Wind Rider - Gainvestor

ARANK's A-RANKed Mission

Gainvestor

Publish date: Thu, 30 Mar 2017, 11:17 AM

Gainvestor

0 97

A wind rider who utilizes fundamental and technical analysis

You can click HERE to link to my blogspot. Thank you.

|

|

|

ARANK company in Selangor |

ARANK through his 100% owned subsidiary, Formosa Shyen Horng Metal SB, is principally involved in the manufacturing and marketing of aluminium billets which is the core business of the group. In 1998, Formosa had an installed capacity of 12,000 metric tonnes per annum of aluminium, now, as written in the latest Annual Report 2016, currently, the installed capacity had grown to 120,000 metric tonnes per annum. Being the largest manufacturer and supplier of aluminium billets, and one of the leading of suppliers of aluminium extrusion billets in Asia, the growth for ARANK in 19 years is 900%. From here, we can see that the demand of aluminium had skyrocketed in the past 20 years, and ARANK had been there, feeding and supplying the skyrocketing demand of aluminium in the industry.

But first, we need to understand how aluminium is produced. We can take a look at this youtube video[2]. To make it short, the raw material of aluminium is bauxite. Bayer process is a process to refine bauxite to produce alumina (aluminium oxide). There are only 30% - 54% of alumina in the bauxite[3]. And aluminium is extracted from the alumina by electrolysis, separating aluminium metal in the negative electrode and sink to the bottom of the tank, while oxygen at the positive electrode[4]. All of these processes involved massive machineries and facilities.

|

|

|

The center bottom, aluminium extrusions; the right is the aluminium billets. (Diameter ranging from 3 inches to 11 inches and longest length up to 6 meters) |

If you like my way of analysis and you haven't join me in my facebook, appreciate if you could like my FB page, https://www.facebook.com/gainvestor10sai/?fref=ts

Thank you^^

|

|

|

The process and machineries involved in aluminium |

ARANK had the integrated facilities, which include: Wagstaff "Airslip" billet casting mould system, melting furnaces with regenerating burners, tilting holding furnace and fully automated vertical direct chilled hydraulic-controlled casting systems from Australia, filters, in-line degassing machines, homogenising furnaces and cooling booths, and automated billet-sawing machines. ARANK achieved the ISO 9001:2008 certification, meaning to say they emphasize on the quality of its product. ARANK even had numerous testing equipment to inspect and evaluate on the quality in the casting and homogenising processes. The products are the aluminium billets, ranging in diameter from 3 inches to 11 inches and any cut length up to 6 meter.

ARANK's another subsidiary is HongLee Group (M) SB (55%). The principal activity is manufacturing and marketing of all types of aluminium and glass fittings and other related activities[5]. HongLee has 11 dealers over Malaysia, Singapore and Indonesia with 14 showrooms in total. They are determined towards continuously developing, expanding and improving our distribution networks. Their own in-house brands are "HongLee" and "Apresi", and products include Apresi Kitchen & storage solution, high performance folding & sliding door, high performance window, pergola & sun louvres, grille & fence and shower & insect screen. ARANK had disposed HongLee Group in January 2017.

ARANK currently exporting about 30% of its production. Its export markets include Africa, Europe, South Asia and South East Asia.

Why is aluminium important in our daily life. Below are some points[5]:

- Strong and durable providing a range of long lasting design options

- Corrosion resistant qualities and resistant to weathering under a range of harsh environmental conditions.

- Hassle-free maintenance – won't swell, crack, split or warp. Free from Termites infestion threat.

- Non-combustible material which is safe even in high temperature environment , does not burn or release toxic fumes.

- Environmentally sustainable material and infinitely recyclable.

- Aesthetic and uniform surface finish quality

1. Fundamental Analysis

|

|

|

Revenue and Net Profit from 2013 to 2017* |

ARANK's revenue had been steady since 2013. And for 2017, it will also be a steady year if ARANK continue to maintain the sales volume. As for net profit, ARANK recorded an improved +54% from RM10,316k to RM15,838k. In 2017, ARANK had only announced 2 quarters of financial result. ARANK managed to maintain the net profit margin by around 2 - 3%.

In the Annual Report 2016, Mr Chairman Dato’ Shahrir Bin Abdul Jalil mentioned about the risks or factors faced by ARANK, which were aluminium price, currencies and also natural gas pricing[1]. All of these are concerns faced in the year of 2016, however the company still able to curb the situation. As mentioned by the Managing Director, Mr Tan Wan Lay, ARANK was able to achieve the satisfactory results by improving the efficiency and recover by controlling the production overhead and transportation costs. The upgrades that had been done in 2016 was improving the homogenise furnaces to increase efficiency in the usage of electricity through the production process as well as an additional one unit of dust control system to ensure cleaner discharge into the environment.

