HLBank Research Highlights

Naim Holdings - A Good Proxy for the Sarawak Infrastructure Play

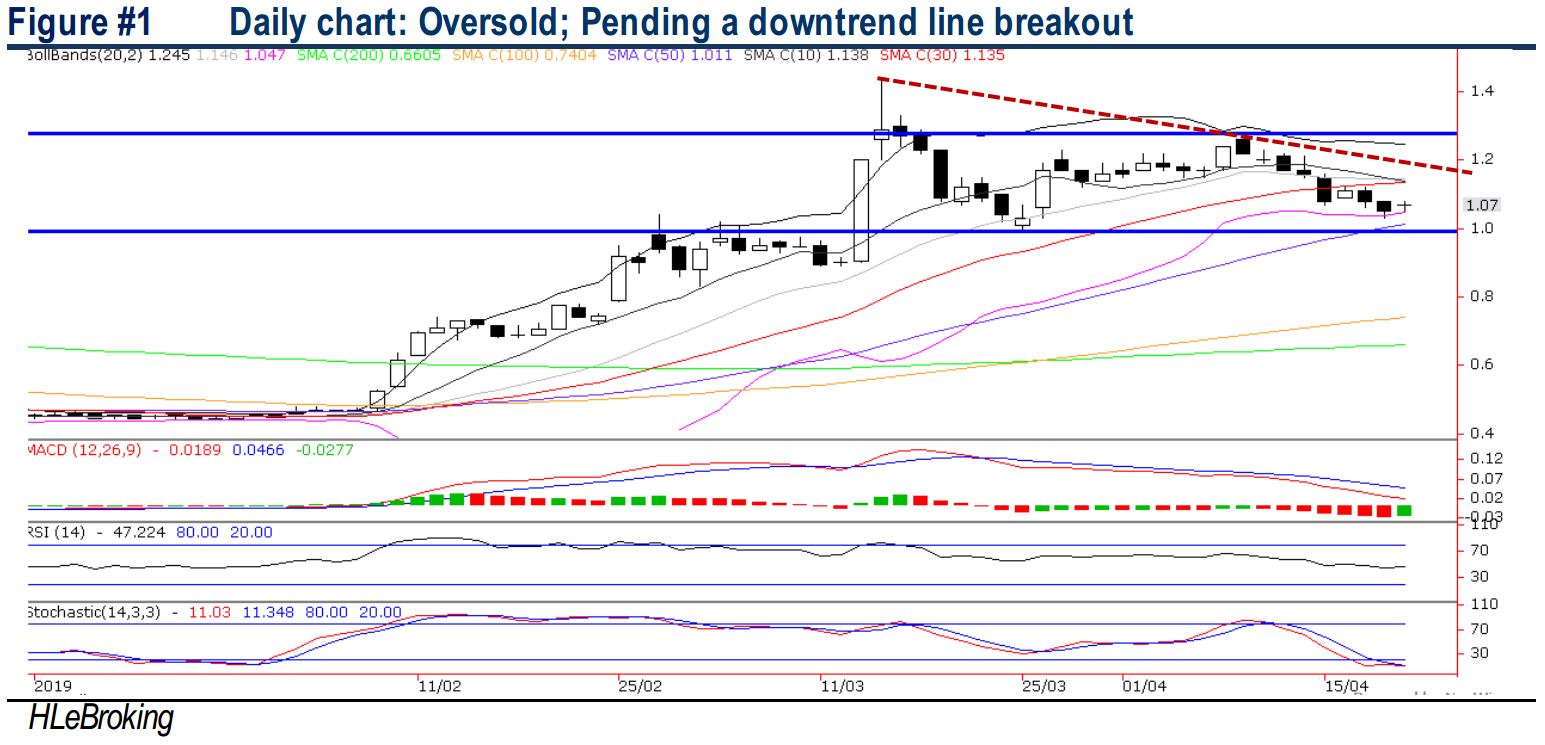

NAIM’s share price has rallied by 140% YTD, mirroring the 148% surge of its 26%-owned associate, Dayang. Notwithstanding the huge rally, NAIM’s share price is still undervalued as we opine that investors have yet to fully appreciate the embedded values of its construction and property businesses. Indeed, adjusted for its stake in DAYANG (RM336m market cap), the current implied value of RM214m market cap (Naim’s market cap of RM550m-RM336m) on its core businesses is only 5.4x P/E against its Sarawak’s peers of 9-10x! Given its robust construction orderbook of RM1.9bn, positive prospects of Dayang and resilient earnings from its property division (despite the challenging outlook) coupled with the expectations of more pump-priming activities before Sept 2021 state election, market could assign a higher rating on NAIM. Currently, the stock is trading at 0.43x P/B, 63% lower against its Sarawak’s peers. Technically, the stock is poised for a downtrend line breakout above RM1.18 to advance further towards RM1.28 levels.

Signs of revival. Sentiment on the domestic construction industry has been boosted by positive newsflow such as (i) resumption of ECRL project; (ii) revival of 121 infrastructure projects (RM13.9bn) offered through direct negotiations and limited tenders by the previous government after cost review; (iii) potential revival of HSR and (iv) approval of high-impact projects under mid-term review of 11th Malaysia Plan such as Kulim airport (RM1.6bn), logistics and manufacturing hub in Sidam (RM300m) and construction of Phase 1A and 1B of the Northern Corridor Expressway (RM1.7bn). Although we do not expect the domestic construction industry prospects to go back to where it was during the period of pre-GE14, we opine that the worst is over for the industry.

