with a fee of USD 45M (3 years ie USD 15M per year). That is a guaranteed profit quaterly (eventhough there is a hiccup in oil production). An arrangement crafted to ensure 2 consecutive quarterly profit for PN17 upliftment.

6. News on TSHS and Kenmakmur plus another one (forget the name) signed MOU in Kazakhstan during PM Najib visit, to build methane plant (TSHS), LPG plant (Kenmakmur) and another guy (orchard farming???). Kenmakmur (owned by CYP & WK) sign a Framework Agreement with CNASIA in June 2014, to design, build and operate the LPG plant. The plant will be the off-taker for Sumatec/CaspiOil gas from Rakushenoye field. Reckon that CNASIA will do the cash call (bonus, enlarge capital, Right Issues, Warrant & RCPS) as the estimated cost would be USD 200M. In return, CNASIA will get profit guarantee of USD 55M/year for 5 years after full operation, estimated end 2017.

7. Since Kenmakmur is buying 100 MMSCF of 120 MMSCF from Rakushenoye field, which means only left 20 MMSCF for TSHS methane plant. Therefore, the raw material (gas) for methane plant should be from Buzachi field.

_______________________

Ok, now for the wishful thinking (this is a disclaimer).

Some rumours going around that linking Petronas with Sumatec.

Actually Petronas want to have foothold in Kazakhstan, but cannot since TSHS is already here. TSHS & the gang is a big "taiko" in Kazakhstan (do you know that due to TSHS, Malaysian do not require a visa to visit kazakhstan). The only way is for Petronas to invest through TSHS. So Petronas need to take up some stakes in these LPG & methane plant and in return TSHS will get some portion of investment in Turkmenistan.

So there you go.... the sinister plan of TSHS revealed.... (another disclaimer)

--------------------------------------

2014-08-31 08:22

Hi ogre, really thanks for your input. It really enlighten me on certain issues. As for sinister, I do agree with Rahim3088 that being smart doesn't mean he is sinister at least innocent until proven guilty right. I always stated that I'm not saying the whole Sumatec thing is a scam because so far he did deliver his promise by injecting O&G assets and successfully lifted PN17 from the company albeit made a killing out of it. But if he is going to bring Sumatec to become a serious O&G player with partners like Petronas and bring sustainable profit to the company and shareholder then I will have to say he deserved the money he earned. Let's us see what is his next move and whether Sumatec can really be transformed into a great O&G player. It is going to be very interesting.

2014-08-31 08:49

Posted by SANG-JERO > Aug 30, 2014 10:08 PM | Report Abuse X

No need to argue....Fund managers/Institution will look at the numbers stated below plus

forecasted numbers before putting in their money.....

I f you think good ..BUY....If you think lousy and you cannot make money....keep your money in the bank or ASB etc.....period..

Let's see what happen on tuesday onwards.

Real time TA also looks fine barring any unforeseen circumstances.

Revenue ('000) 27,488

Profit Attb. to SH ('000) 105,629

EPS (Cent) 16.26

PE 2.86

DPS (Cent) 0.00

NAPS 0.1460

ROE (%) 111.37

--------------------------------------------------------------------------------------------------------------------

P/s: Solly ahh..my england and matematic no good.....I good in Tunnnnnnnnnngguuu only

2014-08-31 11:21

Hi s123445, act the 280M is not exact figure. Is derived from the initial payment from Sumatec of total 418.5M minus his share of placement plus rights issues total amount to 134.25 M. So the act amount is around 280M.

2014-08-31 20:26

@Random Trading, thank you for your good effort in putting up the pieces/puzzles behind Old and New Suma.

While chasing for more profits, many fail to see the ugly side. They will brash aside any negative info or fact (intentionally or unintentionally) to achieve their objectives and continue to denies any warning signals be it good or ugly.

Appreciate your openness in sharing info. Love to hear more from you.

Happy Investing!

Rich Dad: Money Don't Grows on Tree.

