Hidden Gem in Malaysia Stock Exchange

Sunway Berhad - Deeply Undervalued, Reasonable Dividends, High Net Assets, Strong Free Cash Flow....

(The information from various research reports is used.)

Sunway Berhad is noted for its superior and unrivalled 'build-own-operate' model. I set a target price of RM3.91 (PE 12 of FY16 EPS RM0.326, with the last traded RM2.94, potential upside is 33%). For FY16, Sunway sets target property launches of RM1.6b. Property launches of Sunway is well spread scross multiple areas namely Sunway Iskandar, Ipoh, Mont Kiara, Bangi, South Quay, and Jalan Peel. Management is confident hitting the expected sales target of RM1b for FY15 because their 9MFY15 sales already hit RM734m (effective RM564m). Don't forget it has the steady dividend income from 34.5% stake Sunway Reit and earnings from 51% stake Sunway Construction.

The RNAV of Sunway is very impressive. RNAV breaks down as below:

Property Development (Malaysia):

- Sunway South Quay

- Sunway Velocity

- Sunway Damansara

- Medini Iskandar

- Daiwa JV

- Pendas, Iskandar

- Sunway Lenang

- Sunway Wellesley

- Paya Terubong

- Sunway Hillds

- Balik Pulau

- Sunway Cassia

- Sunway Semenyih

- Kelana Jaya Land

- Total worth RM6.8b

Property Development (Singapore)

- Miltonia Residences

- Arc, Tampines

- Lake Vista

- Sea Esta

- Royale Square

- Mount Sophia

- Avant Parc

- Total Worth RM315.9m

Property Development (Others)

- Tianjin Eco City

- Sunway Guanghao (China)

- Sunway OPUS Grand India

- Sunway MAK Signature Residence (India)

- Total Worth RM266.5m

Investment Property

- Monash University

- Sunway Pinnacle

- Sunway Velocity Shopping Mall

- Sunway University Campus

- Monash Residence Hostel

- Total Worth RM1.3b

Other than the above:

- 34.5% stake in listed Sunway REIT RM1.5b

- 51% stake in listed Sunway Construction RM923m

- Sale of 70% stake in 13 acres land to Daiwa RM24.7m

- Trading & Manufacturing Asset RM415.1m

- Quarry Division Asset RM165.9m

- Other Division Asset RM1.1b

Review and Outlook of Business Performance:

After excluding RM13.7m exceptional items, its 3QFY15 core PATAMI increased by 10% QoQ to RM147m (9MFY15 core net profit of RM414.5m, growth of 7.5%, met expectation) mainly due to improved performance from many business segments and lower minority interest contribution -38%. 3QFY15 core EBIT margin was stable at 14.4%, compared to 14.3% in 2QFY15 and 13.9% in 3QFY14. For 9MFY15, property sales was RM734m while its unbilled sales stood at RM2.3b (effective RM1.7b, 1.4x of FY14 property development revenue, providing at least 2 years of visibility).

The improvements in earnings (9MFY15) were mainly driven by

- stronger operating profit in most of its divisions (construction +69%, property investment +44%, quarry +66%; due to improvements in margins)

- property investment emerged as the largest EBIT contributor at RM40m, accounting for 33% of 3QFY15 EBIT given the higher contribution from Sunway University New Academic Block and Sunway Pinnacle.

- the 51% stake construction division was exceptionally strong, with EBIT being boosted mainly by a reversal of over-elimination of intra-group profit in the previous quarter.

- the Emerald Residence and Emerald Boulevard shops have recorded booking rate of 50% and 60% respectively (previewed 25 Nov at Sunway Iskandar), which is satisfactory in this challenging environment.

- reduction in net interest cost (-79%)

- lower minority interest contrition (-20%)

51% stake of Suncon was successfully listed on July 15. As at 3QFY15, the outstanding order book stands at RM4.3b (vs RM2.69b as at June 15), implying a healthy cover ratio of 2.4x on FY14 revenue. The recent RM120m worth of building construction contract win has lifted YTD job wins to stand at RM2.6b (+136% YoY, from RM1.1b in 2014), surpassing management's target of RM2.5b by 4%. Given its strong track record, Suncon should be a main beneficiary of upcoming tenders for LRT, MRT and BRT (another reason is government institutions are substantial shareholders of Sunway as well).

Aggressive Share Buy back by Company:

As you could read, it bought back 1.17% of issued shares!

Consistent Cash Dividends Payout:

Dividends of RM0.11, dividend yield of 3.7%.

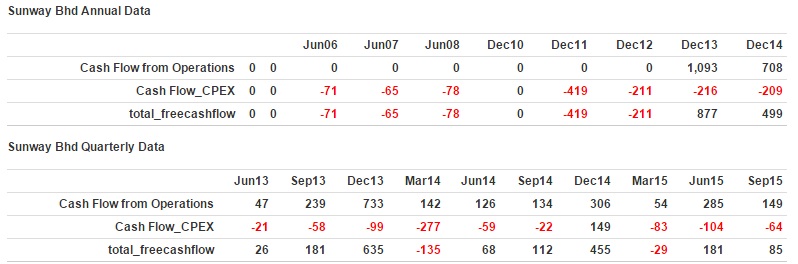

Superior Free Cash Flow:

Even in this challenging environment, it still maintain strong FCF.

