HLBank Research Highlights

Technical Tracker - Lagenda Properties - Sustainable business model to overcome challenges

Lagenda Offers Economical & Affordable Landed Homes (equipped With Community Facilities & Public Amenities) for the Underserved Housing Markets to Cater to the Mass B40 and M40 Income Groups. This Sustainable and Scalable Business Model Has Transformed the Perak-based Property Developer (with Self-sustaining Townships in Sitiawan, Teluk Intan and Tapah) to Expand Its Foray Into Sungai Petani (Kedah), Kuantan (Pahang) and Mersing (Johor).

We like Lagenda for its exposure to the underserved affordable housing segment, defensive customer profile (public sector workers with government financing access), low land cost, high booking conversion rate and superior margins.

All in all, Lagenda has over the years displayed a remarkable track record, underpinned by solid FY20-23 EPS CAGR of 31%, attractive 5.4% FY22 dividend yield, superior FY22 ROE of 25.7%, and remaining GDV over RM6bn to be developed for the next 5-6 years. The stock is also trading at an undemanding 5.6x FY22 FD P/E (5.1x if ex-NCPS 12sen estimated for FY22), which is a steep 39% discount vs peers’ P/E of 9.2x.

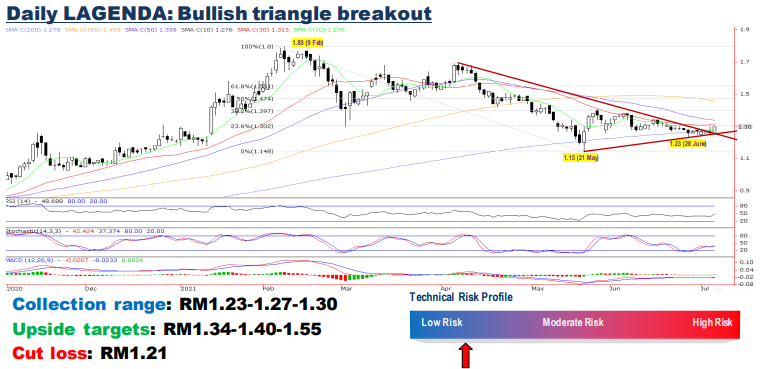

The bullish triangle breakout and a close above 200D SMA (RM1.27) with high volume (1.57m shares vs 20D average 0.7m) will spur the stock higher towards RM1.34-1.40- 1.55 levels, supported by bottoming up indicators.

Source: Hong Leong Investment Bank Research - 7 Jul 2021

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on HLBank Research Highlights

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Latest Videos

MQ Trading Signals

Time

Signal

Duration

Type

2024-11-22 16:40:00

EMA 5

5 Mins

BUY

2024-11-22 16:35:00

ADX

5 Mins

BUY

2024-11-22 16:20:00

ADX

5 Mins

SELL

2024-11-22 16:10:00

ADX

5 Mins

BUY

2024-11-22 14:30:00

EMA 5

5 Mins

SELL

Apps

Top Articles

2

3

BFM Podcast

4

5

BFM Podcast

6

Axcapital's investment blog

KAB - Executing its way to a record quarter. Could more Petronas contracts be coming?

7

Koon Yew Yin's Blog

CPO price is rising rapidly as shown by chart below - Koon Yew Yin

8

Mercury Securities Research

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....