Some background about Mr Tan Wan Lay. He had more than 20 years of experience in aluminium extrusion industry. He joined LBALUM and also PMETAL before setting up the Formosa Shyen Horng Metal which is also known as ARANK. Mr Tan had a wide knowledge and experience in the aluminium sector, which can be noticed from his past experiences. When we checked the top 30 shareholders list, LBALUM holds 1.5 Million shares, which is 1.25% of total shares. When we read through the QR or the AR, eventhough both of them are competitors, in terms of the business, they have close relationship with each other. ARANK sold their products to LBALUM and vice-versa. If your company's shares are bought by your competitor, i anticipate good things in it.

|

|

|

ARANK also sell their products to LBALUM |

When i check through the google map, both of the factories are actually near to each other, that's why they are able to purchase and sell their products to each other. Other investment firms which are holding ARANK are City Data Limited, Fairway Assets Investment Limited, Mablewood International Holding Limited, Mayer Capital Holding Ltd.

|

| Distance between LBALUM and ARANK factories in Googlemaps |

Q2 2017 Result

|

|

|

Quarterly Revenue and Net Profit[6] |

Revenue decreased -7% qoq and -11% yoy respectively while net profit decreased -19% qoq and +10% yoy respectively[6]. The reason for the decrease for revenue is due to lower business volume for Q2 despite the average selling prices were higher. A thing to note here, the average selling prices were higher which is related to global aluminium price. Do notice there is a similarity in the quarter results pattern. The net profit drops from Q1 to Q3 and spiked up in Q4, but if we compare yoy, it is always higher than previous years. The trend had been like that since 2014.

ARANK had disposed its entire 55% equity interest in its subsidiary, HongLee Group for a total cash of RM 2,105k. The announcement was made on 25 January 2017. HongLee had not being delivering satisfactory results, hence the management had decided to dispose it off for good. ARANK is a net cash company with its net cash per share of 0.09. In its prospect, the management is quite honest with the future prospect, underlying that the depreciating RM is good for exports and at the same time, it escalates the costs of doing business arising from costlier raw materials. The volatile aluminium price also adds uncertainty to the decision-making process. These are the risks currently faced by ARANK's management team. Hence, for us, retailers, we will need to monitor the global aluminium price and the forex of USD/RM.

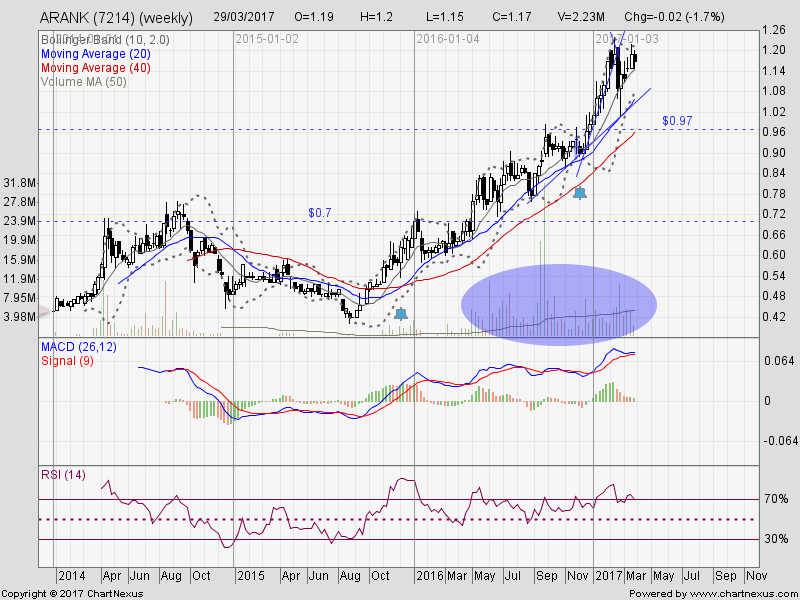

2. Technical Analysis

|

|

|

ARANK Weekly Chart from 2014 till 2017 |

Let's look at a bigger picture. Recently in the mid of 2016, volumes start to kick in. The reason is due to the rise in global aluminium price. Some investors had already seen the situation and started to accumulate aluminium counters for the past 1 year. Just now we mention about the Q4 result is always the highest for every year. The Q4 result for ARANK is from May to July, announced in the month of September. In 2014, share price spiked up a lot before September; in 2015, share price increased after September; for 2016, share price also went uptrend after September. And September 2017 will be very important.

