Bursa Hunter-net-Hunter

纬树股东大会提呈建议:分红股缔造双赢

致董事部

您好,我持有纬树控股的股份已经有一年多了,资本增值加股息近乎一倍,感谢董事部及全体员工的辛劳付出。

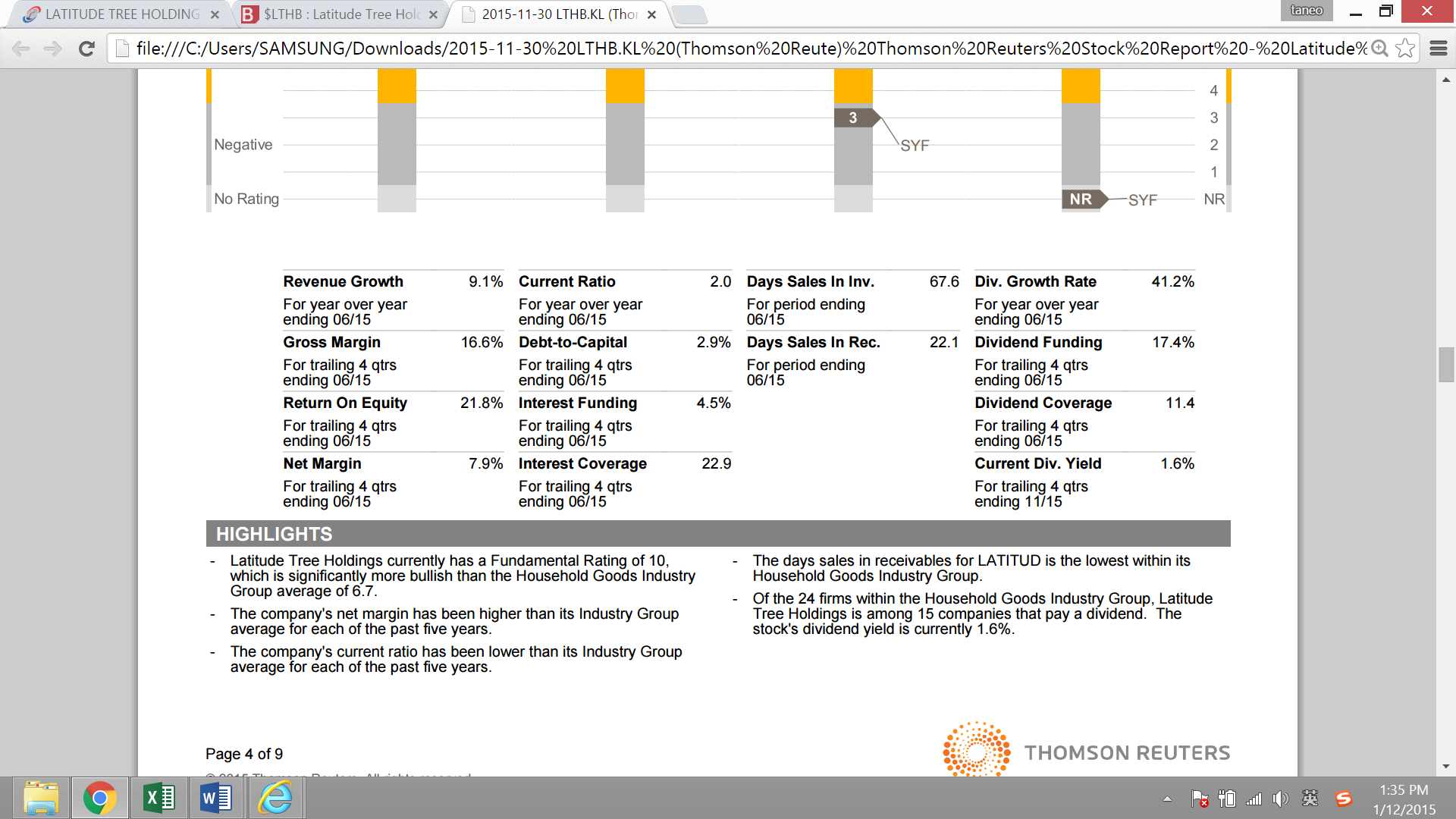

目前我还打算长期持有,并对公司的前景极具希望。因为我做了详细的家私股对比,纬树的股东回酬率高达20%,为同行之最。而且纬树的经营作风稳打稳扎,借贷有度。尽管市况不错也不会贸然大肆扩张。