NAIM - proxy to Sarawak’s stimulus measures, backed by a RM1.9bn sizeable orderbook (~4.8x FY18 construction revenue). To recap, the state government has allocated c.RM9bn for development expenditure under state budget 2019 which is the biggest in the history of the state. Funding for those projects is expected to come from Sarawak’s state reserves (c.RM31bn) which may insulate the projects from risk of reduction of federal government spending. In early April, Opus was appointed as the project management consultant for the coastal road and second trunk road projects, indicating that these jobs are on the verge of rolling out. The momentum of project flows in Sarawak should also gain traction as the next state elections must be held before Sept 2021. Currently, NAIM has a sizeable construction order book of c.RM1.9bn and is slated to win more projects in future based on its track record in various notable projects such as Sabah O&G Terminal, MRT Lembah Kalang/Sg Buloh-Kajang, Pan Borneo Highway etc.

NAIM has sizeable development land banks in Sarawak with low holding cost, mostly located in critically masses population areas like Kuching and Miri. Currently, the group has three flagship mixed development projects in Sarawak, namely Kuching paragon, Bintulu Paragon and Bandar Baru Permyjaya, Miri (developing on a total ~730 acres site). In addtion to the above, Naim has other land banks totaling ~1800 acres located in Bintulu, Kuching and Miri for future development.

Kuching Paragon (covering approx. 33 acres, with indicative GDV of RM1.5bn, lasting for 15 years) is a new landmark which introduces multifaceted lifestyle experiences integrating residential, business, retail and hospitality components . The group has commenced the 1st residential development, known as Sapphire On The Park (comprising 427 units in three high-end condominium towers) with total GDV ~RM310m. The 1st tower, Sapphire Classic with an estimated RM120m was recently completed. The remaining two towers are slated to be completed by 1Q2021.

Bintulu Paragon is an integrated development on a 36-acres land in the heart of Bintulu Town (to be developed in 2 phases), with a total indicative GDV of ~RM2.3bn (lasting for 15 years). The group has completed a RM300m Streetmall and SOVO units while the Peak, with 261 units of condominiums totalling to RM150m of GDV is expected to be completed by 2Q19.

Bandar Baru Permyjaya in Miri (BPP) is a self-contained township developed on a 3300 acres site (indicative GDV of RM5bn), located close to Miri’s central business district. Since launching in 1995 with over 9,000 properties delivered valued at ~RM2.2bn. Currently, its active ongoing project comparises a 450-acre Southlake project valued at RM1bn GDV. To date, the group has launched a 416 units (RM180m GDV) of residential properties scheduled to be completed by 2020. With a remaining 660 acres of land available for development, which may to last for another 15 years.

The unnoticed (ex O&G) earnings growth potentials from core property and constructions segments. Valuations are undemanding at 8.5x FY18 P/E (25% below peers) and 0.43x P/B (62% below peers) and trading at 57% to its adjusted BVPS of about RM2.50 (adjusted 3 for 2 rights issue at RM0.45 completed in Jan 2019). Based on Dayang’s market cap of RM1.29bn, NAIM's 26% associate stake of RM336m already accounted ~61% of its entire NAIM’s RM550m market cap, implying that the market was pricing its embedded property and construction earnings only at 5.4x P/E (vs peers’ 9-10x) based on FY18 PBT of ~RM40m. To recap, the property and construction divisions contributed about 51% (~RM40m) to FY18 PBT whilst the rest 49% (~RM38m) was contributed by Dayang. Given its robust construction orderbook, positive outlook of Dayang and resilient earnings from its property division, supported by the state’s buoyant economy and expectations of more pump-priming activities before Sept 2021 state election, market could assign a higher rating on its property & construction businesses.

Pending a downtrend line breakout to advance towards RM1.18-1.28. In the short term, NAIM could still engage in a consolidation mode as share prices continue to hover below immediate 10D & 30D SMAs at RM1.13. Nevertheless, downside risk is limited amid grossly oversold indicators. Once this pattern ends, we expect prices to stage a breakout above RM1.18 (downtrend line) to advance further towards our LT objective at RM1.28 (9 April high). Key supports are RM1.04 (lower Bollinger band) and RM0.995 (25 march low). Cut loss at RM0.97.

Source: Hong Leong Investment Bank Research - 22 Apr 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-29 14:30:00

TURTLE SYSTEM 20

10 Mins

SELL

2024-07-29 14:30:00

TURTLE SYSTEM 55

10 Mins

SELL

2024-07-29 14:30:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-29 14:30:00

TURTLE SYSTEM 55

5 Mins

SELL

2024-07-29 11:20:00

TURTLE SYSTEM 55

10 Mins

BUY

Apps

Top Articles

1

南洋 - 凭单专栏/温世麟

2

TA Sector Research

3

TA Sector Research

4

PublicInvest Research

5

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

6

7

M+ Online Research Articles

8

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....