CEO Morning Brief

China Unexpectedly Cuts One-year Policy Rate by Most Since 2020

edgeinvest

Publish date: Fri, 26 Jul 2024, 10:11 AM

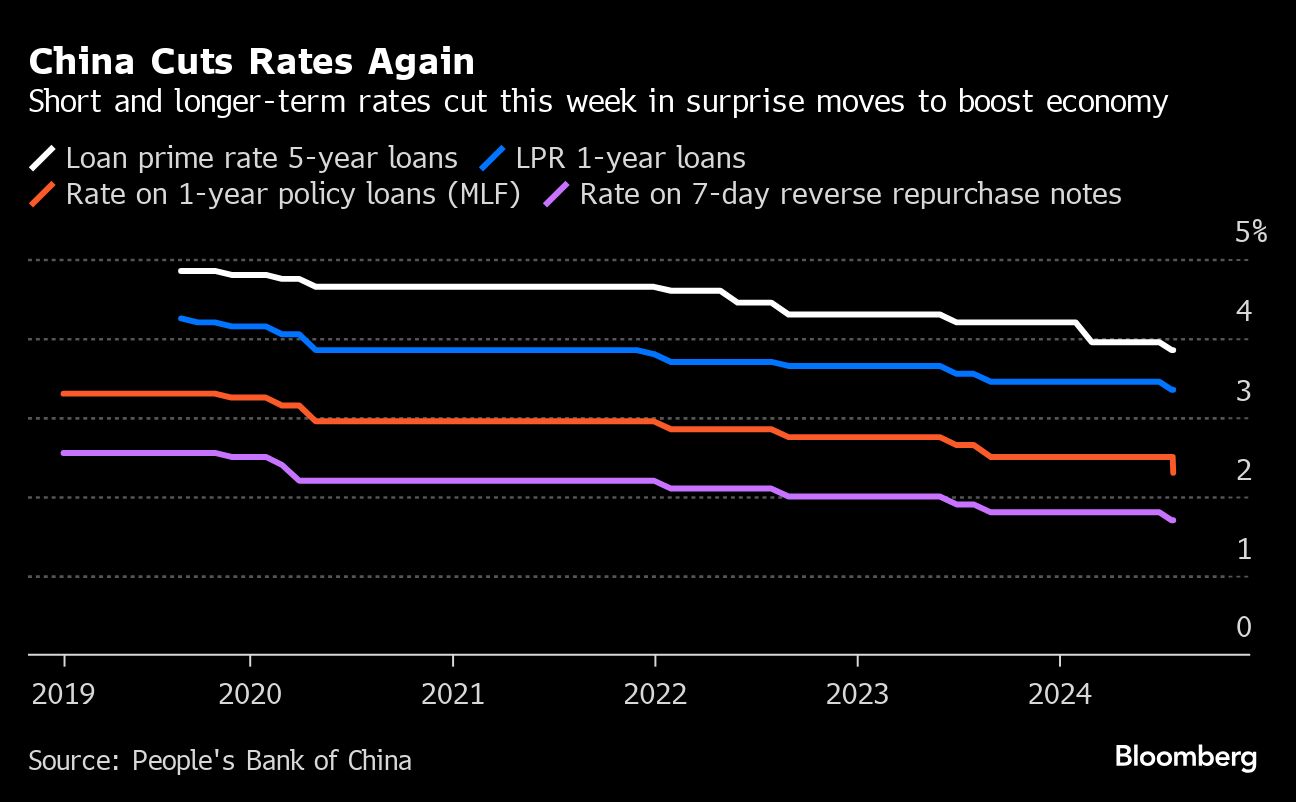

(July 25): The People’s Bank of China (PBOC) unexpectedly lowered the rate on its one-year policy loans by the most since April 2020, days after cutting a key short-term rate, in a sign of greater support for the slowing economy.

The central bank lowered the rate of the medium-term lending facility (MLF) by 20 basis points to 2.3%, according to a statement on Thursday, the first reduction in almost a year. The cut followed the PBOC’s trim of the seven-day reserve repo rate by 10 basis points on Monday. The monetary authority has recently downplayed the MLF rate in favour of the short-term rate to guide markets in a way more similar to global peers.

“It is basically a coordinated effort across all the key interest rates to ease monetary policy,” said Lynn Song, the Greater China chief economist at ING Bank. “It’s worth highlighting this round of easing kicked off with the seven-day reserve repo rate, which may be a signal of its future role as the main policy rate.”