但是目前纬树的股价6.5令吉仅仅是以不高于9倍的本益比交易,相比其他家私股略为逊色。

论股东回酬率,纬树无疑是最高的,但却没有享有应有的溢价。我猜想这是因为纯粹以股价比较,纬树是最高的,市场觉得纬树很“贵”,所以选择其他的家私股。

要如何使纬树的股价表现更加的出色呢?我的建议是分红股(bonus issue),如果能够附送凭单就更好不过。

比如说Hevea、Pohuat和Liihen等家私股的股价在宣布分红后表现踊跃就是很好的证明。

目前,纬树的保留盈利对股本的比率为3倍,适合以一对二的比率分红股。

一旦股票的流通量增加,能够吸引基金的入驻,有助于稳定股价,那么股价就不会那么容易遭到低估。

若股东需要用到钱周转,也不会被迫贱卖公司的股票。此外,公司以后打算扩张产能,也可以以溢价筹资,对公司和股东都是双赢的局面。

期待董事部的回应,谢谢。

纬树的小股东 上

More articles on Bursa Hunter-net-Hunter

MWE bhd's 26% stake in WCE is worth more than its mother, no wonder Upatkoon wanted to privatize it

Created by kakashit | May 08, 2017

TA Global to gain bulk of profit from Trump Tower (Graphic Illustration)

