CEO Morning Brief

Analysts View Axiata’s Ncell Stake Sale Positively Despite Low Valuation

edgeinvest

Publish date: Tue, 05 Dec 2023, 09:01 AM

KUALA LUMPUR (Dec 4): Axiata Group Bhd's swift divestment of its 80% stake in Nepal-based mobile service unit, Ncell, for US$50 million (approximately RM233.6 million) is seen as a positive step despite low valuation, said analysts, considering market concerns about uncertainties regarding the telecommunication group’s ability to find a suitable buyer for Ncell.

This is due to the prolonged regulatory challenges and uncertainties surrounding Ncell, related to the outstanding capital gains tax (CGT).

In a note issued on Monday, Kenanga Investment Bank Bhd said the estimated sale valuation for Ncell translates to 0.3 times the enterprise value/Earnings before interest, taxes, depreciation and amortisation (EV/Ebitda) for the financial year ending Dec 31, 2024 (FY2024).

This valuation seems comparatively low when juxtaposed with the three-year average valuation of Axiata’s listed assets in South Asia, including Robi Bangladesh (5.1 times) and Dialog Sri Lanka (2.4 times), it said.

“Recall that back in 2016, Axiata purchased Ncell at US$1.37 billion which implies significantly higher trailing EV/Ebitda of 5x. On the bright side, although the sale amount appears low versus its original purchase price of RM6.4 billion (based on current exchange rate), it is partially cushioned by Ncell’s total dividend contribution of RM2.2 billion over 2016-2023,” said the research house.

Separately, RHB Research said Axiata’s position of a “clean exit” without an open tender suggests that it was willing to part ways with concessions, resulting in the lower but assured upfront cash payment of US$50 million from the sale and potential dividend income, which are contingent on Ncell’s performance for the financial year ending Dec 31, 2023 (FY2023) to FY2029.

Regarding the impact on Axiata, given its substantial debt load, RHB’s analyst stated to The Edge: “There will be financing risks (more so if there is a larger exposure to US dollar) and where there is a higher proportion of floating rate debt. It would be incumbent upon the telco to deleverage”.

Axiata’s short-term borrowings stood at RM2.74 billion as at the nine-month period ended Sept 30, 2023 (9MFY2023), down from RM7.09 billion as at end-2022, while long-term borrowings rose to RM22.08 billion from RM18.35 billion. The group also has settled a total of US$422 million or RM1.8 billion in CGT to date.

TA Securities Holdings Bhd, on the other hand said, the clean exit would help alleviate the persistent concerns about Axiata’s investments in frontier markets such as Myanmar, Indonesia and the Philippines.

Against Ncell’s guided book value of RM378 million post recent impairment, the fixed consideration of US$50 million implies a price-to-book value (PBV) of 0.6 times, it said.

“Despite the discount, we view it as justified by: i) Axiata’s indemnity against the existing sizable and future Nepalese tax claims, and although less upbeat, ii) potential upside from the conditional consideration, which includes any windfall gains,” TA Securities wrote in a separate note.

