TDM 另类2月之星

最近由于油棕价格大幅度走高,因此有许多投资者也开始关注跟油棕种植相关的种植股,而一些种植股因受投资者的追捧而走高。

投资者追捧种植股并非没有道理,因为7月至9月份时,CPO价格介于2200令吉至2600令吉之间;可是迈入2016年10月份后,CPO的价格已经从2600令吉走高至目前的3100令吉以上。

以下为2016年CPO每个月的均价:-

然而,棕油价格一片大好的时刻,却有很多种植公司在这个时候面对产量下跌的窘境。所以CPO走高未必会惠及所有油棕种植公司, 产量下跌或许还会抵消CPO价格上扬所带来的好处。

因此在挑选种植股的时候,必须特别留意产量和价格这两个因素。

目前,在众多种植股当中,我只留意一家种植公司,那就是TDM(嘉隆发展,2054,主板种植股)。

我会关注它的原因其实很简单,因为这家公司最近的产量提升。在大多数种植公司都面对产量下跌的时候,TDM的产量不仅没有下跌,反而还大幅度提升。

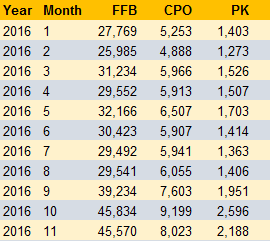

先来看看以下TDM截至2016年11月30日的油棕产量数据:

接着,再将以上数据按季来整理:

2016年第一季:FFB 84987吨,CPO 16107吨,PK 4203吨

2016年第二季:FFB 92141吨,CPO 18327吨,PK 4625吨

2016年第三季:FFB 98267吨,CPO 19598吨,PK 4720吨

2016年第四季:FFB 91404吨,CPO 17223吨,PK 4784吨

注:第四季数据只有10月和11月,12月的数据还没公布

从以上的整理后的数据来看,第四季虽然只公布了两个月的数据,但是无论在FFB、CPO及PK都已经接近,甚至超越第三季度的产量。

个人觉得只要12月份的产量不出差错,那么第四季总产量铁定会超越第三季。但要12月发生产量突发性暴跌的可能性几乎是不可能,

TDM第四季的业绩将会在2017年2月份公布,因此可留意该股的走势并且部署至2月业绩公布的时候。