Created by kakashit | Feb 10, 2017

Discussions

Be the first to like this. Showing 22 of 22 comments

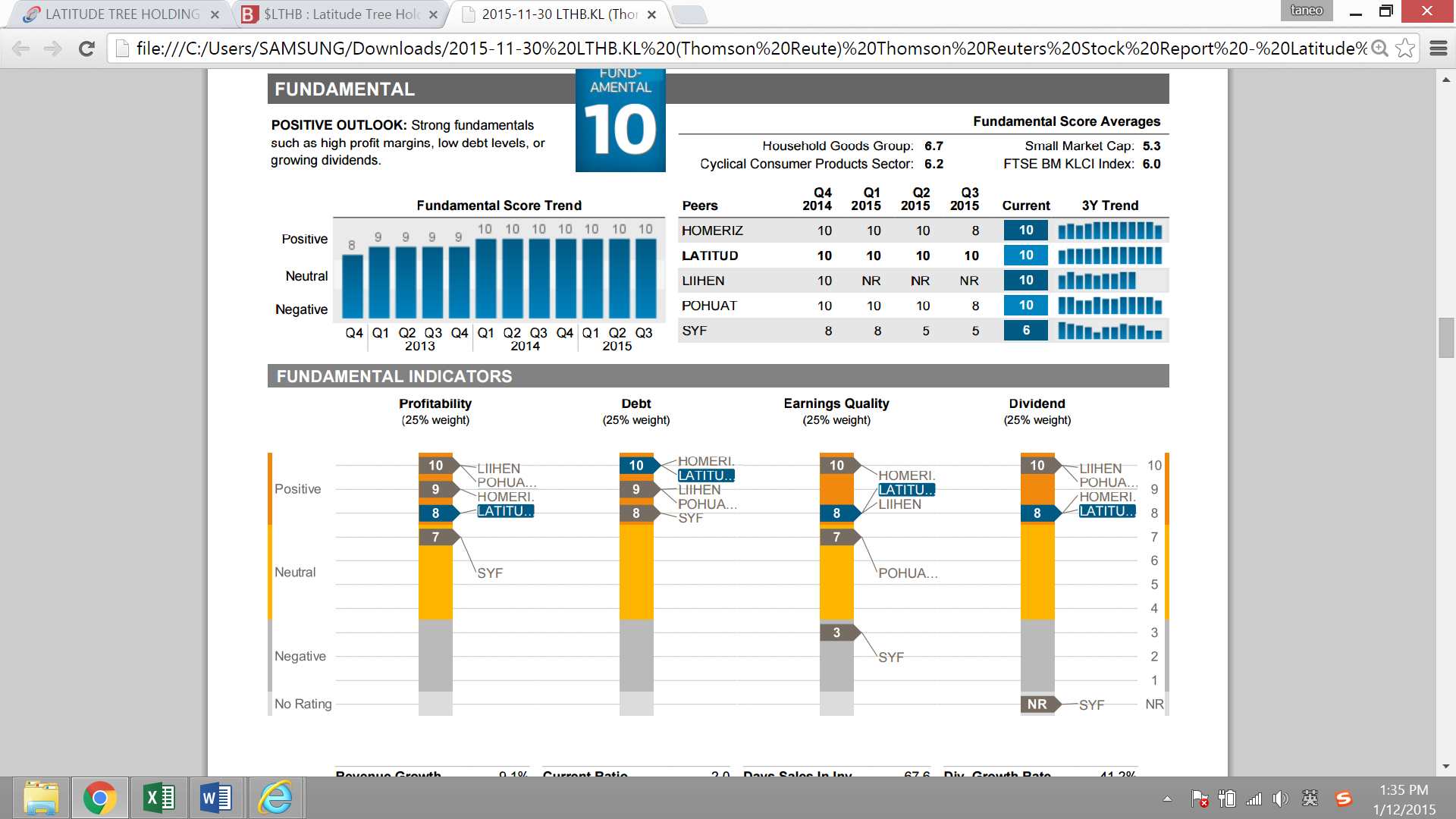

1. 相比其他家私股略为逊色 - PE is determined by ROE, if you compare it to Homeriz, Latitude ROE looks pretty bad

2. 分红股 - Bonus issue doesnt make anyone richer. You as a long term investor should know that. Bonus issue or free warrant or split whatever is just a 'trick' to shiok yourself.

3. 一旦股票的流通量增加,能够吸引基金的入驻, 不会那么容易遭到低估 - Dutch Lady got 64 million shares, Latitude has 97 million shares. And how many institutions own Dutch Lady? Plenty. Is DL undervalued? Nope.

4. 要如何使纬树的股价表现更加的出色呢? Increase all the below: ROE, ROIC, ROE, ROIC, ROE, ROIC, ROE, ROIC, ROE, ROIC. Stop wasting time and money issue bonus. They can go ahead and split the shares until 5 billion, it would NOT add any value to shareholders.

2015-12-01 15:52

JT Yeo,

1. Have a look at the below ROE:

Homeritz - 21.67%

Pohuat - 17.43%

Liihen - 21.72%

Latitude - 19.35%

Do you think it looks PRETTY bad?

2. Bonus issue is to sound like "reward" shareholder, but I guess the main intention of KAKASHIT is to hope the number of LATITUDE shares to be increase. Or maybe it can be the other way, SHARE SPLIT. Either share split or bonus issue will make LATITUDE share price to be cheaper and hence more people will be affordable. The possibility of continue going up is much higher, isn't it?

3. Latitude PE is 8.1+ currently, the lowest compared to Homeritz, Pohuat and Liihen. By looking at this, don't you agree that LATITUDE is undervalue and also the cheapest among others furniture company?

4. I agree with your forth statement. Latitude should use their cash to further expand their production capacity or acquisition so that they can increase their revenue and profit. This is one of the way to maximise shareholder fund.

2015-12-01 16:41

RicheHo,

1. If you look at a normal year or for past 3 years 2012-2014 ROE 4%, 11% & 20%, Homeritz has a more consistent ROE, which always stayed above 18%, I think the market is right to give Homeritz a higher PE.

