HLBank Research Highlights

LII Hen Industries - Solid Fundamentals and Balance Sheet

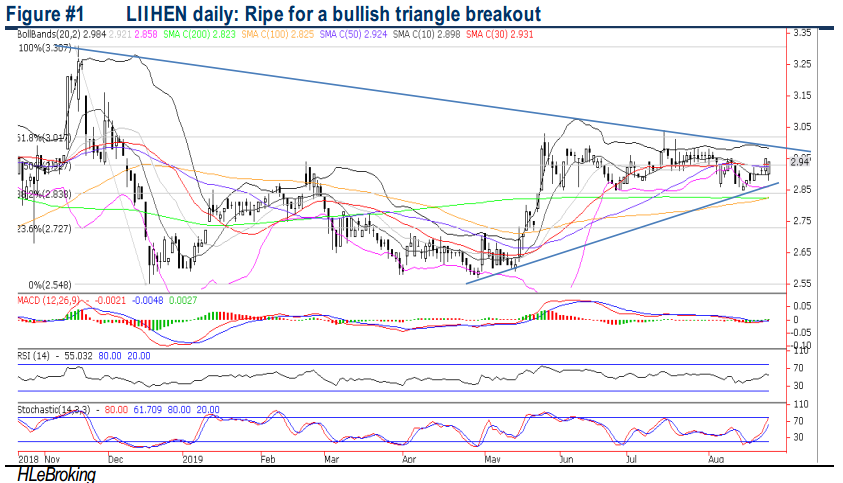

Apart from the weak ringgit climate, we like LIIHEN for its healthy dividend yield (5.6% for FY19-21) and current net cash/share of 54.8 sen or 18.6% to share price as well as cheap valuation of 6.9x FY20 P/E (Ex-cash PE of 5.6x). Moreover, bright outlook in the global furniture market (Global Furniture industry expects a 5.2% CAGR for 2019-2023) and its fruitful diversification to upholstery products as well as growing trade diversion from unresolved US China trade war should enhance stable earnings growth. Technically, the stock is ripe for a triangle breakout soon to lift prices higher towards RM3.13-3.31 levels.

Ripe for a bullish triangle breakout. LIIHEN has been trading in range bound mode within 3.04 (15 July high) and RM2.85 (26 June low) band in the last three months. In our view, the stock is poised for a triangle breakout soon, with share prices closed above key SMAs and supported by upticks in technical indicators. A successful breakout above RM2.96 (downtrend line) will push share prices towards RM3.04 and RM3.13 (76.4% FR) barriers before reaching our LT objective of 52W high at RM3.31 (21 Nov 2018). Key supports are RM2.85 and RM2.80. Cut loss at RM2.78.RM2.99.

Source: Hong Leong Investment Bank Research - 27 Aug 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-29 15:00:00

EMA 5

10 Mins

SELL

2024-07-29 14:55:00

EMA 5

5 Mins

SELL

2024-07-29 14:55:00

ADX

5 Mins

SELL

2024-07-29 14:55:00

TURTLE SYSTEM 20

5 Mins

SELL

2024-07-29 14:50:00

ADX

10 Mins

SELL

Apps

Top Articles

1

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

2

4

南洋 - 凭单专栏/温世麟

5

TA Sector Research

6

TA Sector Research

7

Good Articles to Share

Democrats might put ‘someone else’ in Kamala Harris’ place, GOP sen warns #shorts

8

PublicInvest Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....