2014-08-31 20:55

Hi smartinv, in the market for any stock there must be some people bullish and some people bearish about it that's how we got seller and buyer so the transaction can happen. Buy or sell, bullish or bearish are just individual investment decision. The thing is some take it too personally and became very hostile if there is any info or comments that they don't like. Once a wise man told me that don't take any particular investment too personally, it will cloud your judgement. I believe this is one of the best advice I ever had.

You too Happy Investing!

2014-08-31 21:38

Rt, I guess as much but the numbers were 284.25 so thought I missed out something

2014-08-31 21:52

@Random Trading.

Agree with you on "Once a wise man told me that don't take any particular investment too personally, it will cloud your judgement".

Thank you for the sharing.

2014-09-01 07:30

Good morning,

@Random Trading

I love to follow some facts. Very interesting and logical.

Yet this is business world. Old adage.. business and pleasure do not mix..

Keep it up your analysis. Good game anyway.

2014-09-01 07:59

This just the beginning of TSHS game... Sumatec is his stepping stone for the come back...

You should read into CN Asia MOU with KenMakmore as well...

Then you will get a bigger picture of what he is planning to do...

2014-09-01 13:15

Cheers for such an informative article for people interested in Sumatec but not interested enough to do such a lengthy research. Keep up the good work, appreciate it!

2014-09-01 15:47

Sumatec + PDZ will be bigger than Malaysia Petronas after the share increase to RM 20...

2014-09-01 17:23

"akh731 Sumatec + PDZ will be bigger than Malaysia Petronas after the share increase to RM 20... "

Blind faith without substance!

2014-09-01 18:30

TSHS reportedly making a come back with a Bang! More counters is connected to him like Sumatec, CN Asia, Borneo Oil, PDZ and more to come. Look like he is buiding his Listed Empire again similar to the Renong Group back in the 90s?

He is the prodigy of TDZ and could have strong financial backing by TDZ.

Retailers frenzy provide good support to his coming back story. Lets see institutional funds willing to join the wagon after upliftment of Suma from PN17.

Happy Investing Everyone!

Rich Dad: Money dont grows on trees.

2014-09-01 19:18

Haha, smartinv, the renong saga still not fully solved and the public still don't know (someone knows I guess) exactly what happened then and now another renong is in the making already! Is interesting. If Sumatec, PDZ and the others are going to become part of the new 'renong' group then we shouldn't wait anymore to jump on the bandwagon! Looks like RM 20 a share is not too far away I guess...

2014-09-01 19:41

Imagination run wild.... all the more on low iq ppl...in an absive country

2014-09-01 19:44

Random Trading, thank you for sharing, I really appreciate your good effort.

2014-09-01 20:11

thank you random trading for sharing the detailed history of sumatec and the big names involved. the upliftment of suma from PN17 is not certain yet, any news on the upliftment??

2014-09-02 00:30

Bro.. Tekad Mulia is part of the old management of Sumatec...Under the agreement with the new Suma management ( Which you can say is their White Knight) they are supposed to dispose their shares after a certain period...So nothing alarming there...

You should put in more effort to do more research on the matter rather than just speculating in bad faith as some investors may be spooked as they would think that there's something funny going on there when actually its not (on this matter)...Otherwise to me your article is fine and informative...(However your credibility and accuracy is somewhat spoilt by that negative bit about CYP & Wan from Tekad Mulia disposing their shares)....

2014-09-02 00:53

Hi Aladdin, as I said, I only stated the facts. Those directors selling their shares is a fact and I didn't mentioned anything that it is not a good sign or alarming sign. I simply stated that they are disposing. So to take the info as positive sign or negative sign is up to individual reader. So if anyone think is negative sign then is their own discretion. Sorry if it spook you away from this counter. You should just ignore the article and proceed with your trading plan.

2014-09-02 08:43

what's the reason for the complicated exchange of shares, rights, just so to confuse us further? Thus before I actually put in my hard earned money, I want to fully understand the reason for these cross dealings. Thanks to Random Trading for the sharing and research. We are one step better informed.