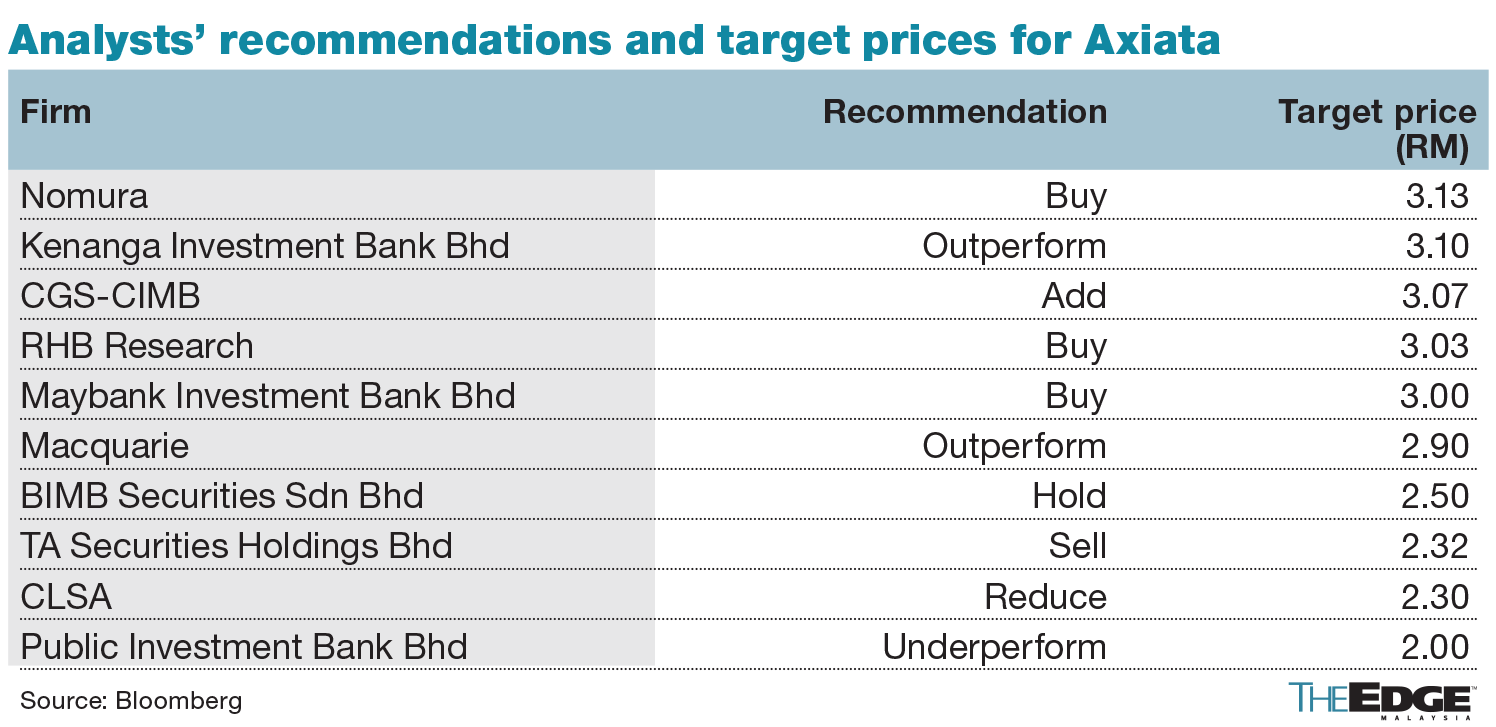

Kenanga revised its target price (TP) downwards by 13% to RM3.10 (previously RM3.55) while retaining its forecasts and "outperform" recommendation. The adjustment in TP aims to more accurately mirror the listing status of Axiata's overseas units, including XL, Robi, and Dialog.

RHB, continues to recommend a "buy", albeit with a reduced TP of RM3.03 (down from RM3.18) following the exclusion of Ncell. The research house has not adjusted its earnings forecasts at this point, awaiting additional insights from management. Axiata is slated to hold its annual investor day on Dec 6 with updates on its asset delayering and monetisation opportunities.

TA Securities, meanwhile, kept its "sell" call, with a lower TP of RM2.32 (from RM2.35). It trimmed its earnings forecasts for Axiata by 3.1%, 16.1% and 12.9% for FY2023, FY2024 and FY2025.

