HLBank Research Highlights

Alliance Bank - Ripe for a Technical Rebound Amid Compelling Valuations and Attractive Dividend Yields

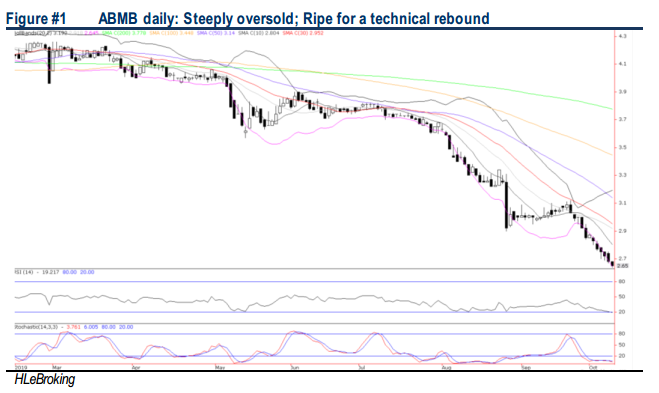

With share price corrected 34% YTD (the worst performer amongst peers) and 39% from 52W high, we are cautiously positive on ABMB, viewing this as an opportune time to accumulate on weakness amid recent selloff primarily due to the concern of 3 problematic loan accounts (which management shared that those were fully provided for and recovery plans are ongoing). Overall, the selling was overdone, reflected by its undemanding valuations at 7.7x FY21 P/E (33% below peers and 13% below 5Y historical mean) and 0.72x P/B (39% below peers and 13% below 5Y historical average), supported by an attractive DY of 6.2% (16% higher than peers). Technically, the stock is ripe for a relief rebound towards RM2.80-3.07 in the mid to long term, as it is at the tail-end of current downcycle from all-time high of RM5.50.

Ripe for a techical rebound. ABMB technical readings are steeply oversold after plunging 39% to RM2.65 from a 52W high at RM4.35 (4 Feb). On a long term monthly chart, the stock is likely at the tail-end of current down cycle (from all-time high of RM5.50 in July 2013), supported by the steeply oversold techncial readings (lower than the global financial crisis). In our view, the stock could trend sideways in the near term to build a base with key supports at RM2.50-2.60 levels before staging a long overdue technical rebound. A decisive breakout above RM2.80 (10D SMA) will spur prices higher towards RM2.95 (30D SMA) before reaching our LT objective at RM3.07 (21 Jan 2016 low). Cut loss at RM2.46.

Source: Hong Leong Investment Bank Research - 10 Oct 2019

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-07-29 16:40:00

EMA 5

10 Mins

SELL

2024-07-29 16:40:00

EMA 5

5 Mins

SELL

2024-07-29 16:30:00

TURTLE SYSTEM 20

30 Mins

SELL

2024-07-29 16:30:00

TURTLE SYSTEM 55

30 Mins

SELL

2024-07-29 16:30:00

TURTLE SYSTEM 20

5 Mins

SELL

Apps

Top Articles

1

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

3

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

4

Good Articles to Share

5

南洋 - 凭单专栏/温世麟

6

Good Articles to Share

Democrats might put ‘someone else’ in Kamala Harris’ place, GOP sen warns #shorts

7

8

TA Sector Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....