2014-09-02 09:24

Looks like road blocks slightly clearing. Hope there will be showtime and fireworks in 2nd session haha.

2014-09-02 10:34

petikan...

17.5 sen a share and all WB for free. harga sekarang dah banyak untung....

2014-09-02 15:37

Interesting criminal thought and some good comments.

From my experience, I don't think they will be able to cash out with this kind of movement. If this is a scam, it's not attractive yet to pull the net. There are more to come..

2014-09-04 17:42

Hi DumbnDumbe, ya, I do think that if this is really just a pump and dump thing, it is not yet the time to pull the net. This counter will probably be the most speculative and highly traded stock for quite awhile. If it is really a real growth story, it will certainly be the most exciting stock in recent history. If it is a scam then it still has the rights issue to play out so the end game won't be so soon. As for some investors that believe that as long as TSHS is not selling then there is no reason to do so themselves, they should recall what happen to stocks such as Mtronic, Harvest, AGlobal (now rename Nextnat) and Scomnet. Raymond Chan, the center figure of these stocks only sold his shares at 'loss' after the share price collapsed. But we all know that he is certainly not losing money for his 'investment' in those stocks. So if you follow the 'I only sell if he sells' strategy, I afraid it could be too late.

2014-09-04 20:19

Nice article. fact help us to think clearly. Do you know where we can dig more info about sumatec? in term number of human resources, the breakdown of where they put the money and to whom?

2014-09-05 09:05

Haha..Thanks for bringing up Raymond Chan.

I would say that is a classic example on how cashing out is done. Create the hype. Spiked it up and distribute it all the way down. Trouble with people is that they always sees it this way- how much it has fallen from the peak and not how much it has risen from the bottom. One can never maximize profit but able to maximize the loss.

After saying that, you can't really compare apples to oranges. If I were to compare tshs case with another company, I would liken this to Ekran case by looking at its modus operandi. And not Tenggara Capital in year 2000 as that scam lasted only 2 and half months from a low of 1.45 to peaked at 8.70 in that short period.

Just my 2 sen thought here. Applying disclaimer just like you. Haha!

2014-09-07 14:45

what is the end game of Tan Sri Halim Saad?

i know! it is to build up Sumatec to be a big, respectable, profitable and fearful world class O&G player.

2014-09-07 16:46

RT......your article definitely has enlightened many ppl regarding Sumatec......but many can see only the trees but not the forest.......its very difficult to TSHS to remove the stigma as "con man" he is trying to prove his innocence thru Suma & fulfilled his promises......everybody shd be given a second chance.........it would be interesting to know what actually you think of HS & Sumatec besides laying out the facts.......

2014-09-07 17:04

Hi Noraini, to be honest, I don't really trust him or any well connected tycoon for that matter. As I mentioned above, to be smart like him as indicated in this article doesn't mean he is a 'con man'. He could be seriously looking to build something or a legacy for himself since we all know he doesn't really needs the money or the fame and so far he did lived up to his promises. So as I said, only he knows what is his plan. If he is serious about it and build it in good faith then honestly it is good for the shareholders, if not then we all know how it will ends. Let's see!

2014-09-07 17:48

sumatec npdz belum berakhir,next week is second chance spt yg dikatakan oleh puan noraini...friday siapa sangka boleh up terutamanya pdz..inilah malaysia market,,hanya siapa yg berani saja dapat beli harga rendah..pergerakan diluar jangka..saya mengambil pengalaman pdz ketika harga 27c dua tiga minggu lepas tiba2 melonjak 34n dan seterus ke 42bsebelum jatuh minggu lepas .begitu juga sumatec..mari kita renong ,org yg beli suma harga 50,52 dan keatas mesti mengharap harga naik lagi dgn pelbagai cerita tentangnya.kesimpulannya suma n pdz masih relevan next week n bergerak positif

2014-09-07 18:05

1st round made plenty of money by swapping JIA of Raku oilfileld with cash and shares

What happen?? Cant even deliver the projected profit for 2014??