China’s bond futures edged higher with the yuan after the cut, though the moves were modest.

The PBOC’s string of rate cuts underscores authorities’ growing urgency to support growth, which came in worse than expected in the second quarter, as faltering consumer spending more than offset an export boom. The central bank had refrained from cutting rates since late last year, as it sought to keep the yuan exchange rate stable.

The announcement was unexpected because the PBOC typically conducts MLF operations in the middle of each month, and had already drained a net three billion yuan (RM1.93 billion) of cash via the funds earlier this month when a batch of them matured. The PBOC provided 200 billion yuan of MLF on Thursday, the biggest net injection since January.

PBOC’s shift

The sequence of the rate cuts and the off-schedule MLF operation underlines the PBOC’s transition towards a new framework.

Making the seven-day reverse repo the main policy lever that guides lending and longer-term rates could allow the PBOC to send out a clearer signal and better influence the market. Along with the new tool of government bond trading that has yet to be used, the shift could potentially give the central bank more sway over borrowing costs from short- to long-term durations.

Taken together, the rate cuts amount to a modest round of easing this time around, and are unlikely to move the needle in terms of boosting domestic demand, in the absence of any improvement in the overall jobs market, economists have said.

The cuts are “helpful, but the impact of interest-rate cuts will likely be more muted, given weak confidence and still entrenched expectations of house price declines”, said Michelle Lam, a Greater China economist at Societe Generale SA. “That is still insufficient to turn around people’s weak expectations for jobs and income.”

The MLF remains too high both in absolute terms and also relative to the seven-day reverse repo, as market rates have come down, and the spread between short- and longer-term borrowing costs narrowed, according to Lam.

Banks have had little appetite for the MLF funds in recent months, as a decline in market rates meant it became cheaper for them to borrow from each other than from the PBOC via the programme. A bigger cut in the MLF rate helps bring it closer to market borrowing costs.

The rate on one-year negotiable certificates of deposit issued by AAA-rated banks, a gauge of short-term interbank borrowing costs, is now 1.9%, cheaper than the MLF funds.

Managing liquidity

The surprise announcement also risks introducing more confusion over the schedule of the PBOC’s policy moves, as it is now unclear whether the MLF operations will take place on the 25th of each month instead of the 15th.

If that is the case, banks could find it harder to manage liquidity, as existing MLF funds would still mature around the 15th, the PBOC-managed Financial News said in a report on Thursday.

The latest cut came after China’s largest state banks lowered rates on some deposit products to ease pressure on profit margins, following their earlier cuts in the benchmark lending rates, known as the loan prime rates (LPRs).

Most economists narrowly predict that banks will cut their lending rates again in the fourth quarter, with the one-year LPR seen falling by 10 basis points or more, according to a Bloomberg survey.

In a separate statement, the PBOC disclosed that banks had taken up just 12 billion yuan of the 300 billion yuan quota for the affordable housing relending programme as of the end of June. It allows the central bank to provide cheap funding to lenders if they issue credit to help local governments buy unsold homes and convert them into subsidised housing.

That programme is a major part of a broad property rescue package unveiled in May, which has yet to have any material impact on reversing slumping home prices.

Uploaded by Tham Yek Lee

Source: TheEdge - 26 Jul 2024

More articles on CEO Morning Brief

JAKS Resources Inks Land Lease MOU With TDM Unit for LSS5 Project

Created by edgeinvest | Jul 26, 2024

Meta to be Hit With First EU Antitrust Fine for Linking Marketplace and Facebook — Reuters

Created by edgeinvest | Jul 26, 2024

Apple's China Market Share Shrinks as Huawei Surges, Data Shows

Created by edgeinvest | Jul 26, 2024

Insured Losses From CrowdStrike Outage Could Reach US$1.5b, CyberCube Says

Created by edgeinvest | Jul 26, 2024

Thailand Car Production Drops Sharply in June, Local Sales Fall

Created by edgeinvest | Jul 26, 2024

Hyundai Motor Posts Record 2Q Profit on Strong US Sales, to Boost Hybrid Lineups

Created by edgeinvest | Jul 26, 2024

UK Mortgage Rate Surge Pushed 320,000 Into Poverty, Report Shows

Created by edgeinvest | Jul 26, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

3

4

BFM Podcast

5

7

Good Articles to Share

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....