Kenanga Research & Investment

Daily Technical Hightlight - (MGRC, PWROOT)

Malaysian Genomics Resources Centre Bhd (Trading Buy)

• MGRC was previously involved in the business of providing clinical pathology and medical laboratory services via MPath group (which contributed c.99% of FY19 revenue).

• However, post the disposal of MPath group in Dec 2019 for RM42.0m, MGRC now plans to leverage on its expertise in marketing and distribution in the clinical pathology business by adding companion diagnostic and cancer immunotherapy to its products portfolio.

• On June 30th 2020, the group announced that it has secured a 20-year exclusive licensing rights for Malaysia, Singapore, Thailand and 5 other South East Asian countries for CAR T-cell therapy for solid cancers of organs (such as liver, pancreas and stomach) under a tripartite licensing agreement signed recently with ICARTAB Biomedical (iCARTab) and Advance Immune Therapeutics (AIT).

• Financially, MGRC is a debt-free company with RM6.0m in cash, which translates to 5.8 sen/share.

• On the chart, the stock has retraced from an all-time high of RM0.84 on 7th August 2020. Since then, the stock has been consolidating near the bullish Kumo Cloud while forming higher lows. A pennant pattern is also in sight, which indicates signs of a potential breakout.

• Should the buying momentum return, our overhead resistance levels are set at RM0.62 (R1) and RM0.71 (R2), which translates to potential upsides of 16% and 33%, respectively.

• Our stop loss is set at RM0.47 (-12% downside risk).

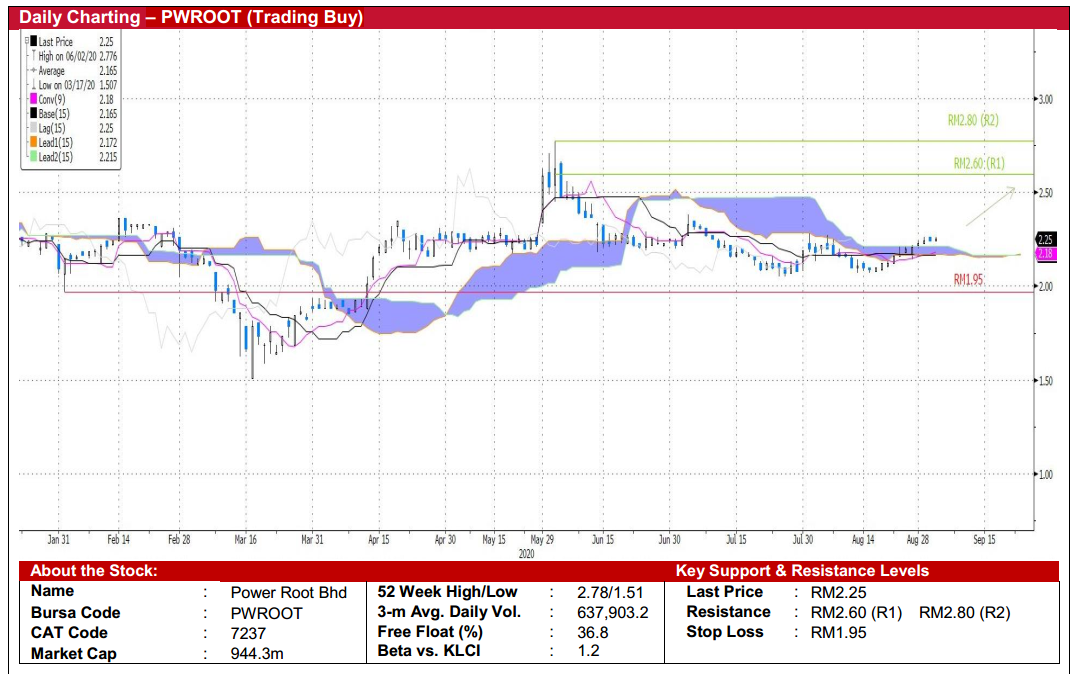

Power Root Bhd (Trading Buy)

• PWROOT is engaged in the production of pre-mixed instant powder beverages in Malaysia. The group manufactures and distributes its beverage products in the FMCG (Fast Moving Consumer Good) segment.

• The group saw its 1QFY21 net income declined to RM10.7m (-15% QoQ) due to lower sales at shopping malls following the implementation of the movement control order (MCO) in March. Nevertheless, sales are on the recovery since the relaxation of the MCO in May.

• Consensus is currently projecting net incomes of RM53.7m (+4.6% YoY) in FY21E and RM59.7m (+11.1% YoY) in FY22E, which translates to forward PERs of 17x and 16x, respectively.

• Chart-wise, the stock has been consolidating within the range of RM2.06 to RM2.28 since early-July. Ichimoku-wise, the stock has broken above the Kumo Cloud, indicating that it could potentially continue its upward momentum.

• With that, our resistance levels are set at RM2.60 (R1) (+16% potential upside) and RM2.80 (R2) (+24% potential upside). • Our stop loss level is pegged at RM1.95 (-13% downside risk)

Source: Kenanga Research - 4 Sept 2020

Related Stocks

| Chart | Stock Name | Last | Change | Volume |

|---|

More articles on Kenanga Research & Investment

Actionable Technical Highlights - PRESS METAL ALUMINIUM HLDG BHD (PMETAL)

Created by kiasutrader | Nov 25, 2024

Actionable Technical Highlights - PETRONAS CHEMICALS GROUP BHD (PCHEM)

Created by kiasutrader | Nov 25, 2024

Weekly Technical Highlights – Dow Jones Industrial Average (DJIA)

Created by kiasutrader | Nov 25, 2024

Malaysia Consumer Price Index - Edge up 1.9% in October amid food price surge

Created by kiasutrader | Nov 25, 2024

Discussions

Be the first to like this. Showing 0 of 0 comments

Post a Comment

Featured Posts

Introducing MY's First IPO Fund for Sophisticated Investors!

New Update. Discover investment communities that resonate with your ideas

M & A Value Partners IPO Equity Fund has been launched - Targeted 13% Return p.a

Latest Videos

Apps

Top Articles

1

2

3

save malaysia!

Visa-free travel to China extended for Malaysians to 30 days

4

Good Articles to Share

5

Good Articles to Share

What’s behind the slew of restaurant bankruptcies in 2024? Experts unpack the problems

6

Good Articles to Share

Four convicted in Spain over homophobic murder that sparked nationwode protests

7

Good Articles to Share

8

Good Articles to Share

#

Stock

Score

Daily Stocks

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Stock Name

Last

Change

Volume

Featured Advertisers / Partners

Ride The Bull Short The Bear

CS Tan

4.9 / 5.0

This book is the result of the author's many years of experience and observation throughout his 26 years in the stockbroking industry. It was written for general public to learn to invest based on facts and not on fantasies or hearsay....