HLBank Research Highlights

Telekom Malaysia - A Prime Beneficiary of 5G Rollout

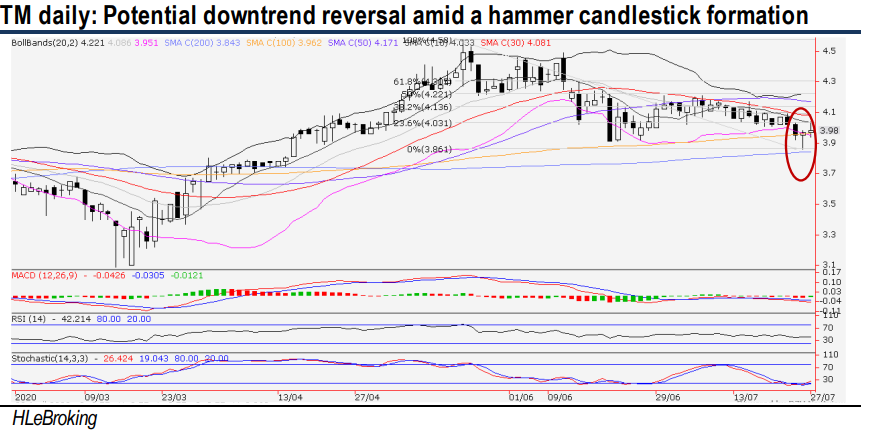

Anticipate a steady 9% EPS CAGR growth for FY20-22. HLIB Research maintains a BUY rating with a DCF-derived fair value of RM5.17 (+29.9% upside), supported by an undemanding 17.5x FY21 PE (31.5% lower than peers) and a steady 9% EPS CAGR for FY20-22. In the long run, we are upbeat on its cost optimization measures and expect TM to be a prime beneficiary of 5G rollout. Technically, the stock is poised for a downtrend reversal to retest RM4.09-4.58 upside targets, after tumbling 13% from a 52-week high of RM4.58, while downside risk is cushioned near RM3.80-3.86 zones. Cut loss at RM3.75.

Potential downtrend reversal amid hammer pattern. After falling 15.7% from the 52-week high of RM4.58 to RM3.86 (24 July), TM staged a technical rebound to end at RM3.98 yesterday. In the wake of a hammer candlestick formation and bottoming up indicators, we expect the stock to recapture above the key 20D SMA resistance at RM4.09 soon. A successful breakout will send share price higher towards RM4.22 (50% FR) before reaching our LT objective at RM4.58. Supports are pegged at RM3.86 and RM3.80. Cut loss at RM3.75.

Source: Hong Leong Investment Bank Research - 28 Jul 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

2024-07-26

TM2024-07-26

TM2024-07-26

TM2024-07-26

TM2024-07-26

TM2024-07-26

TM2024-07-25

TM2024-07-25

TM2024-07-25

TM2024-07-25

TM2024-07-25

TM2024-07-25

TM2024-07-25

TM2024-07-25

TM2024-07-24

TM2024-07-24

TM2024-07-24

TM2024-07-23

TM2024-07-23

TM2024-07-23

TM2024-07-22

TM2024-07-22

TM2024-07-22

TM2024-07-19

TM2024-07-19

TM2024-07-19

TM2024-07-19

TM2024-07-19

TM2024-07-19

TM2024-07-18

TM2024-07-18

TM2024-07-18

TM2024-07-18

TM2024-07-17

TM2024-07-17

TM2024-07-17

TM2024-07-17

TM2024-07-17

TM2024-07-16

TM2024-07-16

TM2024-07-16

TM2024-07-16

TM2024-07-16

TM2024-07-16

TM2024-07-16

TMMore articles on HLBank Research Highlights

Technical tracker - HLIB Retail Research –19 July 2024 (Short-Selling)

Created by HLInvest | Jul 19, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

2

save malaysia!

3

4

Good Articles to Share

How insuring a pet may save money in the long run: Spot Pet CEO

5

Good Articles to Share

6

Good Articles to Share

7

Good Articles to Share

Wall Street expert warns stock market is a 'really big accident waiting to happen'

8

Good Articles to Share

North Korea vows 'total destruction' of enemy on Korean War anniversary

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....