|

|

|

ARANK Daily Chart |

ARANK had been in uptrend since December 2016. The SMA20 first cross over SMA40 in the month of October, then after that, it had been going sideways before spike up in January 2017. With the supports at 1.15 and 1.09, ARANK is poised to go sideway above 1.10. With the recent Q2 results being announced on 29 March 2017, ARANK might be going down tomorrow, after announcing a dull QR. The resistance will be in 1.24. Currently, ARANK is at the position of all time high, if they are able to break 1.24, then they will be ALL TIME HIGH.

|

| ARANK Daily Chart as of 10.35am 30 March 2017 |

Today (30 March 2017), ARANK gapped down with a high volume. I guess those who bought on the 1 March 2017 had already sold their ARANK shares due to less-excitement results. I make this assumption based on the volumes. Let's see how ARANK closes today. Hopefully to create a hammer with high volume.

3. Projection Analysis

Let's talk about some reasons why we should aim the commodities stocks, or in this case, it will be aluminium. These are all self-observed facts. Please judge and have your own individual thoughts also. I might be wrong.

A) Donald Trump: Make America Great Again

|

|

|

US President Donald Trump - Dont Play Play |

Still remember this guy? Yes, he is the US President Donald Trump. "Make America great again", the four words is enough to make the impact in the whole world. Donald Trump had an ambitious to-do list for the next four years: building stronger borders, keeping the country safe against terrorism, producing more jobs, repealing the Affordable Care Act, replacing it with something better, promoting excellence in engineering and science, investing in modern infrastructure[7].

When a country want to invest in modern infrastructure, what is required? You are right, they are steels and aluminiums. When we want to develop a country, equip the infrastructure, we need those materials in building our constructions, pilings, etc. Trump had repeatedly threatened to slap American manufacturers with a border tax if they move jobs and production out of the country and then sell goods back to the United States. With the fear of being charged with high border tax, i guess the companies will continue to set up their factories in US[8]. If DT stood firm by his vision, i believe some commodity price will be in high demand, and also the US economy will be good, and Dow Jones will be good, followed by our FBMKLCI will be good too. (haha, think too far)

B) Global Aluminium Price

|

|

|

Aluminium Price[9] |

The aluminium price had increased around 35% since finding its bottom around 1,420. After that, aluminium is in the uptrend and now ready to run over 2,000. The aluminium price went up after the month of January 2017. That is the time when Donald Trump became the US President. Is this coincidence or there's a logic behind? For me, i believe since the share price went up 35%, there must be a valid reason for it. And i think it's related to DT's Make America great again legacy. The demand for aluminium will still be high in the coming months and years.

ARANK's 34% of its revenue is derived from the sales from foreign countries such as South East Asia, Europe and South Asia. But one thing to note from here. The gradual increase of aluminium price is good for ARANK. Imagine now ARANK sold the same quantity of aluminium, the selling price will be higher if compare to previous 6 months. This is also aligned to what we saw in the Q2, 2017. The management mentioned about the higher selling price. But we also need to remember that the volatility of aluminium price will add uncertainty to the management's decision making. But in the future, if aluminium price continues to go up, and ARANK be able to achieve higher sales, things are bright for them.

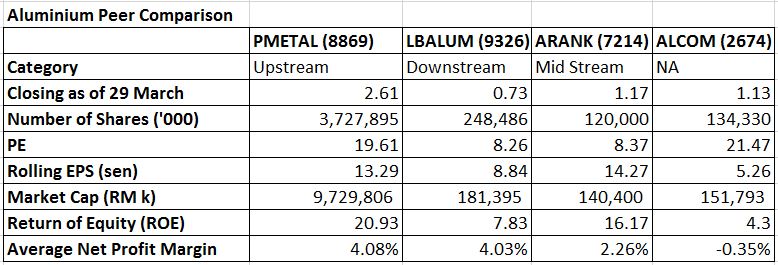

C) Peer Comparison

A simple peer comparison is done among its competitor. I am going to compare against PMETAL, LBALUM and also ALCOM.

|

| Aluminium Peer Comparison |

PMETAL is the dragonhead for the aluminium counters. It got the highest market capitalization, which is around RM 10B. PMETAL had currently expanded to China and are looking to kick start its phase 3 in Samalaju, Sarawak. PMETAL is categorized as upstream, ARANK as mid stream and LBALUM as downstream, (from what i read in The Edge Weekly). LBALUM seems lagging behind in terms of the price, with the PE of 8. The reason why i look into ARANK is because of its high EPS and also high ROE. ROE is one of the most important element to me, because it translates the efficiency of the management in generating more profit with the money shareholders have invested. If compared to the average net profit margin for the recent 3 full years, PMETAL and LBALUM both score the highest scores.

|

|

|

PMETAL Daily Chart |

|

|

|

LBALUM Daily Chart |

|

|

|

ALCOM Daily Chart |

As we can see from PMETAL, LBALUM and ALCOM's chart, similarly to ARANK, the share price gained momentum after the election of Donald Trump as US President, which is aligned with the global aluminium price. Since PMETAL is the dragon head, its movements might also elevate or drag down the share prices for other aluminium counters.