2. I think the possibility it will go up is 99%, the possibility it will add real value is 1%.

3. If you use comparative valuation, it is 'undervalued' to the industry average. If you look at historical ROE I think it is fair price. Or from FCF, Latitude generate avg FCF of 34mil, Homeritz FCF is half of that. Homeritz EV is half of Latitude.

4. I heard they are going up/down stream of the supply chain like acquiring kiln operations. Again if those activities has higher ROE they should pursuit but if ROE is lower they will just dilute their ROE and bloat the company. Case in point being CBIP, they have a wonderful business selling palm oil mill to plantations company. Patented design, high margin/ROE, cost is the biggest pain of plantations co everyone wants to upgrade their mill to compete, great business. And they go and invest all their money into buying lands and grow palm oil, a commodity industry, a price taker, a capital intensive, a low margin/ROE business.

2015-12-01 17:31

Here come our PE haters. He say homeriz should be higher. By higher by how much? He didnt say. He dun know give a value to a company but he keep say one comoany should higher than one company. But what is the fair value?

2015-12-01 17:53

Or u mean if roe high u can buy at any price? PE not important. Common. PE13.38 vs PE8. Differences by 67.5percent!!

2015-12-01 18:17

http://koonyewyin.com/wordpress/2015/05/04/how-to-improve-the-price-and-liquidity-of-latitude-tree-bhd/

Letter to the CEO of Latitude Tree Bhd.

Dear Joseph Lin,

Your shareholders register will show that my wife Tan Kit Pheng, my nephew Yap Sung Pang and I are holding more than 10% of your total issued shares.

We must congratulate your management for producing such a fantastic profit. As a result, your share price has gone up very rapidly from Rm 1.00 to above Rm 6.00 in the last 24 months. You would have noticed that it has come down in the last few trading days because we have not been supporting it. Even though it is selling so cheaply in terms of P/E ratio, many investors and fund managers I spoke to, would not buy it because they are afraid that they cannot sell at some point due to poor liquidity.

I would like your board of directors to consider my suggestion on how to improve the share price and its liquidity.

Immediately give out 1 bonus share for every 4 shares held.

Split one shares into 5 shares making 20 sen its par value.

Declare to give out 1 bonus share for every 4 shares held for the next financial year.

Declare a dividend policy of giving out 30% of net annual profit.

After the completion of item 1 and 2 above, 4 original shares with one bonus share will become 25 shares. Basing on the current share price of about Rm, 6.00, the new price will be about 96 sen. It is easier for 96 sen to move up to Rm 1. 92 sen than for Rm 6.00 to move up to Rm 12.00.

Basing on your first half year profit of 45 sen per share and 100% of your products are being exported for US$, every investor can foresee your EPS for the year will most likely exceeds Rm 1.00. Moreover, you have additional income from your huge cash deposit with Banks. Your share should deserve to sell at a higher P/E ratio.

A higher share price will benefit all the shareholders, including you, as controlling shareholder. Moreover, with a higher share price, the company can take advantage of it for acquisition of assets and share placement every year according to Securities Commission rules to get large amount of cash for company expansion.

As one of the founders of IJM Corporation Bhd, I know that the company has been doing what I have described above regarding share placement and assets acquisitions to expand the company. Basing on the current IJM Corporate Bhd share price, its market capitalization exceeds Rm 13 billion.

Koon Yew Yin

2015-12-01 18:24

Never said high ROE can buy at any price, but high ROE does common a higher valuation, all other else being equal. case in point Harta, PBB, Amway etc

2015-12-01 18:47

Harta is harta. Ppb is ppb. Those are really giant multinasional company. Cannot use in homeriz and latitude case. Somemore in term of size, latitude is much more bigger than homeriz.

My question again. Then how u calculate what is the value for homeriz and latitude? Do you have any calculation to show the value of homeriz and latitude without using PE ratio?

