HLBank Research Highlights

Homeritz Corporation - Value resurfaces

HOMERIZ risk-reward profile is attractive after sliding 28% from an all-time high of RM0.89 to RM0.64 yesterday, supported by undemanding valuations of 7.9x (ex NCPS of 19sen) FY21E P/E and 1.08x P/B (22% below peers). The group is expected to ride on the promising industry outlook, boosted by: 1) structural demand shift on the US-China trade tension; 2) pent-up demand for furniture amid the work-from-home (WFH) trend; and 3) sustainable margins on price reviews and improved utlisation despite growing pressures from stronger RM and higher raw material prices. Meanwhile, as an ODM manufacturer, it provides HOMERIZ with a better competitive advantage due to superior cost control from its integrated manufacturing operations and its in-house R&D team.

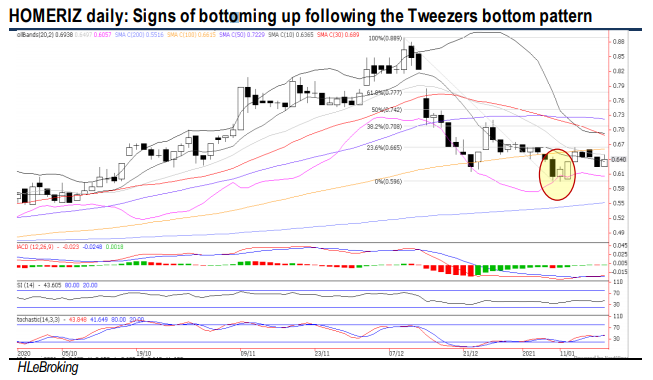

Signs of bottoming up following the Tweezers bottom formation. After hitting an all-time high of RM0.89 (9 Dec), HOMERIZ share prices slipped 28% to close at RM0.64 yesterday. Following the formation of the Tweezers bottom, the stock is poised for a potential downtrend reversal as technical indicators are on the mend. A decisive breakout above RM0.665 (23.6% FR) will spur prices higher towards RM0.71 (38.2% FR) before advancing further to our LT objective at RM0.78. Key supports are situated near RM0.595 (Tweezers bottom on 8 &11 Jan) and RM0.58 (200W SMA). Cut loss at RM0.57.

Source: Hong Leong Investment Bank Research - 20 Jan 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

2

3

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

4

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

5

Mercury Securities Research

6

BFM Podcast

7

8

BFM Podcast

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....