HLBank Research Highlights

Rohas Tecnic Bhd - Anticipate a strong FY17-20 EPS CAGR of 21%; Potential downtrend reversal amid hammer pattern

As the existing core business are not affected by change in government, we believe ROHAS’s rout (-24% YTD and 28% off historical peak on 9 Jan) as overdone. Besides, values emerge amid undemanding 9.6x FY19 P/E (26% lower than 1Y historical P/E of 13x), supported by a strong EPCC orderbook of RM680m and 21% EPS CAGR for FY17-20, riding on the tower boom and infrastructure heat in the ASEAN region. Potential downtrend reversal amid hammer formation.

50% of orderbook replenishment target in hand. Rohas’ recent 2nd EPCC job win of RM38m on 9 July brought the YTD sum to ~RM290m and a total EPCC orderbook of ~RM680m (translated to a healthy cover of 5.2x on FY17 EPCC revenue). This is expected to provide a strong boost to Rohas' earnings growth for the next two years. The company is targeting for orderbook replenishment of RM500m this year with bulk of the new jobs from Bangladesh as HGPT is one of the top three EPCC companies in the country's power transmission sector.

Opportunities mushrooming within ASEAN region. We like Rohas for its exposure to ASEAN, which is one of the fastest growing economic regions in the world. Infrastructure investment needs are expected to be robust in the foreseeable future and this will generate steady demand for its products. HLIB institutional research pegged a RM1.74 TP, providing another 46% upside.

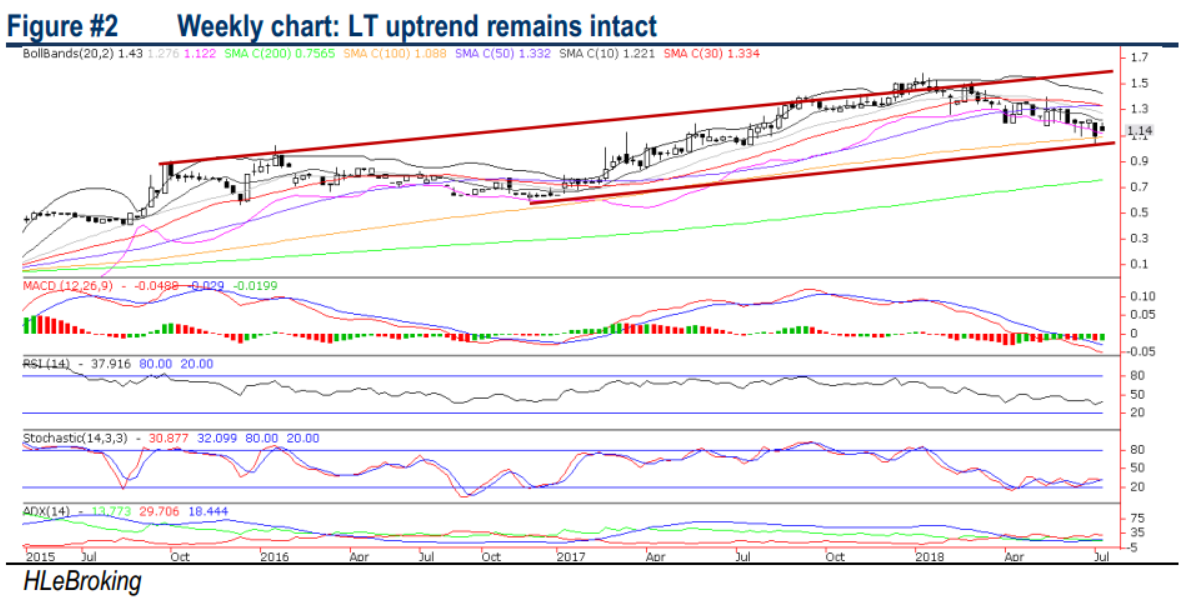

Potential downtrend reversal amid hammer pattern. After a 41% slump in share prices from historical high of RM1.58 (9 Jan) to a low of RM1.02 (6 July), ROHAS has formed a hammer pattern on 6 July before closing at RM1.14 on 13 July. We see limited downside risks with a floor near RM1.09 (100W-SMA) and RM1.03 (weekly support trendline), supported by bottoming up indicators and its strong fundamental prospects. On the flip side, a successful breakout above RM1.21 (downtrend resistance) will spur prices higher towards RM1.30 (50% FR) before reaching our LT target at RM1.45 (76.4% FR). Cut loss at RM1.02.

Source: Hong Leong Investment Bank Research - 16 Jul 2018

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-30 09:50:00

EMA 5

5 Mins

SELL

2024-07-30 09:40:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-30 09:35:00

EMA 5

5 Mins

BUY

2024-07-30 09:30:00

TURTLE SYSTEM 20

5 Mins

BUY

Apps

Top Articles

1

save malaysia!

DAP urges calm over school charity concert sponsorship issue

2

Good Articles to Share

3

4

5

6

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

7

MQ Market Updates

8

TA Sector Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....