2015-12-01 18:56

Dear Mr Koon,

Thank you for buying 10% of the company's shares and pushing the share price up while so doing.

We were advised you have been a significant shareholder in other public listed companies such as JTiasa and Mudajaya in 2014 but no longer.

We as the management of the company would like our large shareholders to show loyalty and commitment to company business, not just be a fair weather stakeholder who makes money from trading the shares.

If you have a sound business proposal for ours company, We will happy to hear from you. Otherwise happy holding.

Joseph Lin

On behalf of Latitude Management

2015-12-01 19:04

ok we will use DCF

Average 3 years DCF = 67mil.

Assume Capex = depreciation = 20mil

FCF = 47mil.

Growth rate next 10 years = 5%

Terminal growth rate = 3%

Total present value of cash flows = 810 mil

Outstanding shares = 97,208

Value per share = $8.34

Comments: 10 years growth at 5% isn't low at all. Not many companies can grow more than 10% in the long term, unless they got moat. When KC Chong did a valuation on Latitude in March 2014, using 5% growth in FCF, he comes up with a value of $6.13. That is $2 per share difference from my valuation in just over 20 months. That gives you a good gauge that Latitude value is sitting somewhere around $7-8. Very rough but we can never be precise.

http://klse.i3investor.com/blogs/kcchongnz/48173.jsp

For Homeritz

Average 3 years DCF = 23mil.

Assume Capex = depreciation = 3mil

FCF = 20mil.

Growth rate next 10 years = 5%

Terminal growth rate = 3%

Total present value of cash flows = 341 mil

Outstanding shares = 300,000

Value per share = $1.14

2015-12-01 19:38

U didnt show the calculation. Just show ur calculation out. Anyway rm1.14 for homeriz? Seriously i wont buy any homeriz at this price. It is overvalued

2015-12-01 19:42

Pls la. U cannot use the grow rate 5percent. U cannot even predict when the economy downturn. Somemore using this method, it did not book in what strategies that the company will implement. If the company going for wide expansion, u cannot book in the price using this method.

I dont know about homeriz but latitude have been improve year by year for 9 consecutive quarter. The grow of profit is way more than 5percent. 5percent is way too underestimate.

Somemore even using the 5percent grow, latitude is still way more undervalue than homeriz

2015-12-01 19:50

Evertthing also got value. As a investor, we know the value and we buy at cheap sell when expensive. There is bunch of good company in bursa malaysia. As investor we must buy cheap sell expensive. U tell people to buy homeriz which is already fully value and dont buy latitude which is undervalue?

2015-12-01 19:55

Figure is juz figure, in the end, u still need to look at the business prospect.

Juz bcoz there're many thing we do not know other than figures, so we must practice diversification, or polygamy.

2015-12-01 22:15

Well from my calculation, both are fairly valued, not a good price to enter thats all. Kakashit, everyone has their own calculation, just like your letter, i can disagree every single point of it, but that doesnt reduce the people that want bonus issue to make themselves happy.

2015-12-02 04:07

The practice of investing is to listen to different opinions, after that, if you still want to stick to what you do, you have your conviction, simple as that.

2015-12-02 06:10

Nvm different people got different opinion. Let see how much it priced in the long run

2015-12-02 13:51

Post a Comment

Featured Posts

Latest Videos

Apps

Top Articles

1

Stock Market Enthusiast

YTLPower: Hammer + Oversold + Strong Support Level Means Bullish Reversal?

2

CEO Morning Brief

These Big-cap Stocks on Bursa Pay More Than 5% Dividend Yield

3

Mercury Securities Research

4

5

RHB Investment Research Reports

6

Kenanga Research & Investment

7

M+ Online Research Articles

8

AmInvest Research Reports

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

MQ Trading Signals

Stock

Time

Signal

Duration

Stock

Time

Signal

Duration

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....

murali

Nowadays all use the same tricks....

2015-12-01 15:24