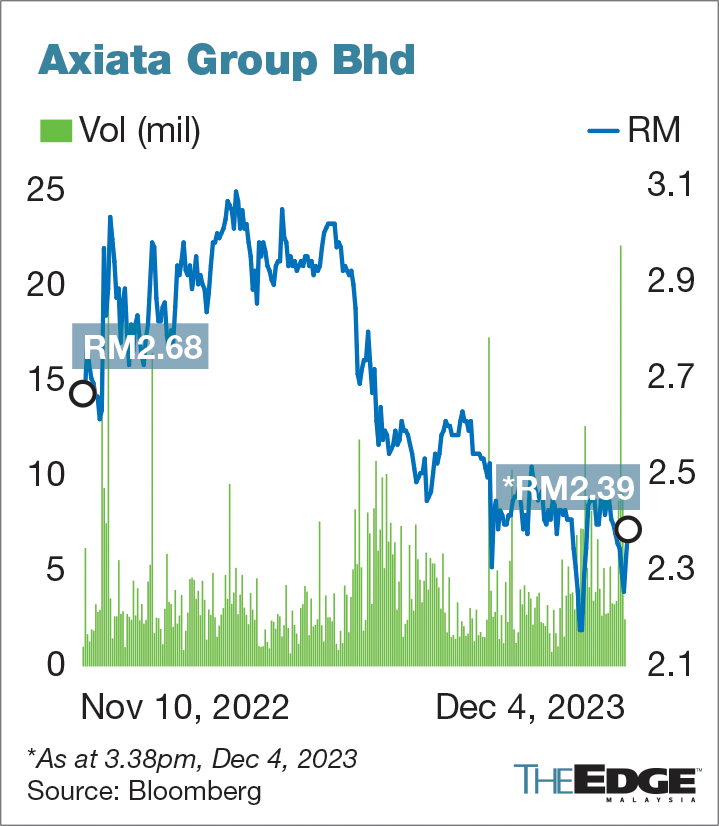

At the time of writing on Monday, shares of Axiata were seven sen or 3% higher at RM2.40, giving it a market capitalisation of RM22.03 billion. The counter has fallen over 19% year-to-date and 22% in the past year.

Source: TheEdge - 5 Dec 2023

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-08-23

AXIATA2024-08-23

AXIATA2024-08-23

AXIATA2024-08-22

AXIATA2024-08-22

AXIATA2024-08-22

AXIATA2024-08-21

AXIATA2024-08-21

AXIATA2024-08-20

AXIATA2024-08-19

AXIATA2024-08-16

AXIATA2024-08-15

AXIATA2024-08-14

AXIATA2024-08-14

AXIATA2024-08-14

AXIATA2024-08-14

AXIATA2024-08-14

AXIATA2024-08-14

AXIATA2024-08-13

AXIATA2024-08-13

AXIATA2024-08-13

AXIATAMore articles on CEO Morning Brief

High Court Allows Felda and FIC to Obtain Two Classified Reports as Evidence in Semarak Land Suit

Created by edgeinvest | Aug 23, 2024

RM49,000 Deposited Into Wan Saiful's Personal Account Two Years Ago, Says Witness

Created by edgeinvest | Aug 23, 2024

'Lembu' and 'durian' Among Codes Used by Officers at KLIA Allegedly Involved With Syndicate

Created by edgeinvest | Aug 23, 2024

1MDB-Tanore: Defence Says Jho-Low 'mirror-image' of Najib Theory Lacks Proof

Created by edgeinvest | Aug 23, 2024

Naza-Berjaya JV Files Notice of Discontinuance Over Challenge of Govt Vehicle Fleet Project

Created by edgeinvest | Aug 23, 2024

Kerjaya Prospek Unit Sues Yong Tai Subsidiary Over Alleged Unpaid Sum of RM105 Mil

Created by edgeinvest | Aug 23, 2024

PTT Synergy Inks Deal With China's Siasun to Distribute Autonomous Equipment in Malaysia

Created by edgeinvest | Aug 23, 2024

Hextar Retail to Introduce Hong Kong's Tam Jai Noodle Chain in Malaysia

Created by edgeinvest | Aug 23, 2024

Capital a Secures US$443m Revenue Bond to Strengthen AirAsia Fleet, Financials

Created by edgeinvest | Aug 23, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

.png)

MQ Trading Signals

Time

Signal

Duration

Type

2024-08-23 16:30:00

EMA 5

5 Mins

BUY

2024-08-23 16:05:00

EMA 5

5 Mins

SELL

2024-08-23 15:35:00

EMA 5

5 Mins

BUY

2024-08-23 15:30:00

EMA 5

5 Mins

SELL

2024-08-23 14:55:00

EMA 5

5 Mins

BUY

Apps

Top Articles

1

Mercury Securities Research

2

save malaysia!

3

4

The Alpha Trader

7

8

THE INVESTMENT APPROACH OF CALVIN TAN

JCY (5161) Posted a 2nd Qtr of Good Profits: Showing a Clear Sign of A Turnaround, Calvin Tan

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....