2nd round to make plenty more money by swapping lost making companies which owns the new oilfields even when these oilfieds are already producing oil??

2rounds and to make plenty also??

With toned down profit projection for 2014??For investors :What happened to Suma shares when it reached 60+sen?

2ndround and future profit projection ammounting to rm billions based on what??

Definitely cannot be based on the 1st round swapped assets which cant even delver as projected in 2014

Based on the newly acquired assets owned by two companies losing money even when these assets are alredy producing oil??

What is the end game??

Any substance to back all this projections when a mere rm60+ cant be achieved for 2014??

More questions than answers??

Any good news for.......

..........Investment or Entertainment........??

2014-09-23 13:45

I go along with randomtrading and appreciate his articles for me to make an informed decision as an investor and i also have heard few times before where money is concerned.......TRUST is a fool 's CURRENCY........anyway i agree ........lets see

2014-09-23 14:31

The sell down of the counter before the RI is quite surprising especially it is currently trading so close to the indicative price. 40 sen is a quite an important support so if it breaks then things might get very ugly. For those bought the mother share near the peak already loss one third of their investment. It is even worse for the warrant holders that see half of their investment gone. Of course, as long as you don't cut loss it is still only a paper loss, but how long one can hold? Can you afford not to have any cut loss point at all? Is up to individual investor to decide.

2014-09-23 18:14

WOW! This is an excellent post of very high quality. I was doing some research on beaten down oil & gas counters and making a list of companies "with potential" to invest/speculate in. Sumatec is one of them. Your post here has helped A LOT towards my understanding. Thanks for your great effort. I will be reading your other posts too, that's for sure. It's very difficult to find quality analysis and posts concerning Bursa Malaysia but I'm encouraged after reading this.

By the way, the Corston-Smith Asset Management Managing Director in Malaysia is Datuk Shireen Muhiudeen who writes "Governance Matters" in StarBizWeek on Saturdays. For what it's worth, my wife was her classmate at BBGS in the 70s and she knows what type of person Datuk Shireen is. I'm very sure she had done a lot of research on Sumatec before approving the purchase for the client, whoever this may be.

And the involvement of people like Halim Saad and also Chua Ma Yu - they have the experience and credibility. This isn't a group of market manipulators out to hype and chase up a counter... and then selling off for huge profits after retail investors had piled in. I believe they are after genuine projects with potential. I'm going to put Sumatec at the top of my list regardless of the O&G turmoil, crude oil prices etc. The present low price presents an opportunity for those who have holding power.

Thanks again for this very informative post.

2014-12-08 14:50

I think the guys at sumatec are as bewildered as every one else out there. How will they navigate through the current environment?? I cannot help thinking that THS has made a booboo...and as proven in the past his so called expert team of managers are not particulary expert. He has a history of not succeeding outside of Malaysia.

2014-12-21 22:13

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

HLBank Research Highlights

2

RHB Investment Research Reports

Market Strategy - Data Centre-Artificial Intelligence Party Pooper

3

HLBank Research Highlights

4

Kenanga Research & Investment

Renewable Energy - Big News, Another 2GW LSS Incoming (OVERWEIGHT)

5

PublicInvest Research

Northern Solar Holdings Bhd - Solar RE Specialist with PV Asset Portfolio

6

Mercury Securities Research

7

TA Sector Research

8

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

rikki

@randomtrading....thank you again for the excellent report. Looks like all the money was/are coming from investors. Sumatec is also putting all the eggs in one basket. Khazastan, how's the country risk & ratings ? Don't think any of our Malaysian banks interested.

Sumatec also managed to get for the approval to uplift from PN17 super fast. How long did Ho Hup took ?

By the way, why are there no Investment Bank research on this Sumatec even though already profitable 8 months ago? Why was Sona already covered by HLIB & and given loan by BNP eventhough still reporting losses? I leave the question for our investors to answer.

2014-08-30 23:32