HLBank Research Highlights

WTI - Downside bias ahead of the OPEC meeting (25-26 June) and G20 summit (28-29 June)

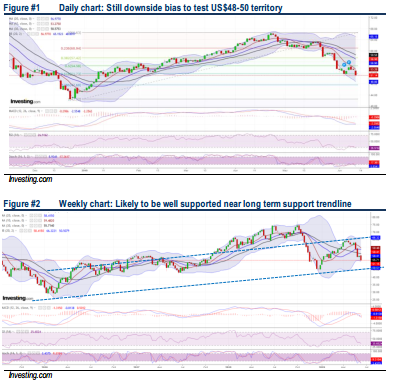

WTI sank 4% to a 5M low at US$51.1 (-23.3% from YTD high of US$66.6 on 23 Apr) after U.S. crude stockpiles jumped for the 2nd week in a row, as the market continues to grapple with concerns about weakening fuel demand due to the escalating US-China trade war. The US commercial crude inventories rose by 2.2m/barrels in the week through 7 June (consensus: -480k barrels), according to the U.S. Energy Information Administration (EIA). Technically, WTI further selldown towards US$48-50 levels unless prices can swiftly reclaim above the US$53-54 trajectory.

US commercial crude inventories increased. Crude inventories rose by 2.2m/barrels in the week through 7 June (consensus: -480k barrels), according to the U.S. Energy Information Administration (EIA). The primary concerns are increasing crude supplies from U.S. and the U.S.-China trade dispute may lead to decelerating global growth and weigh on oil demand.

Choppiness prevails with key supports at US$48-50 levels. Following the 57% rally from Dec low of US42.4 (24 Dec) to a high of US$66.6, WTI has fallen 23% to end at US$51.2 yesterday. We see further near term downward consolidation amid negative technical and prices are hovering below 10D/20D/30D SMAs with key supports at US$48-50. More solid support is the long term support trend line at US$46. Stiff resistances are pegged at US$53.3-55 levels.

Source: Hong Leong Investment Bank Research - 13 Jun 2019

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

2

4

南洋 - 凭单专栏/温世麟

5

TA Sector Research

6

TA Sector Research

7

Good Articles to Share

Democrats might put ‘someone else’ in Kamala Harris’ place, GOP sen warns #shorts

8

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....