HLBank Research Highlights

Pecca Group - A Record Year in the Making

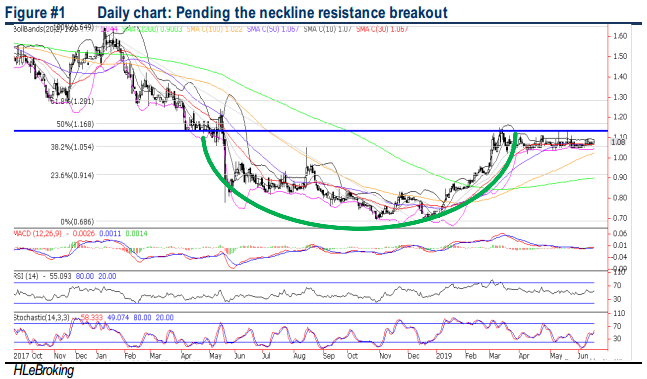

Pecca’s share prices rallied 47% YTD following a 65% surge in 9MFY19 earnings to RM13.8m, mainly attributed to higher sales volume and improved operational scale. HLIB maintains a BUY rating with a RM1.40 TP (+29.6% upside) based on 13x P/E on FY20 EPS, given its strong operational cash flow of RM17-25m per annum (FY19-21) with current net cash position of 51sen per share. Valuation is undemanding a 10.5x FY20E (35% lower than average 16.2x P/E since listed), supported attractive DY of 5.6-7.4% for FY19-21. Technically, the rounding bottom pattern signals potential long term downtrend reversal pattern, with upside targets at RM1.13-1.28 levels.

Decent earnings and net cash position. 9MFY19 earnings to RM13.8m, mainly attributed to higher sales volume (driven by higher Perodua demand) and improved operational scale. HLIB maintains a BUY rating with a RM1.40 TP (+29.6% upside) based on 13x P/E on FY20 EPS, given its strong operational cash flow of RM17-25m per annum (FY19-21) with current net cash position of RM94.0m (51sen/share).

Rounding bottom pattern signals potential cup and handle reversal pattern. The rounding bottom is a long-term reversal pattern, representing a long consolidation period that turns from a bearish bias to a bullish bias. After an extended sideways consolidation, PECCA is ripe for a neckline resistance breakout above RM1.13, supported by bottoming up indicators. A decisive close above RM1.13 will spur prices higher towards RM1.17 (50% FR) before reaching our LT objective at RM1.28 (61.8% FR). Key supports are situated at RM1.00-1.04. Cut loss at RM0.99.

Source: Hong Leong Investment Bank Research - 21 Jun 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-29 16:40:00

ADX

10 Mins

SELL

2024-07-29 16:30:00

EMA 5

30 Mins

SELL

2024-07-29 16:30:00

MACD/RSI

30 Mins

SELL

2024-07-29 16:05:00

EMA 5

5 Mins

SELL

2024-07-29 16:00:00

EMA 5

10 Mins

SELL

Apps

Top Articles

1

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

2

4

南洋 - 凭单专栏/温世麟

5

TA Sector Research

6

TA Sector Research

7

Good Articles to Share

Democrats might put ‘someone else’ in Kamala Harris’ place, GOP sen warns #shorts

8

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....