Kenanga Research & Investment

Daily technical highlights – (LYC, NTPM)

LYC Healthcare Bhd (Trading Buy)

- After rising from RM0.12 on 19 March to hit a high of RM0.54 on 1 June, LYC’s share price subsequently pulled back by as much as 52% to a low of RM0.26 recently before closing at RM0.33 yesterday.

- On the chart, its RSI indicator – which has been sliding towards the oversold territory in tandem with the share price weakness – saw a tick-up recently, possibly indicating that a short-term trend reversal may be underway.

- A likely rebound could push the stock to reach our resistance target of RM0.39 (R1), before challenging the next resistance level of RM0.44 (R2) thereafter. This represents potential returns of 18% and 33%, respectively.

- Our stop loss threshold is pegged at RM0.28 (or 15% downside risk).

- Meanwhile, pursuant to an ongoing private placement exercise involving the issuance of up to 30% of its share base (representing 107.2m shares), LYC’s major shareholder Lim Yin Chow (who currently holds a 18.3% stake) has stated his intention to take up any unsubscribed portion of up to 50.0m shares. This could be a seen as a vote of confidence in the Group’s fundamentals from its substantial shareholder.

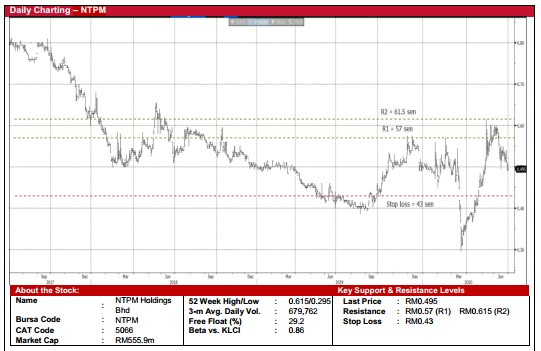

NTPM Holdings Bhd (Trading Buy)

- After the March market meltdown, NTPM’s share price has since recovered from a trough of RM0.295 to peak at RM0.615. It saw a subsequent correction and settled at RM0.495 yesterday.

- On the chart, the stock is looking to find support around the current price levels. This could then pave the way for its shares to resume its uptrend soon.

- Riding on the positive momentum, its share price will probably climb to our resistance target of RM0.57 (+15% potential upside), before testing the next resistance line of RM0.615 (+24% potential upside).

- On the downside, the stop loss level is set at RM0.43 (-13% downside risk).

- Fundamentally, NTPM stood out in the current result reporting season with a better earnings performance (unlike the majority of listed companies which were hit by the Covid-19 restrictions). It posted net profit of RM4.1m in the Feb-Apr quarter (versus net loss of RM4.9m in the previous year) on the back revenue of RM201.6m (+11% YoY) as the Group (which is involved in the business of tissue paper and personal care products) remains largely unaffected by the Covid-19 pandemic.

Source: Kenanga Research - 1 Jul 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

Market Buzz

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

4

Good Articles to Share

5

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

6

Good Articles to Share

7

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....