Low price-to-book ratio:

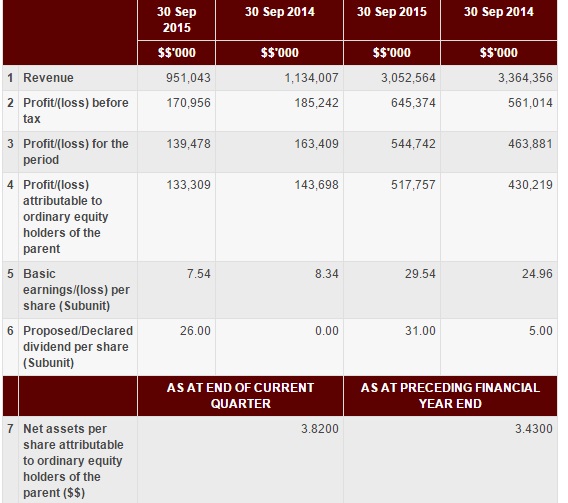

NAV is RM3.82, price-to-book ratio of 0.77!

Aggressive director share buy back since 1 December 2014:

The insiders keep buying Sunway shares.... could it be clearer than this?

Amanah Saham Bumiputera and EPF keep acquiring...

High Return of Tangible Equity (ROTE)

Average annual ROTE is 15.1%!

Based on the annual report 2014, some of the substantial shareholders are:

- Skim Amanah Saham Bumiputera 4.92%

- Employees Provident Fund Board 3.87%

- Amanah Saham Malaysia 1.75%

- Eastspring Investments Berhad 1.28%

- AIA Berhad 1.28%

- Amanah Saham Wawasan 2020 1.23%

- Great Eastern Life Assurance Berhad 0.91%

- J.P. Morgan Bank Luxembourg S.A. 0.78%

- Demensional Emerging Markets Value Fund 0.77%

- Amanahraya Trustees Berhad - As 1Malaysia 0.75%

- Public Islamic Select Treasures Fund 0.6%

- Public Islamic Select Enterprises Fund 0.47%

- Amanah Saham Didik 0.46%

- VCAM Equity FD 0.37%

- Citibank New York 0.34%

- The Bank of New York Mellon 0.32%

- UBS AG 0.32%

- CBNY Emerging Market Core Equity 0.31%

- Amanah Saham Nasional 3 Imbang 0.29%

- Amanah Saham Nasional 2 0.28%

- JPMorgan Chase Bank, National Association (USA) 0.42%

Hope you enjoy reading!

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-06-26

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-25

SUNWAY2024-06-24

SUNWAY2024-06-24

SUNWAY2024-06-24

SUNWAY2024-06-24

SUNWAY2024-06-21

SUNWAY2024-06-20

SUNWAYMore articles on Hidden Gem in Malaysia Stock Exchange

JAKS RESOURCES: 25 years recurring income, order book RM2.5bn, FY2019 revenue RM1.1bn

Created by James Ng | Oct 02, 2017

Chin Well Holdings berhad - Superior Free Cash Flow, Minimal Capex, Net Cash, Good Dividend...

Created by James Ng | Mar 10, 2016

Pantech Group Holdings Berhad - Earnings Accelerating, Large PVF Tendered, New Hot-Dip Factory...

Created by James Ng | Feb 08, 2016

Discussions

Be the first to like this. Showing 6 of 6 comments

shortinvestor77: I meant Sunway is a good company, and I seriously recommend it.

2016-02-18 08:25

Post a Comment

Featured Posts

New Update. Discover investment communities that resonate with your ideas

MQ Trading Signals

Time

Signal

Duration

Type

2024-06-26 16:00:00

ADX

10 Mins

SELL

2024-06-26 16:00:00

EMA 5

5 Mins

SELL

2024-06-26 14:50:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-06-26 14:50:00

TURTLE SYSTEM 55

5 Mins

SELL

2024-06-26 14:35:00

TURTLE SYSTEM 20

5 Mins

BUY

Apps

Top Articles

4

5

save malaysia!

Putrajaya reviewing need to slash RON95 subsidy, says Rafizi

6

save malaysia!

7

save malaysia!

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

JT Yeo

A thing about the Sunway FCF. Large portion of capital expenditure for property companies doesn't come from acquiring property, plant & equipment but comes from buying lands. A manufacturing buy more machines to produce more products; a property needs to constantly buy more lands to sell more house (products).

Therefore the FCF is normally 'overstated' as it doesnt include money spent acquiring lands for development purposes.

2016-02-07 21:53