Of course, we might also need to monitor:

1. Global aluminium price - the higher the better, however it will be an obstacle for the management to make some critical decision

2. USD/MYR - maintain as it is, the higher it goes, the higher the processing cost however, benefit from forex gain

3. Donald Trump - Make America Great Again, more and more facilities will be built in US

4. PMETAL - If the dragonhead continues to perform better, then the the rest should follow, and not to forget about ARANK.

5. The QR of ARANK - Q1, Q2, Q3 is lower but will spike up in Q4, will the trend continues? If it continues, we can expect the share price to break new high also

Summary:

Can ARANK accomplished his mission? Or if the share price continue to drop, you can just wake me up when September ends...

- ARANK just released its Q2 2017 result, not an exciting result due to the lower sales volume, however the average selling price is higher due to the increment in the global aluminium price.

- The management had taken firm steps by improving the plant operation's efficiency as well as disposing the loss-making HongLee Group and expected to gain RM2 Mil from its disposal.

- Aluminium together with steel are the most important commodities for the country's development and building infrastructure.

- Net cash per share of 0.09

- The management had taken prudent action by upgrading the plant facilities as well as dispose off its subsidiary HongLee at RM2 Mil.

- If we observe the trend, the Q1, Q2 and Q3's net profit will be dropping, spiking up in Q4. The yoy net profits are better than previous years.

- The current support for ARANK is 1.09 with the resistance of 1.24.

- With the current PE of around 8 with high EPS and ROE if compared with its peers PMETAL, ALCOM and LBALUM.

- If we annualized the EPS and take the average PE among aluminium counters, the TP for ARANK is 2.00

- A few things to take note, global aluminium price, USD/MYR, US Donald Trump's policy, PMETAL's movement and also the QR for ARANK.

- **The share price gapped down today with high volume. This is not a plesant sign. However, please conduct your own studies before making any decision.

If you like my way of analysis and you haven't join me in my facebook, appreciate if you could like my FB page, https://www.facebook.com/gainvestor10sai/?fref=ts

Thank you^^

Let's Ride the Wind and Gainvest

Gainvestor 10sai

30 March 2017

11.15am

Sources:

[1]: Annual Report 2016: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5255449

[2]: How Aluminium is Made: https://www.youtube.com/watch?v=fa6KEwWY9HU&t=1s

[3]: https://en.wikipedia.org/wiki/Bayer_process

[4]: http://www.bbc.co.uk/schools/gcsebitesize/science/add_ocr_pre_2011/chemicals/extractionmetalsrev3.shtml

[5]: http://www.honglee.my/about.html

[6]: http://www.bursamalaysia.com/market/listed-companies/company-announcements/5379317

[7]: https://www.washingtonpost.com/politics/how-donald-trump-came-up-with-make-america-great-again/2017/01/17/fb6acf5e-dbf7-11e6-ad42-f3375f271c9c_story.html

[8]: http://www.independent.co.uk/news/world/americas/donald-trump-threatens-toyota-got-facts-wrong-a7513061.html

[9]: https://www.investing.com/commodities/aluminum-advanced-chart

More articles on Wind Rider - Gainvestor

How Retailers can Perform Analysis: Plastic Packaging and Commodity (Steel & Aluminium)

Created by Gainvestor | Aug 10, 2017

Featured Posts

Latest Videos

Apps

Top Articles

1

CEO Morning Brief

2

CEO Morning Brief

3

4

Good Articles to Share

US Army veteran plows truck into New Orleans crowd - Five stories you need to know | Reuters

5

Good Articles to Share

‘THINGS ARE GETTING WORSE’: Credit card debt skyrocketing to concerning levels #shorts

6

Good Articles to Share

Apple offers iPhone discounts in China as competition intensifies | REUTERS

7

Good Articles to Share

New Orleans, Tesla truck explosion, Gazprom and the debt ceiling

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

Jon Choivo

Few things, higher aluminium price results in higher input cost. So the net effect is that they balance off.

2017-03-30 13:11